2025 KFF Marketplace Enrollees Survey

About the Survey

In 2021, during the COVID-19 pandemic, Congress passed the American Rescue Plan Act (ARPA) which temporarily increased tax credits available for adults purchasing their own health insurance through the ACA Marketplace. These enhanced tax credits increased the financial assistance available to existing Marketplace enrollees who already qualified for financial help and extended financial assistance to some middle-income adults who were previously not eligible for premium tax credits. The tax credits were extended as part of the 2022 Inflation Reduction Act and are set to expire at the end of 2025.

If Congress does not extend the tax credits beyond 2025, premium payments will increase 114% on average for the 22 million people who currently get a tax credit. To better understand how people are navigating these cost increases during the 2026 Open Enrollment period, which began on November 1st, KFF conducted a probability-based survey of 1,350 adults who purchase coverage on the ACA Marketplaces.

This report highlights their expectations for their health insurance coverage and costs for 2026, as well as how increased health care costs may affect their coverage decisions, finances, and their political preferences in the coming elections.

Findings

Key Takeaways

- Marketplace enrollees largely see health insurance as very important to their ability to access care, to their financial well-being, and to their peace of mind; however, if the enhanced premium tax credits are not extended, many of the twenty-four million adults in the U.S. who currently buy their own insurance through the ACA Marketplace may consider changes to their current coverage. When asked what they would do if the amount they pay for health insurance each month doubled, one in three enrollees (32%) say they are very likely to shop for a lower-premium plan (with higher deductibles and out-of-pocket costs) and one in four (25%) say they would be very likely to go uninsured.

- Notably, with Congress potentially voting on extending the premium tax credits in December and recent discussions about a Republican health care proposal, the vast majority of enrollees (89%) expect to make a decision about the 2026 coverage by the end of the year, including many enrollees who say they have already made their decision.

- Many Marketplace enrollees are already struggling with health care costs. Six in ten adults (61%) who buy their health coverage on the ACA Marketplace say it is very or somewhat difficult to afford their deductibles and out-of-pocket costs for medical care and half (51%) say it is difficult to afford the cost of health insurance premiums each month. In addition, nearly six in ten Marketplace enrollees say they would not be able to afford an annual increase of $300 in health care expenses without significantly disrupting their household finances.

- The enhanced premium tax credits allow most Marketplace enrollees to pay less than the full price of their health insurance premiums, and the poll finds bipartisan support among Marketplace enrollees for Congress to extend these tax credits even as the political parties in Congress disagree about the way forward. More than eight in ten (84%) Marketplace enrollees – including nearly all Democrats and about seven in ten Republicans – say Congress should extend the tax credits. If the tax credits are allowed to expire, most enrollees who want to see the credits extended think either President Trump (41%) or Congressional Republicans (35%) deserve most of the blame.

