How Many of the Uninsured Can Purchase a Marketplace Plan for Less Than Their Shared Responsibility Penalty?

Issue Brief

The Affordable Care Act (ACA) has expanded health insurance coverage by offering both penalties and incentives. The ACA expanded eligibility for Medicaid, and low and middle-income households who earn too much to qualify can purchase subsidized coverage on the health insurance marketplaces using premium assistance tax credits. Individuals, who do not obtain coverage, are subject to a tax penalty under the law’s individual mandate unless they meet certain exemptions. While the percent of the population without health coverage has decreased substantially since the major coverage expansion in the ACA, about 10% of the population is still uninsured. Some of those who remain uninsured are eligible for premium subsidies large enough to cover the entire cost of a bronze plan, which is the minimum level of coverage people can buy to satisfy the individual mandate. Others could obtain coverage, after taking into account premium subsidies, for less than the penalty they would have to pay under the individual mandate. This analysis looks at the non-elderly uninsured eligible to enroll in a marketplace plan to determine how many of them would be financially better off enrolling in coverage than paying the penalty.

{kind=link}

Who Is Subject to the Individual Mandate

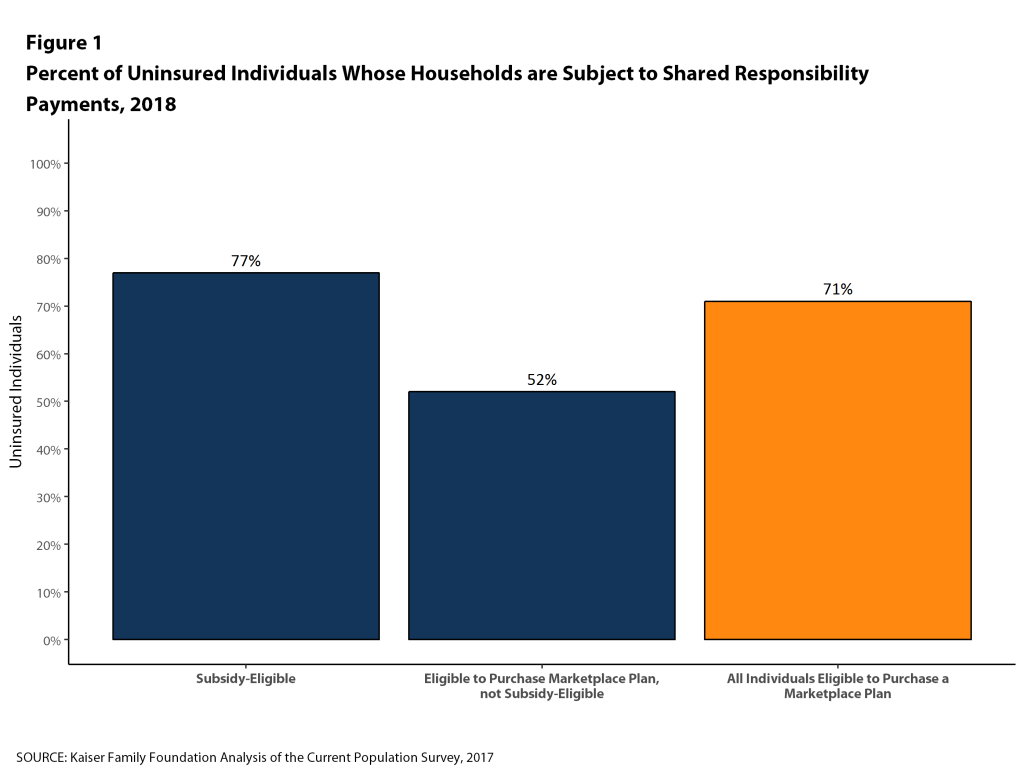

The ACA included the shared responsibility payment, commonly known as the individual mandate, to encourage healthier individuals to purchase coverage offered by the Marketplaces. Since 2014, most people are required to be covered by a health insurance policy which meets minimum standards or pay a tax penalty. Some individuals are exempt from the penalty, including undocumented immigrants, those whose incomes are so low that they are not required to file taxes, people in the “Medicaid Coverage gap,” people who have to pay more than 8.05% of household income for insurance (taking into account any employer contributions or subsidies), members of certain groups, such as religious minorities or those facing a specified hardship such as foreclosure or bankruptcy. In 2018, we estimate that 71% of the marketplace-eligible uninsured will be subject to a penalty if they do not buy insurance, including 77% of those eligible for premium subsidies and 52% of those who are not.

