KFF Follow-Up Survey of Marketplace Enrollees: Following End of Enhanced Credits, Half of Marketplace Enrollees Now Say Costs Are a Lot Higher, Most Expect to Cut Back on Basic Household Expenses to Afford Coverage

One in 10 Dropped Their Marketplace Coverage and Are Now Uninsured and Three in 10 Switched ACA Plans, Most Citing High Costs

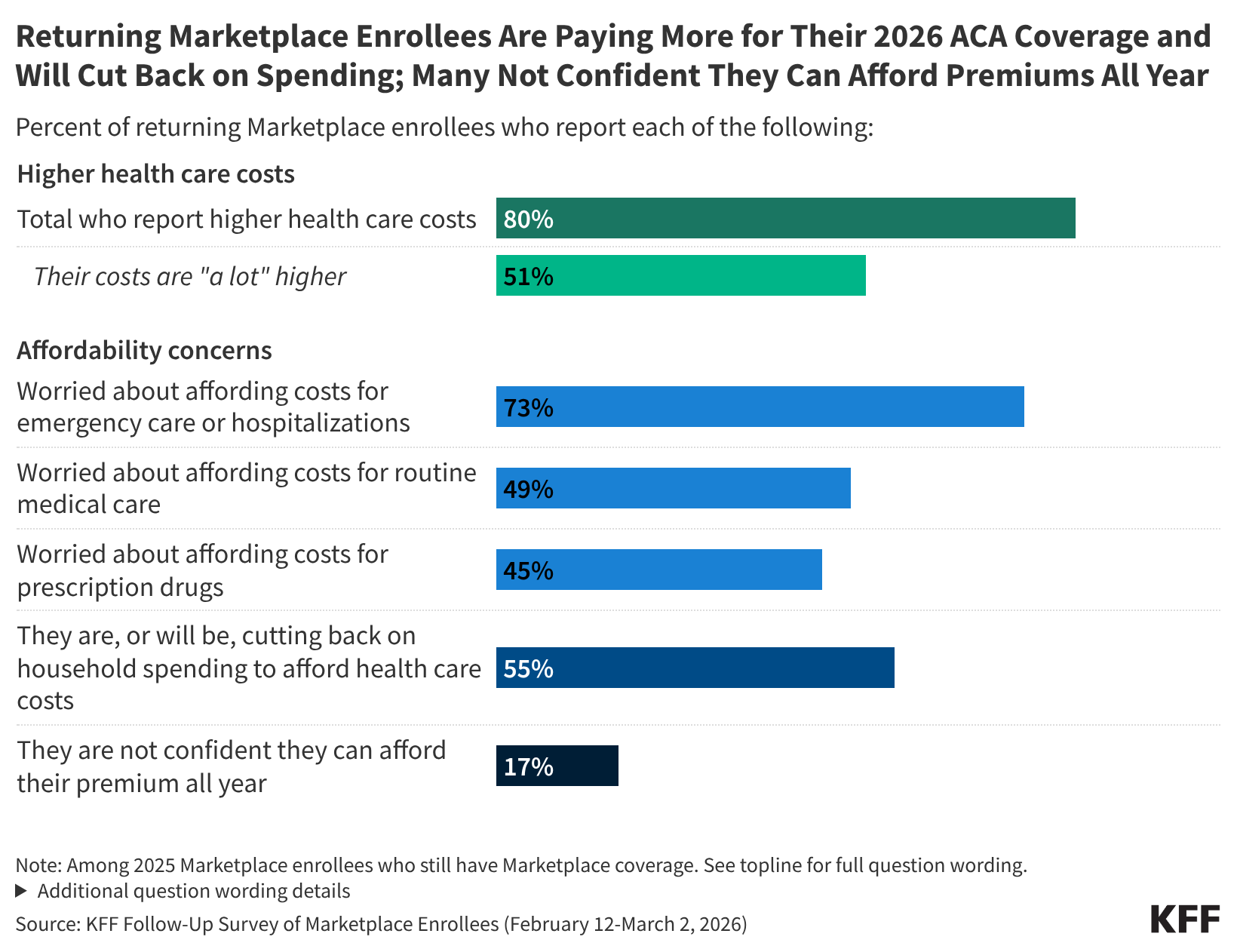

Following the expiration of the enhanced premium tax credits for people with Affordable Care Act (ACA) Marketplace plans, a new KFF follow-up survey of the same Marketplace enrollees KFF surveyed in 2025 finds half (51%) of returning enrollees say their health care costs are “a lot higher” this year compared to last year, including four in 10 who specifically say their premiums are “a lot higher.” In all, a large majority (80%) of these enrollees say their health care costs, which can include premiums, deductibles, co-pays, or coinsurance, are higher.