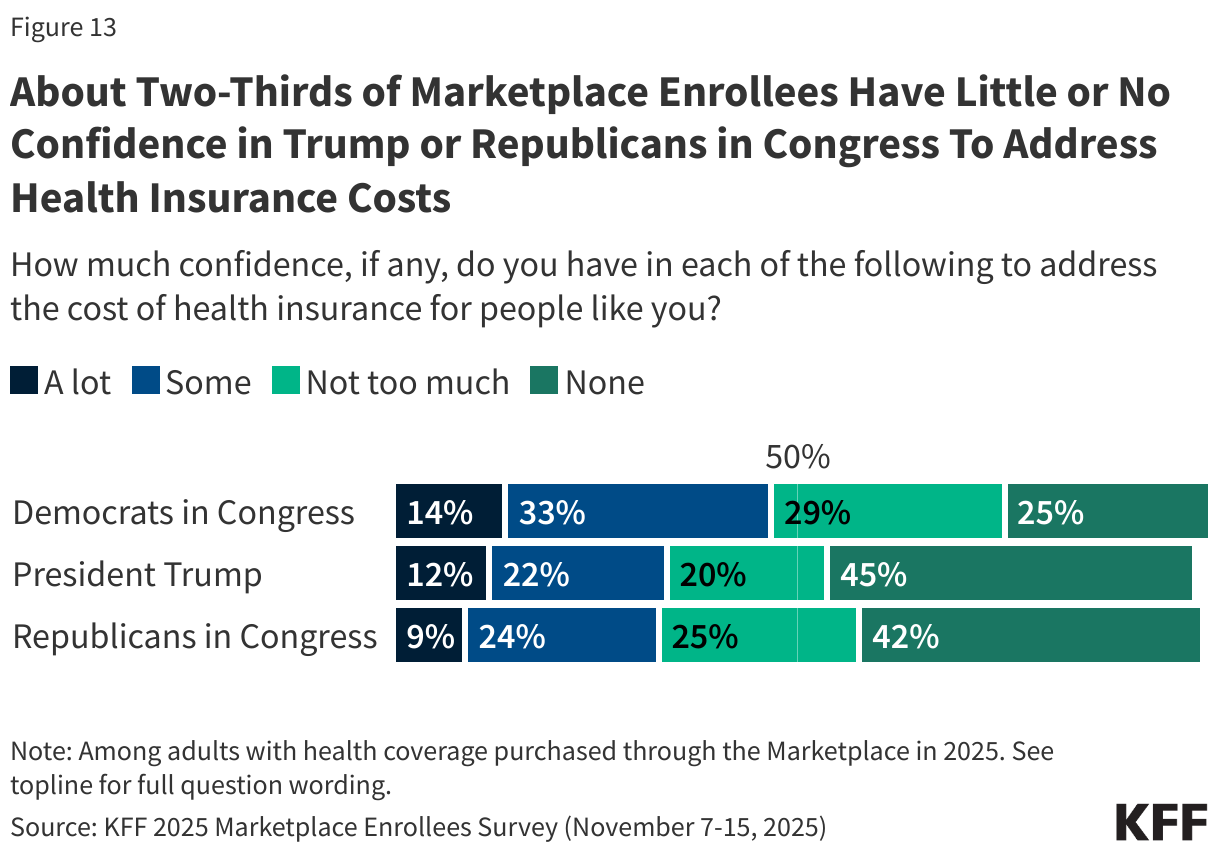

- Following the longest federal government shutdown in U.S. history, which ended without an extension of the enhanced premium tax credits, about two-thirds of Marketplace enrollees say they have either “not much” or “no confidence” in President Trump, nor in Congressional Republicans, to address health care costs for people like them. Congressional Democrats fare slightly better, but still more than half of enrollees say they lack confidence in Congressional Democrats to address this issue.

- Regardless of whether Marketplace enrollees decide to continue with their current Marketplace plan, switch to a lower-premium but higher-deductible plan, or go uninsured in 2026, many will face higher health care expenses next year and many say this increased financial burden will impact how they approach the 2026 midterm election. A slight majority (54%) of enrollees who are registered to vote say if their health care expenses increase by $1,000 next year, it would have a major impact on whether they will vote in the 2026 elections and about half (52%) say it would have a major impact on which party’s candidate they will support.

Most Enrollees Are Wary About Expiring Enhanced Premium Tax Credits

Open enrollment for the ACA Marketplace began on November 1st amid a government shutdown as Congress debated extending the tax credits. The survey, conducted in the first weeks of open enrollment and as Congress passed a short-term spending bill, finds that the focus on the enhanced premium tax credits has resonated with most Marketplace enrollees. At the time the survey was fielded in mid-November, about six in ten Marketplace enrollees say they’ve heard “a lot” (27%) or “some” (32%) about the enhanced premium tax credits. However, four in ten enrollees say they have heard “a little” (22%) or “nothing at all” (19%) about the enhanced premium tax credits. In most states, open enrollment for ACA Marketplace plans ends on January 15th, 2026.

