In an effort to reach a deal to extend the enhanced Affordable Care Act (ACA) premium tax credits, some members of Congress are talking about limiting financial help to people below a certain income threshold.

The enhanced premium tax credits are already on a sliding scale and naturally phase out as incomes rise. For people with higher incomes, the enhanced tax credit becomes smaller and eventually disappears once their expected premium contribution (8.5% of income) matches the full premium in their area. In other words, the enhanced premiums tax credits are means-tested in a way, but the income at which they phase out varies by county and age, based on local premiums.

If Congress reinstates an income cap—or allows the enhanced subsidies to expire—the “subsidy cliff” would return. That would mean anyone earning even a small amount above the income cap would lose all financial help and pay the full cost of a Marketplace plan, regardless of how high their premiums are. Under the original ACA, before the enhanced tax credits were passed, the eligibility limit for tax credits was set at an income of four times (400%) the federal poverty level (FPL).

An income cutoff for ACA premium tax credits would reduce the cost to the federal government of extending the credits. However, from a federal budget perspective, most of the enhanced premium tax credit dollars are already going to people with incomes below $150,000 (which is over four times poverty for a family of four). The Joint Committee on Taxation estimates that if the enhanced tax credits were extended, 86% of spending would be allocated toward those making under $150,000 in 2026 and 94% of spending would be allocated toward enrollees making under $200,000 in 2026. Setting an income cap may not have much effect on the federal budget, but it could have a big effect on some household budgets, particularly for older enrollees.

An income cap for the enhanced tax credits could take shape in any number of ways, for example, by keeping enhanced tax credits for people making under four times poverty and ending them for people who make above that amount. Or Congress could set a higher income limit, say at five- or six-times poverty. Rather than using a percent of poverty, Congress could instead use a fixed dollar income cap, which would leave larger families paying more. (The poverty level varies by family size.)

Nearly 2 million ACA enrollees are known to have incomes above four times the poverty level ($62,600 for a single person or $128,600 for a family of four), and about 1 million of them have incomes above five times poverty ($78,250 for a single person or $160,750 for a family of four). There are an additional 1 million people for whom income data are not available, but it is likely they have higher incomes and have not applied for tax credits.

Based on our previous analyses, about half of these higher-income enrollees are older adults (ages 50-64), who would be hit hardest by a subsidy cliff because premiums for older adults are up to three times higher than those for younger adults.

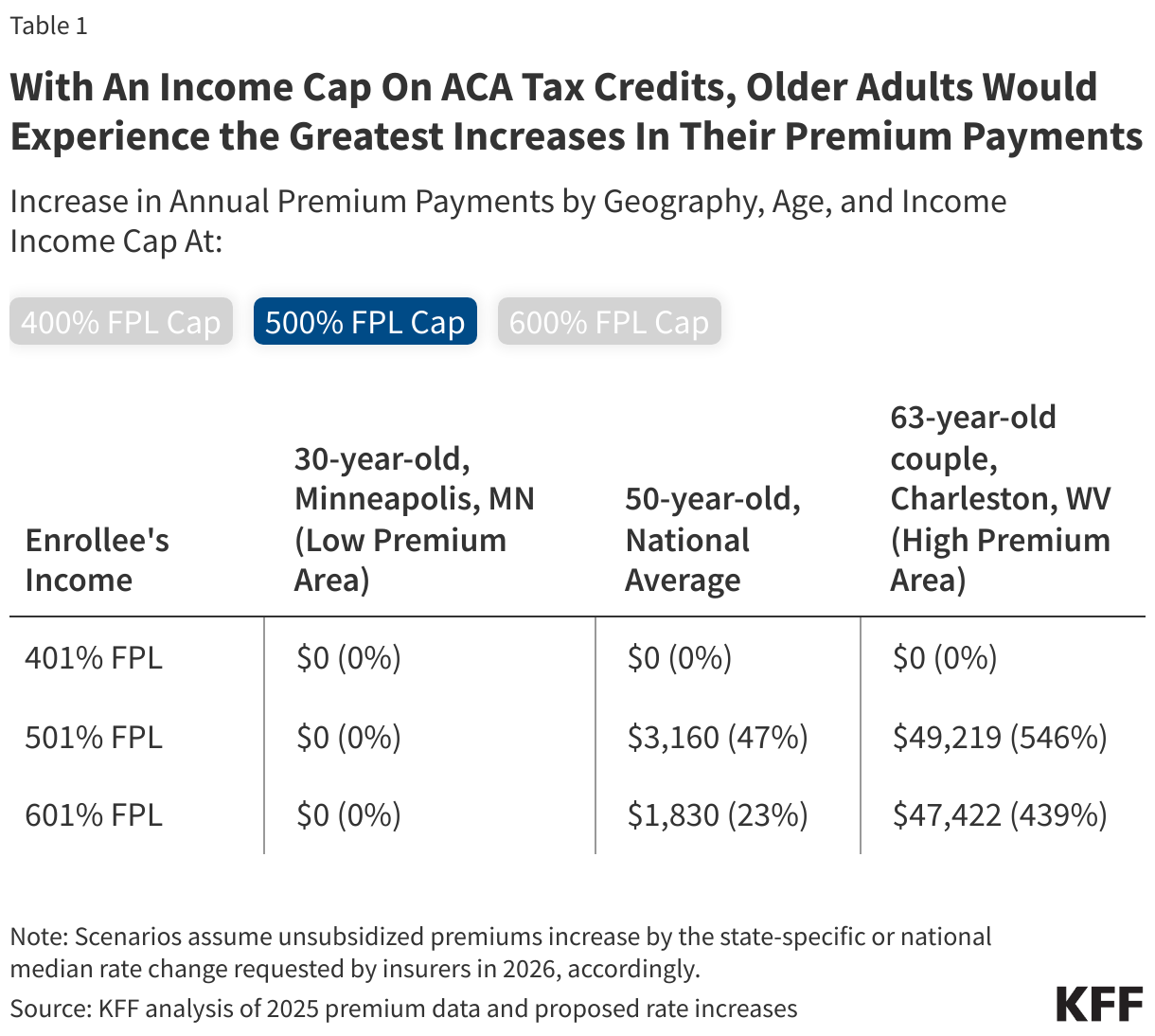

The effect of an income cap would vary greatly from person to person. For a middle-income 50-year-old, making just under $63,000 (401% FPL), losing eligibility for tax credits could mean paying roughly $4,000 more, after accounting for an 18% increase in premiums, the median rate increase proposed by insurers nationally for 2026.

In low-premium areas, like Minneapolis, Minnesota, the unsubsidized premium for a 30-year-old making just under $63,000 is so low (about 6% of their income without a tax credit, after accounting for planned premium increases in 2026), that they do not qualify for a tax credit at all, so an income cap would have no effect on them.

In high-premium areas, like West Virginia, an older couple (both age 63) making just under $85,000 (401% FPL) could face a premium increase of over $50,000 after accounting for a nearly 12% increase in premiums—making coverage unaffordable without a tax credit.

The chart below shows how much more certain enrollees would pay for a silver plan under three scenarios of income caps (400% FPL, 500% FPL, and 600% FPL), relative to a clean extension of the enhanced premium tax credits. These scenarios assume unsubsidized premiums increase by the state-specific or national median rate change requested by insurers in 2026, accordingly.