The penalty is assessed as 2.5% percent of family income in excess of tax filing thresholds with both a minimum and maximum. The penalty can be no less than a flat dollar amount equal to $695 per adult plus $347.50 per child, up to $2,085 for the family. The penalty can also be no more than the national average premium for a bronze plan. In 2017, the national average bronze plan was $272 for single coverage and $1,360 for a family of five or more. The penalty is pro-rated for people who are uninsured for a portion of the year and waived for people who have a period of insurance of less than three months.

For How Many of the Remaining Uninsured is Coverage Cheaper than the Penalty

The premium tax credits that subsidize Marketplace coverage are calculated using the second-lowest cost silver plan in each rating area as a benchmark. Since the Federal Government elected recently not to reimburse insurers for the cost sharing reductions they are required to make to reduce cost sharing for some low income enrollees, many insurers passed the increased cost on through higher premiums for silver plans. With higher silver premium costs, many people eligible for Marketplace subsidies will receive a larger tax credit. In many cases, consumers will be able to purchase a bronze plan for no additional cost, and in some cases a gold plan will be free or relatively inexpensive.

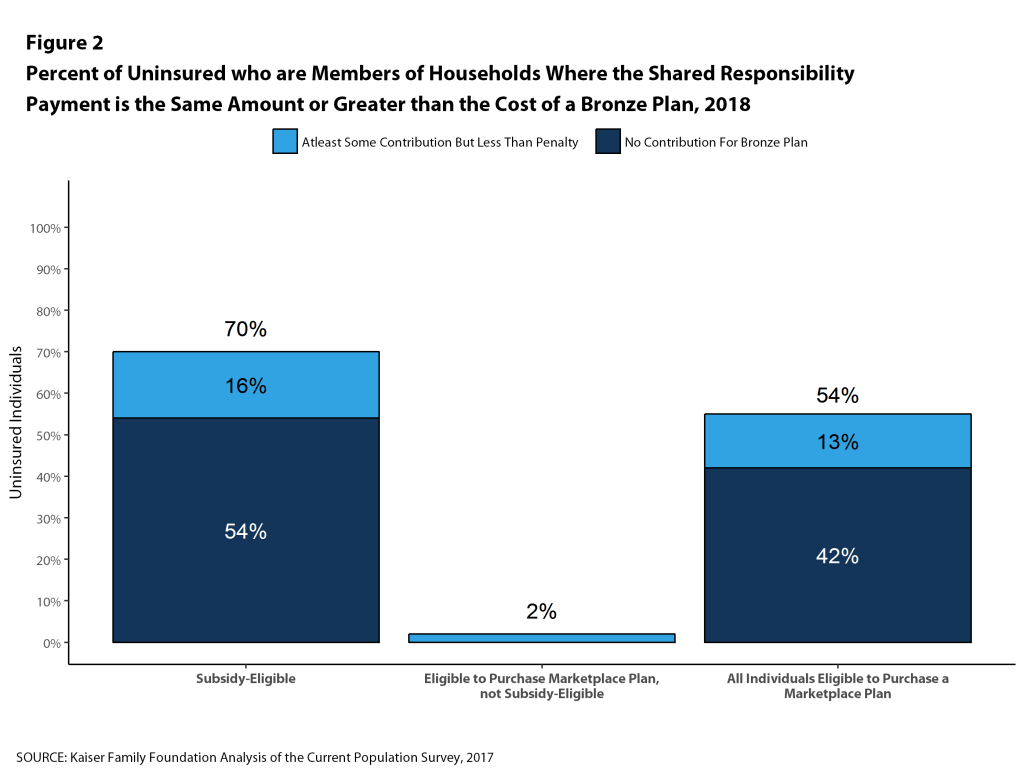

We estimate that over half (54%) of the subsidy eligible-uninsured could purchase a bronze plan for 2018 for no premium contribution, after accounting for the premium subsidy. An additional 16% of this group could purchase a bronze plan for less than the cost of the tax penalty if they do not secure minimum essential coverage. Altogether 70% of subsidy eligible-uninsured (5.8 million people) are able to purchase a Bronze plan for nothing or less than the cost of the individual mandate penalty.