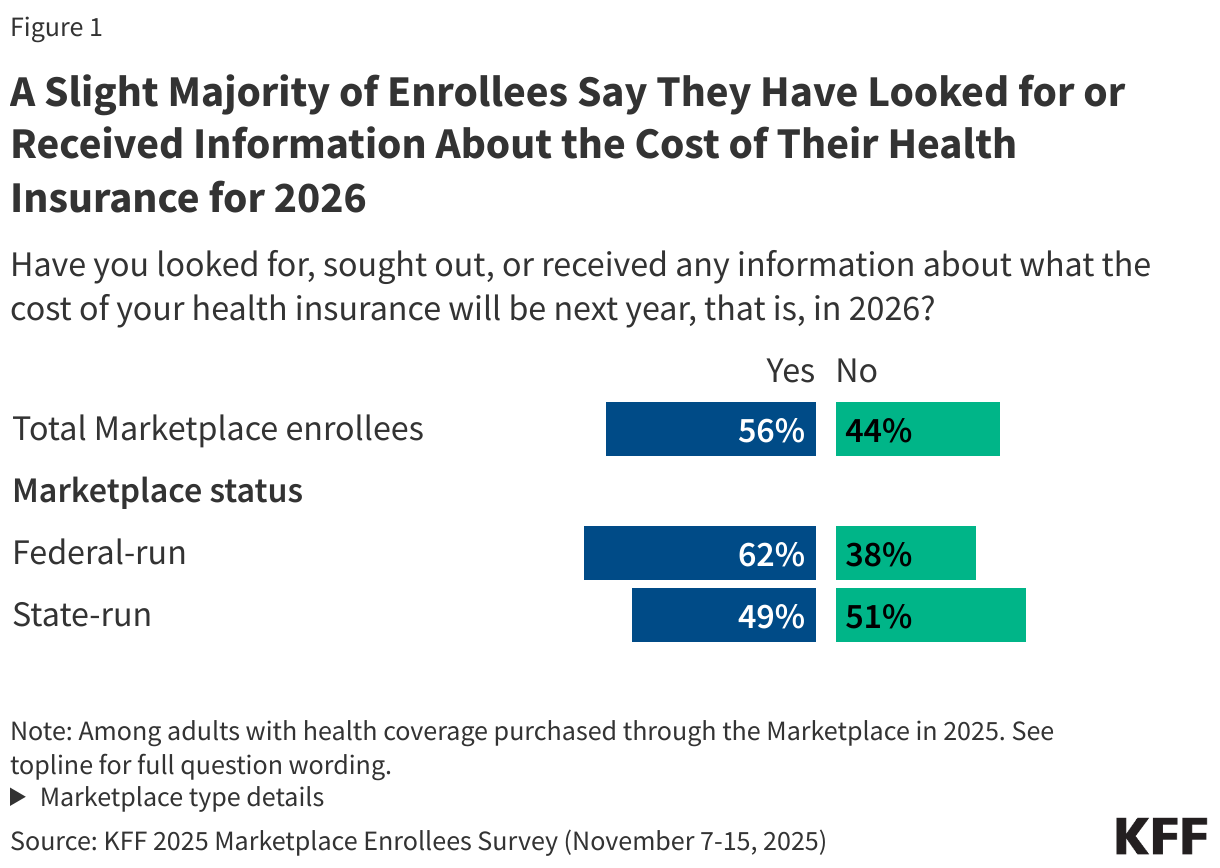

As of mid-November, a slight majority (56%) of enrollees say they have looked for, sought out, or received any information about what the cost of their health insurance will be in 2026. Enrollees in states that use the federal ACA Marketplace platform are more likely than those in states that have a state-run Marketplace to say they have looked for or received information about the cost of their health insurance for next year (62% vs. 49%).