This new survey, which was fielded about a month after open enrollment ended in most states and before the grace period to make payments ends for many enrollees, re-interviewed Marketplace enrollees who shared their expectations for their coverage decisions late last year. It also finds that nearly one in six (17%) returning ACA Marketplace enrollees say they are not confident they will be able to afford their premiums this year. For those who kept the same Marketplace plans, the expiration of the ACA’s enhanced premium tax credits in 2025 is estimated to have increased annual premium payments by more than two-fold on average this year.

Responding to Rising Health Costs

Among those who re-enrolled in an ACA Marketplace plan, a majority (55%) say they have cut or plan to cut spending on food or other basic household expenses to afford their health care costs. The impact is even greater for those with chronic health conditions, more than six in 10 (62%) of whom say they are, or will be, cutting back on food and other basics.

Marketplace enrollees are also concerned about their ability to pay for both routine and unexpected medical expenses. About three in four (73%) returning Marketplace enrollees say they are “very worried” or “somewhat worried” about being able to afford costs for emergency care or hospitalizations while about half are worried about affording costs for routine medical visits (49%) or prescription drugs (45%).

“The impacts on Marketplace enrollees we see in this follow-up survey will likely get worse as people struggle to make payments and the grace period many have expires,” KFF President and CEO Drew Altman said.

For some, rising costs have already forced them to make tough choices. About one in 10 (9%) Marketplace enrollees dropped their ACA coverage and are now uninsured and another nearly three in 10 (28%) changed Marketplace plans. When asked why they decided to drop or change their coverage, most cited costs.

A 63-year-old man in California describes why he is uninsured now:

“The end of ACA subsidies caused a huge increase in premiums, the cost of which I could not afford.”

A 56-year-old man in Texas explains why he switched to a different Marketplace plan:

“Income exceeded the subsidy limit, forcing us to pay the full cost, so we switched down to a bronze from a gold plan. Even doing that our premiums are 3 times what they were in 2025, with lower plan features and a higher deductible.”

In all, seven in 10 (69%) of those who had ACA Marketplace coverage in 2025 have re-enrolled in a plan through the Marketplace, while others became eligible for different types of health insurance coverage either through an employer (5%) or through Medicare (4%) or Medicaid (7%). A small share (5%) purchased health plans outside of the ACA Marketplace, which typically provide less comprehensive coverage and have fewer consumer protections than Marketplace plans. Even in years with few policy changes, shifts across Marketplace plans or to other types of coverage are normal and often follow changes in employment, income, age, and other life circumstances.