Just over half (54%) of uninsured individuals who are eligible to purchase a marketplace plan with or without a subsidy would better off financially if they purchased a bronze plan rather than remaining uninsured. Of the 10.7 million people who are currently uninsured and eligible to purchase marketplace coverage, around 7.7 million people will be subject to the shared responsibility penalty. Most of these people will have access to at least some subsidies (6.3 million) to purchase a Marketplace plan.

Generally, consumer must enroll in a marketplace plan before the end of the open enrollment period (December 15), but do not bear the cost of the penalty until they complete their 2018 income taxes by April of 2019. Significant numbers of the remaining uninsured risk paying more in tax assessments than the cost of enrolling in coverage.

Methods

This analysis uses data from the 2017 Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC). The CPS ASEC provides socioeconomic and demographic information for the United Sates population and specific subpopulations. Importantly, the CPS ASEC provides detailed data on families and households, which we use to determine income and household composition for ACA eligibility purposes.

Medicaid and Marketplaces have different rules about household composition and income for eligibility. For this analysis, we calculate household membership and income for both Medicaid and Marketplace premium tax credits for each person individually, using the rules for each program. For more detail on how we construct Medicaid and Marketplace households and count income, see the detailed technical Appendix A available here.

Undocumented immigrants are ineligible for federally-funded Medicaid and Marketplace coverage. Since CPS data do not directly indicate whether an immigrant is lawfully present, we draw on the methods underlying the 2013 analysis by the State Health Access Data Assistance Center (SHADAC) and the recommendations made by Van Hook et. al.15,16 This approach uses the Survey of Income and Program Participation (SIPP) to develop a model that predicts immigration status; it then applies the model to CPS, controlling to state-level estimates of total undocumented population from Pew Research Center. For more detail on the immigration imputation used in this analysis, see the technical Appendix B available here.

Individuals in tax-filing units with access to an affordable offer of Employer-Sponsored Insurance are still potentially MAGI-eligible for Medicaid coverage, but they are ineligible for advance premium tax credits in the Health Insurance Exchanges. Since CPS data indicate whether a worker held an offer of ESI at the time of interview (for the 2017 CPS, February, March, or April 2017) but not during the prior year (which serves as our basis for type of insurance coverage), we developed a model that predicts offer of ESI for any individuals with a change in employment status across the period. Additionally, for families with a Marketplace eligibility level below 250% FPL, we assume any reported worker offer does not meet affordability requirements and therefore does not disqualify the family from Tax Credit eligibility on the Exchanges. For more detail on the offer imputation used in this analysis, see the technical Appendix C available here.

The CPS asks respondents about coverage at the time of the interview as well as throughout the preceding calendar year. People who report any type of coverage throughout the preceding calendar year are counted as “insured.” Thus, the calendar year measure of the uninsured population captures people who lacked coverage for the entirety of 2016 (and thus were uninsured at the start of 2017). We use this measure of insurance coverage in 2016, rather than the measure of coverage at the time of interview, because the latter lacks detail about coverage type that is used in our model.

As of January 2014, Medicaid financial eligibility for most nonelderly adults is based on modified adjusted gross income (MAGI). To determine whether each individual is eligible for Medicaid, we use each state’s reported eligibility levels as of January 1, 2017, updated to reflect state Medicaid expansion decisions as of October 2017 and 2016 Federal Poverty Levels.17 Some nonelderly adults with incomes above MAGI levels may be eligible for Medicaid through other pathways; however, we only assess eligibility through the MAGI pathway.18

The household contribution for a marketplace plan includes the cost of covering all subsidy-eligible individuals in the tax filing unit, including those who might currently be purchasing non-group coverage outside of the exchange. Individuals who are eligible for a Basic Health Plan in New York or Minnesota are included as subsidy-eligibles in this analysis. The penalty for each uninsured non-elderly individual is based on the number of uninsured people in the household. In this analysis, households with incomes below the relevant tax filing threshold, in the Medicaid gap, or where the cost of the cheapest available (subsidized) bronze plan exceeds the affordability standard are considered to not have a penalty. Individuals ineligible to purchase marketplace coverage, such as undocumented immigrants, are excluded from the analysis. There may be additional exemptions which individuals are eligible for, including particular hardships such as medical debt or domestic violence and membership in groups such as a health care sharing ministry or a recognized Indian tribe. Individuals 65 or above are excluded from the analysis.