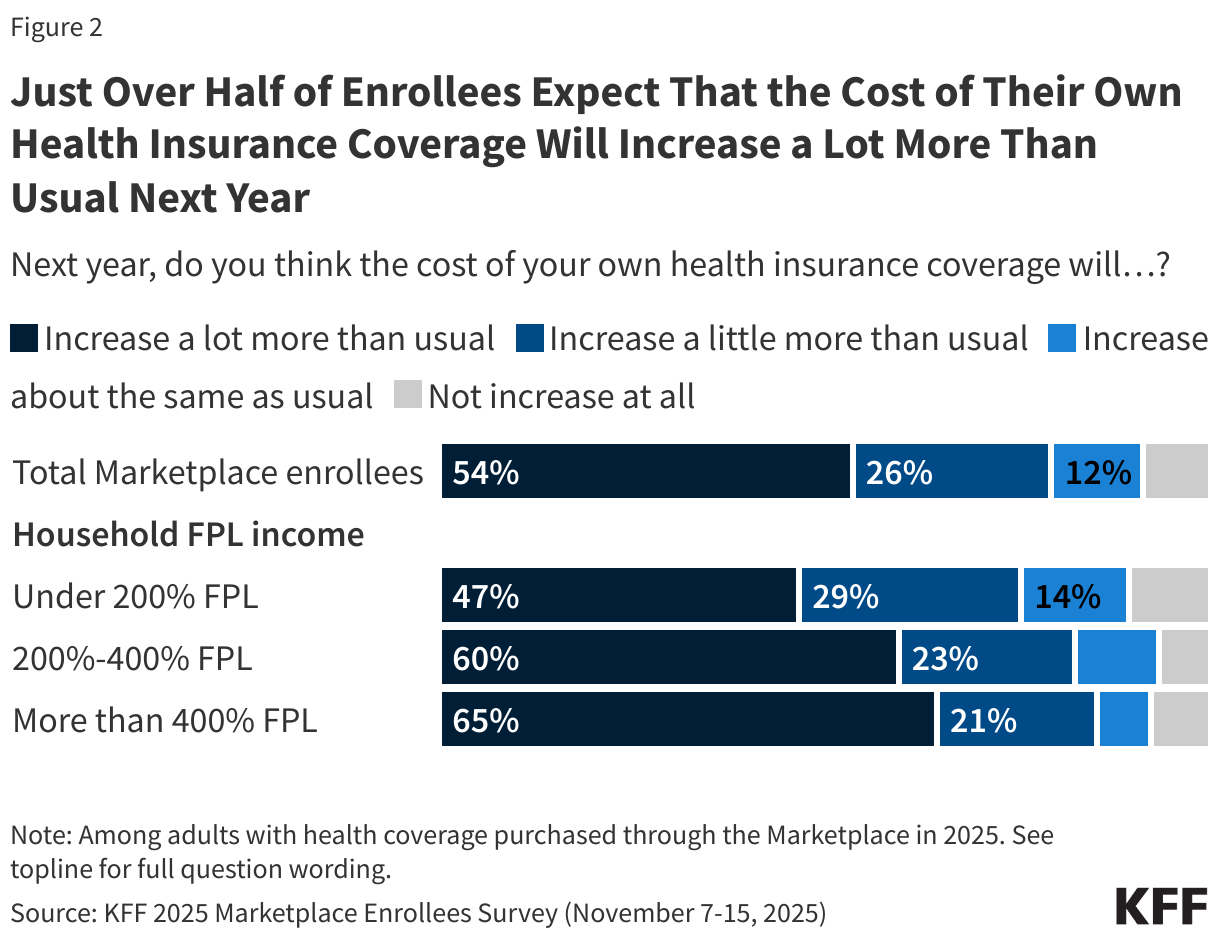

More than half of Marketplace enrollees (54%) expect that the cost of their health insurance coverage for next year will “increase a lot more than usual.” A further one in four (26%) expects it to increase a “little more than usual,” while fewer expect their health insurance costs to “increase about the same as usual” (12%) or to “not increase at all” (8%). Enrollees with higher incomes are somewhat more likely than those with lower household incomes to expect their costs to increase “a lot more than usual.” Notably, Marketplace enrollees with an income just above 400% of the federal poverty level (FPL), who currently pay no more than 8.5% of their income in monthly insurance premiums, would have to pay full price for their insurance coverage if the enhanced premium tax credits are allowed to expire.

Half or more across partisans and geographies expect the cost of their health insurance for next year to increase “a lot more than usual,” including 60% of Democrats, 52% of Republicans, 54% of independents, 53% of enrollees living in states that have expanded Medicaid, and 56% of enrollees living in states that have not expanded Medicaid.

