Affordable Care Act (ACA) Marketplace insurers are raising their premiums by an average of 18% next year. Insurers say that overall average includes an extra 4 percentage point increase beyond what they would otherwise charge. The reason is they expect the expiration of the enhanced premiums tax credits will lead healthier people to drop their coverage, leaving a sicker group of enrollees next year.

Premiums for all private insurance plans, including those offered by employers, are expected to rise steeply next year, simply because the cost of health services like hospital care is rising. High-cost prescription drugs like GLP-1s used for weight loss are also driving up premiums for everyone with private insurance, whether they get coverage through the ACA or not.

If Congress had acted to extend the enhanced premium tax credits over the summer, ACA insurers probably would have revised their premium increases down. Instead of premiums increasing by about 18%, they might have risen by around 14%. That would still be the sharpest increase in years.

It may be too late for insurers to change their premiums ahead of open enrollment. Insurers submit their premium requests to state regulators in the spring and summer and by fall those premiums are locked in for the next calendar year. If Congress extends the enhanced tax credits this week, with open enrollment just a few weeks away in most states (and a few days away in Idaho), it’s hard to imagine insurers having time to revise their premiums and have all the data ready for the enrollment websites to launch on time.

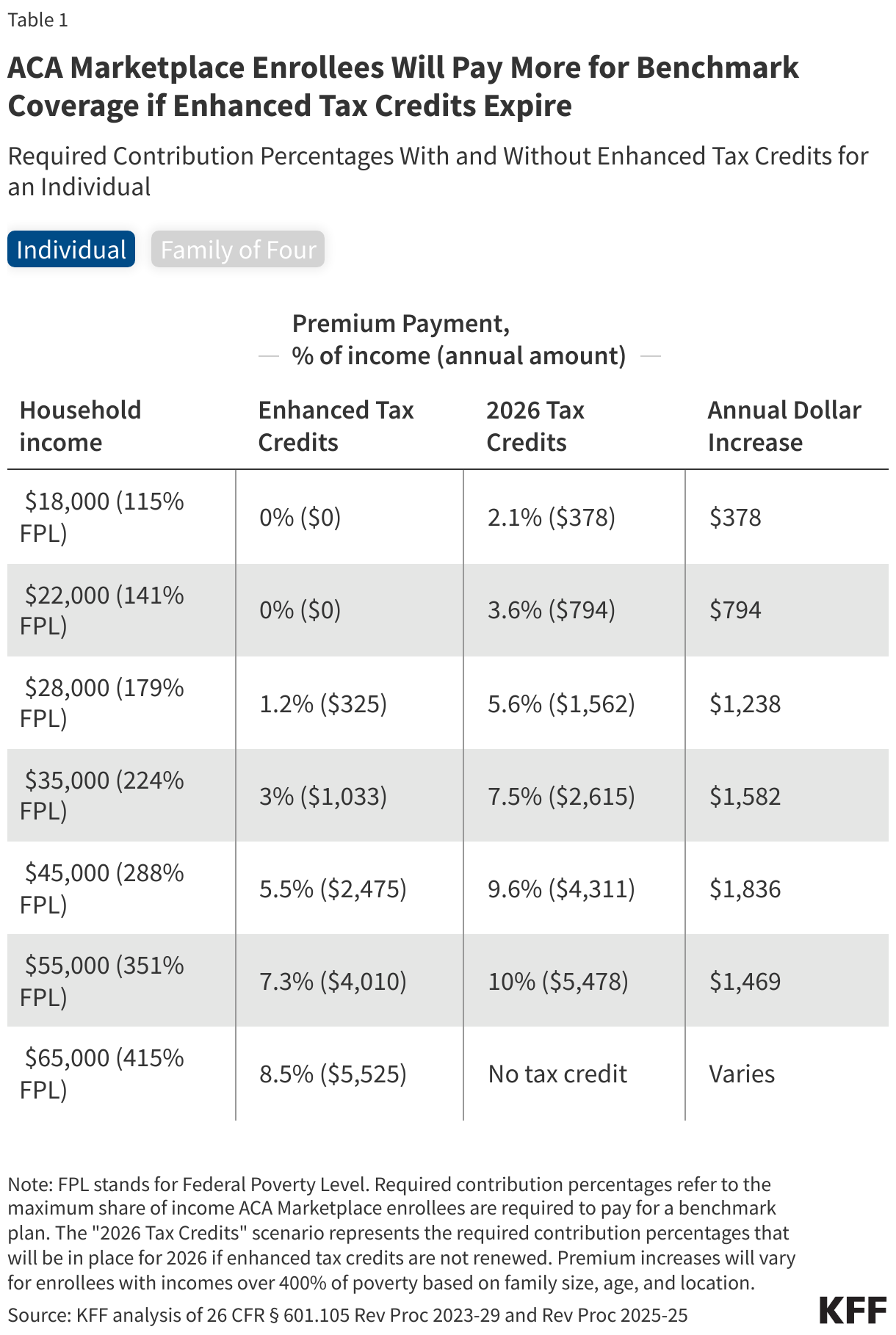

Even if insurer premiums are locked in, Congress can still prevent the vast majority of ACA enrollees from facing higher premium costs. With enhanced premium tax credits, the vast majority (93%) of ACA enrollees currently receive financial help to lower their monthly premium. People who get a tax credit simply pay a certain percent of their income for their premium payment, ranging from 0% to 8.5% on a sliding scale with lower income people paying less and higher income people paying more. The enhanced premium tax credits lower the percent of income people have to pay across the board.

For subsidized enrollees, what they pay each month is not up to insurers, it’s up to Congress.

Conversely, if Congress does not act to extend the enhanced tax credits, a low-income person who currently has a $0 premium plan will soon have to pay about 2-4% of their income each month. A middle-income person might go from paying about 7% of their income to about 10% of their income if the enhanced tax credits expire. This would have been the case whether insurers increased premiums by 18% or 14%.

If Congress doesn’t extend the enhanced tax credits, some people – those with incomes over four times the poverty level, who make up about 1 in 10 ACA enrollees – will be hit both by the loss of the enhanced premiums tax credits and by the higher premium insurers are charging. But if Congress extends the enhanced tax credits, those enrollees will continue to have their monthly costs capped at 8.5% of their income.

In other words, when we say premium payments will go up 114%, most of that increase is just based on a formula set by Congress.

The Congressional Budget Office has estimated that extending the enhanced premium tax credits would cost about $35 billion per year. The higher the premiums, the higher the cost to the federal government.