Looking Ahead to the Midterms

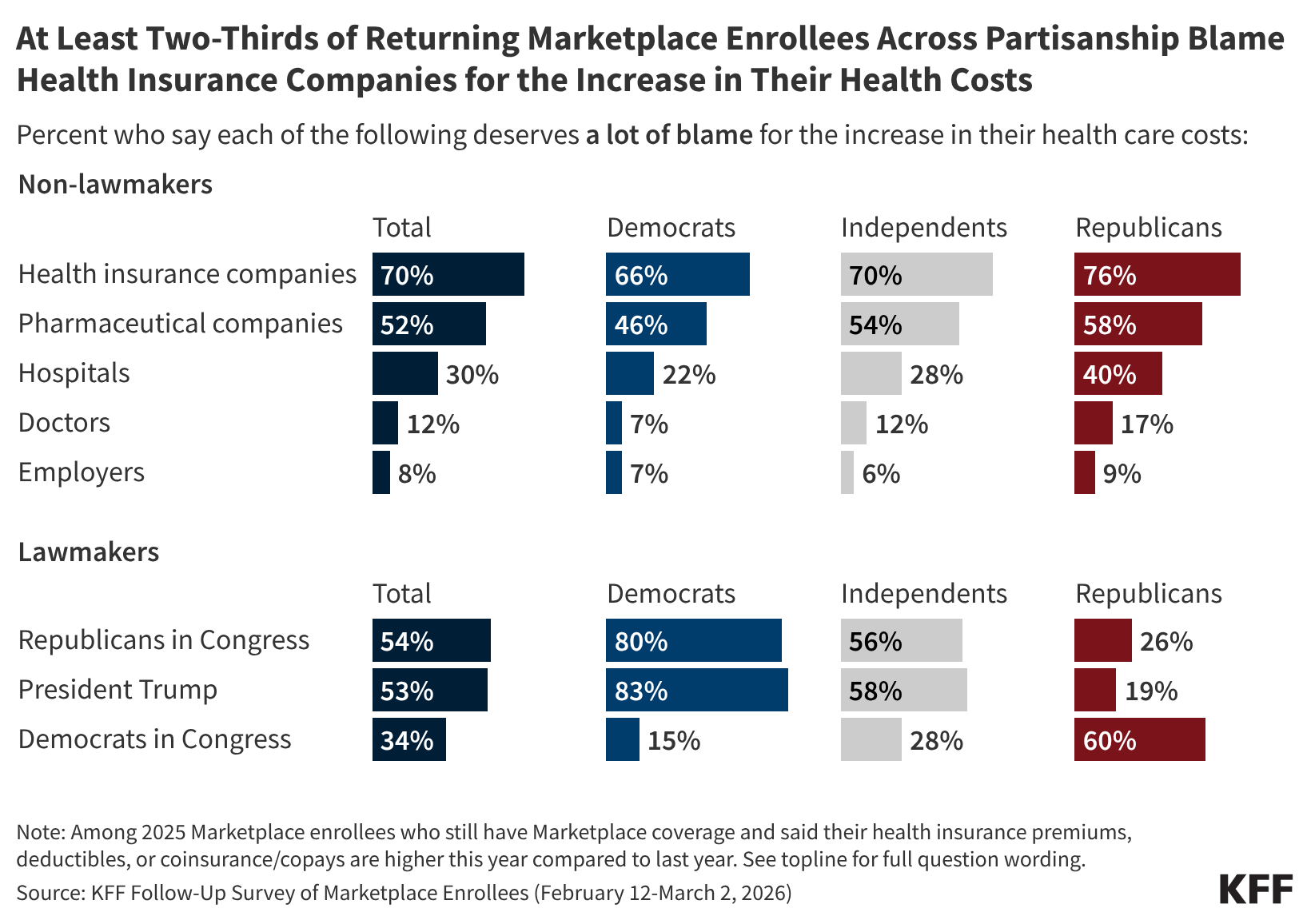

Among returning Marketplace enrollees who saw higher health costs, seven in 10 (70%) blame health insurance companies “a lot” for their increased costs and at least half place “a lot” of blame on congressional Republicans (54%), President Trump (53%), or pharmaceutical companies (52%). While majorities of partisans place “a lot” of blame on lawmakers from the opposite party, independents with Marketplace coverage are more likely to say Congressional Republicans (56%) and President Trump (58%) deserve “a lot” of blame than Congressional Democrats (28%).

Three-quarters of those who had Marketplace coverage in 2025 and are registered to vote say health care costs will affect their decision to vote (73%) and which party’s candidate they will support (74%). Democrats are more than twice as likely as Republicans to say it will have a major impact on their decision to vote (67% vs. 27%) and which candidate they may support (70% vs. 30%). Among independent voters, nearly half say the issue will have a major impact on their decision to vote (47%) and which candidate they will support (44%).

Designed and analyzed by public opinion researchers at KFF, this survey, which builds on a 2025 survey of ACA Marketplace enrollees, re-interviewed more than 80% of the original sample to learn how they are navigating changes to the ACA Marketplace. The survey was conducted February 12-March 2, 2026, online and by telephone, in English and in Spanish, among a nationally representative sample of 1,117 U.S. adults who had ACA Marketplace coverage in 2025 and completed the initial KFF survey. The margin of sampling error is plus or minus four percentage points for the full sample. For results based on other subgroups, the margin of sampling error may be higher.