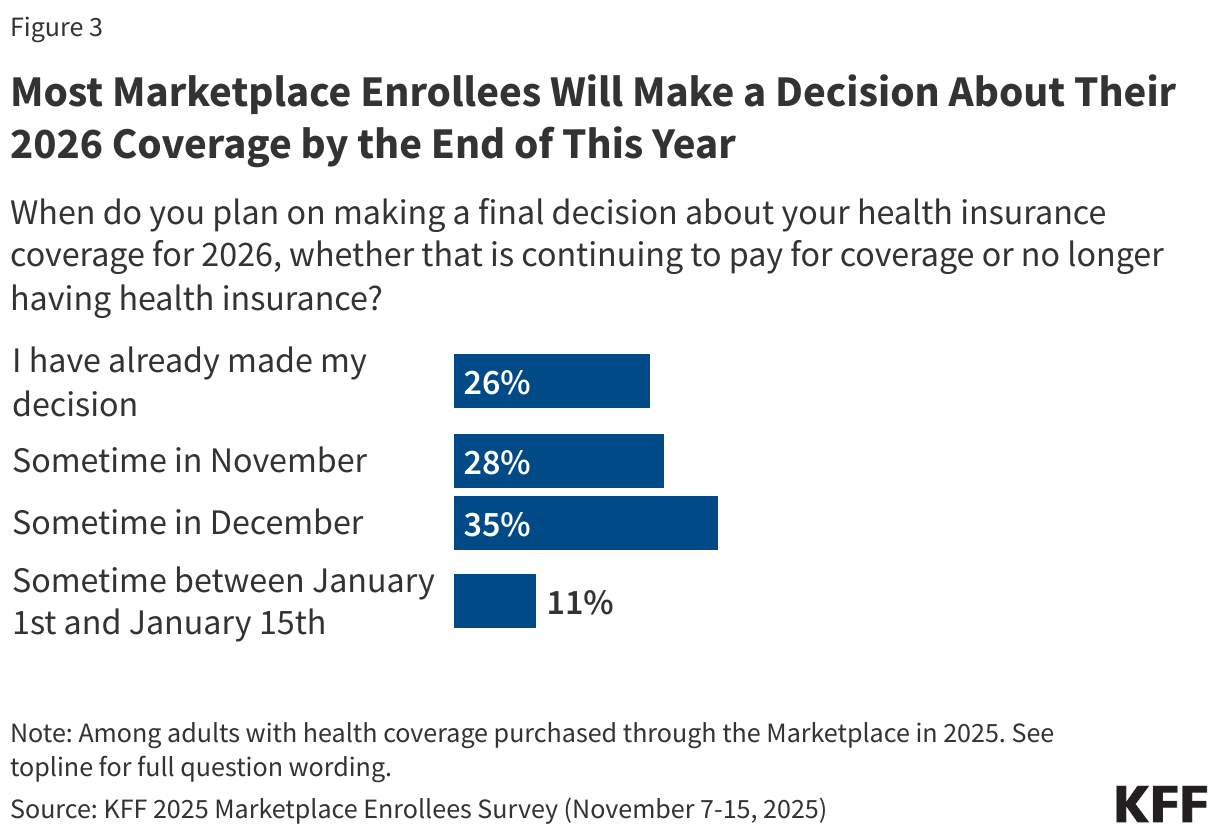

About nine in ten (89%) Marketplace enrollees say they will make a decision about their coverage for 2026 this year, including one in four (26%) who say they have already made a decision about their health insurance coverage for next year and 28% who planned to make a decision sometime in November. Enrollees must generally select a plan or be automatically reenrolled by December 15 for coverage to start on January 1, 2026. About a third (35%) of enrollees say they plan to make their health insurance decision in December, while one in ten (11%) say they plan to decide in early January.

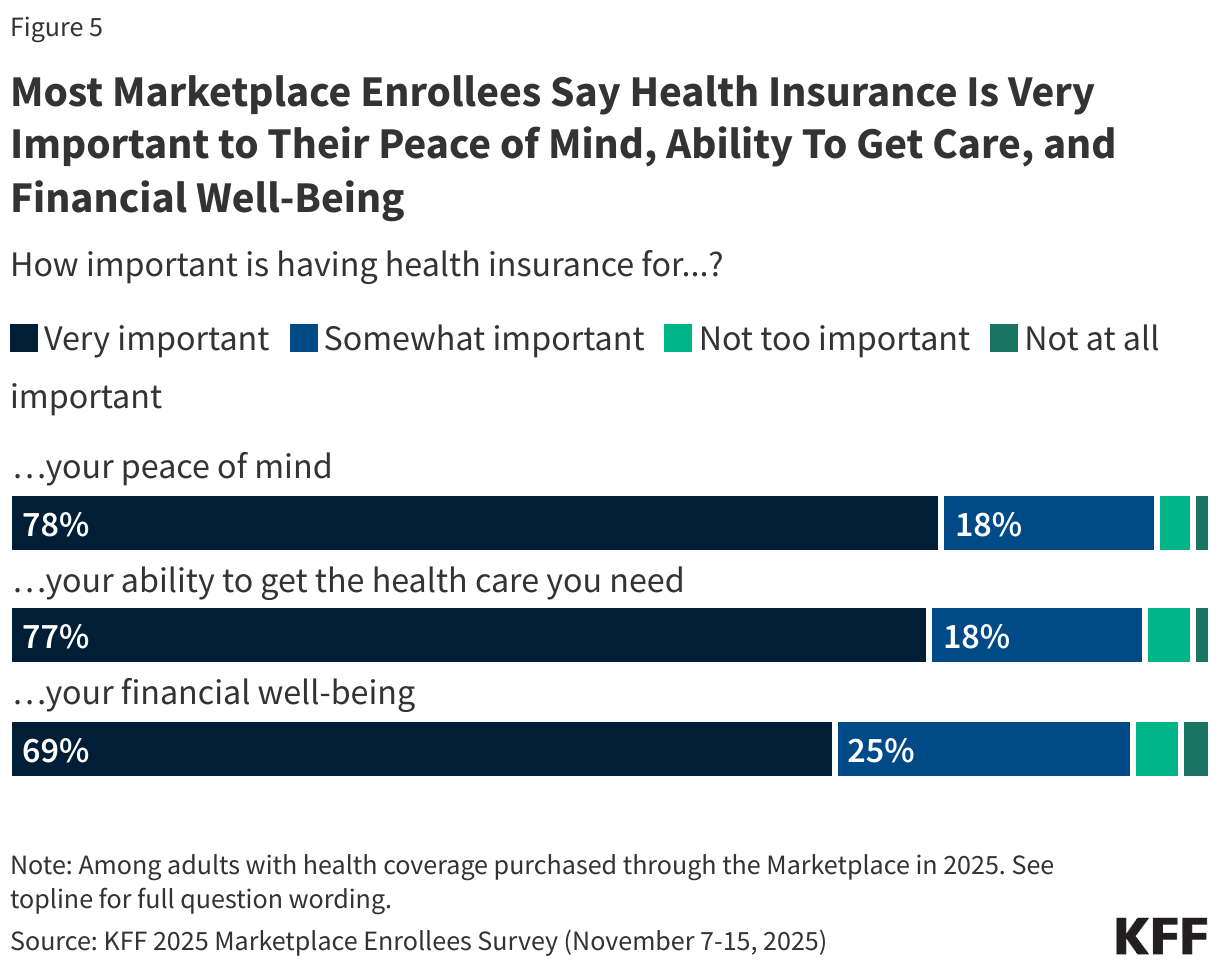

Most Enrollees See Health Insurance as Very Important – Particularly Those Ages 50 and Older

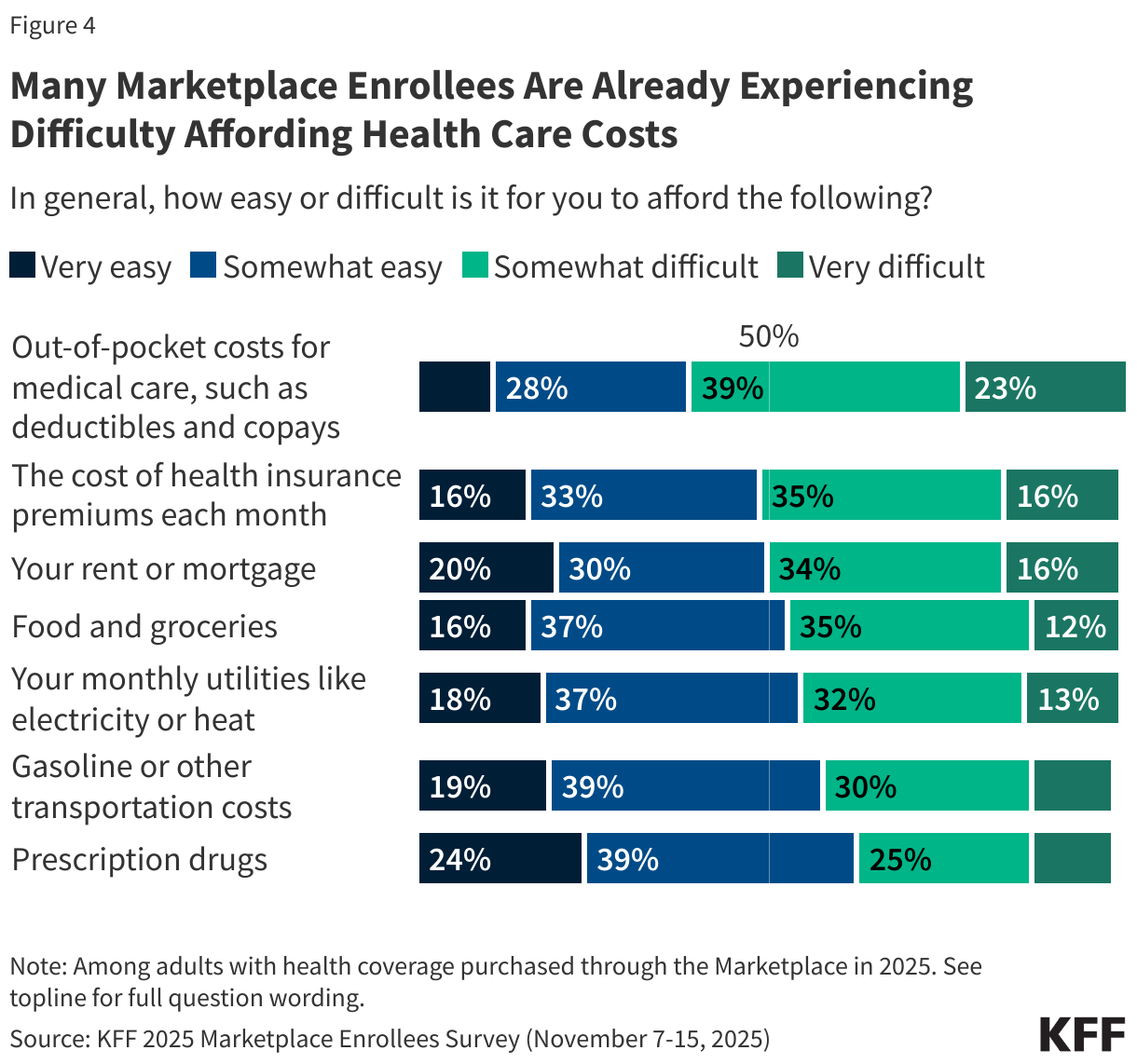

Even with the current financial help provided by the enhanced premium tax credits, many Marketplace enrollees are already struggling to afford health care costs. About six in ten (61%) Marketplace enrollees say it is very difficult or somewhat difficult for them to afford out-of-pocket costs for medical care, and about half (51%) say they already have difficulty affording their health insurance premiums. Out-of-pocket costs for medical care ranks as the top household budget item that Marketplace enrollees find difficult to afford – ranking ahead of rent or mortgage, food and groceries, utilities, and housing costs.

Yet, health insurance is a clear priority for Marketplace enrollees. More than three in four say having health insurance is “very important” for their ability to get the health care they need (77%) and for their peace of mind (78%). About seven in ten (69%) say it is “very important” for their financial well-being. Notably, enrollees between the ages of 50 and 64 – a group that does not yet qualify for Medicare but may have additional age-related health care needs – are more likely than younger enrollees to say that health insurance is very important to accessing needed health care, to their financial well-being, and to their peace of mind. A majority of Marketplace enrollees, regardless of partisanship, say that health insurance is “very important” to their financial wellbeing, their peace of mind, and their ability to access health care.

Expiring Premium Tax Credits May Make Coverage Unaffordable for Most Marketplace Enrollees

Nine in ten Marketplace enrollees (90%) expect that the expiration of the enhanced premium tax credits will have an impact on the amount they pay monthly for their health insurance, including seven in ten (69%) who say it will have a “major impact.” KFF analysis has found that if the enhanced premium tax credits for adults who purchase their own insurance through the ACA Marketplace are not extended, the annual amount that enrollees pay for their premiums for 2026 will more than double on average.

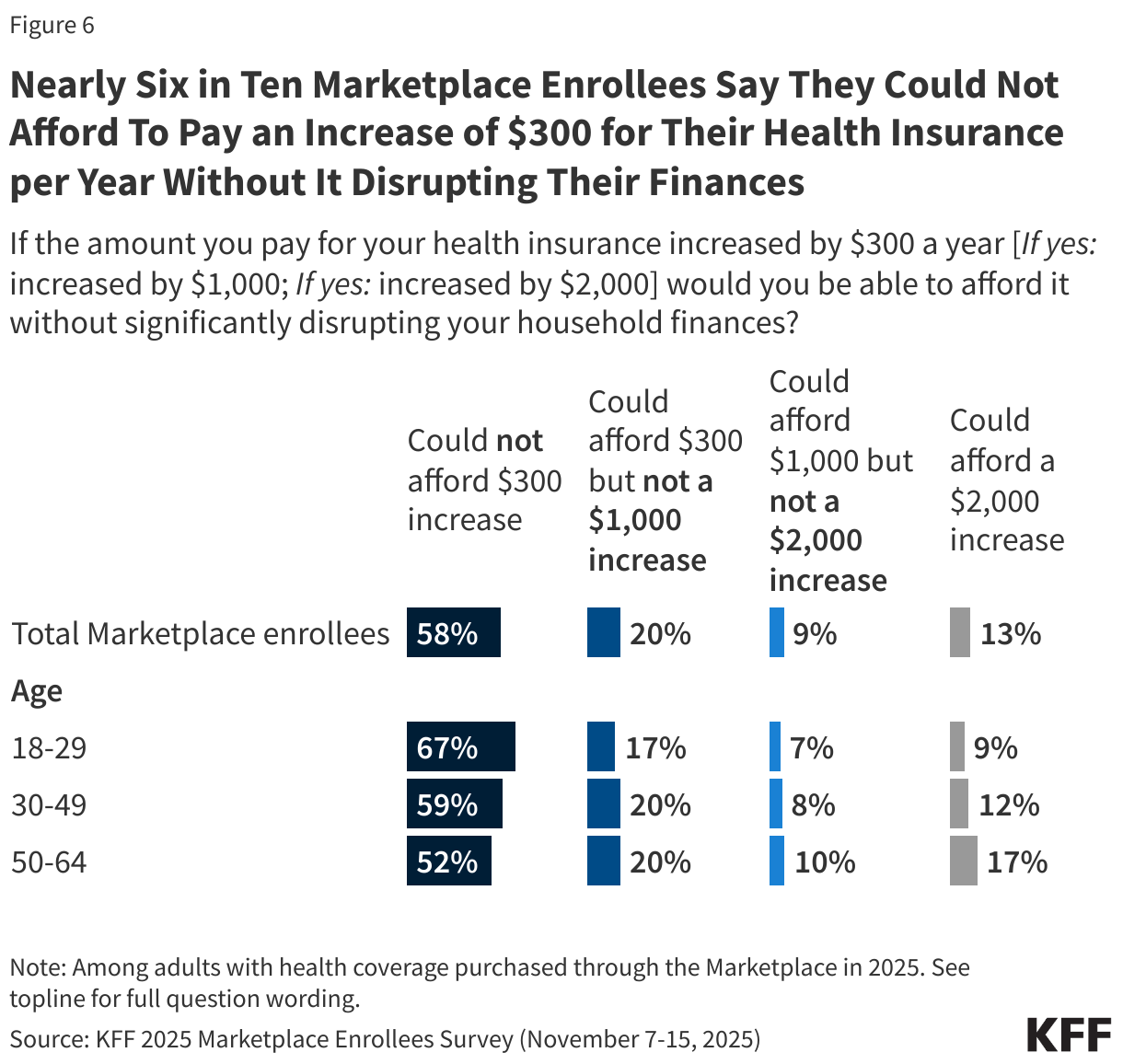

The KFF 2025 Marketplace Enrollees Survey finds that this type of increase could have a significant impact on the household finances of the millions of adults who purchase their own insurance through the ACA Marketplaces. Nearly six in ten enrollees (58%) say they would not be able to afford an increase of just $300 per year in the amount they pay for insurance without significantly disrupting their household finances. Those with lower incomes are likely to see smaller dollar increases in their premium payments, yet notably seven in ten (70%) enrollees with household incomes under 200% FPL say they wouldn’t be able to afford a $300 increase in the amount they pay each year, which is the approximate increase for a low income person to keep a “silver plan” if the enhanced premium tax credits expire.

If enrollees said they could afford an annual increase of $300, they were then asked about their ability to afford larger annual increases. A further 20% of enrollees say they would be unable to afford an increase of $1,000 per year, the average projected increase, without significant financial disruption. Only one in eight Marketplace enrollees (13%) say they could afford an increase of $2,000 or more (which some people would face).

Younger adults are less likely to be able to afford any increase, including two-thirds (67%) of adults ages 18 to 29 who say they would not be able to afford a $300 annual increase without disrupting their household finances. ACA Marketplace insurers have expressed concern that the expiring tax credits will lead to younger, healthier people disproportionately dropping their coverage, and are therefore raising premiums more than they otherwise would.

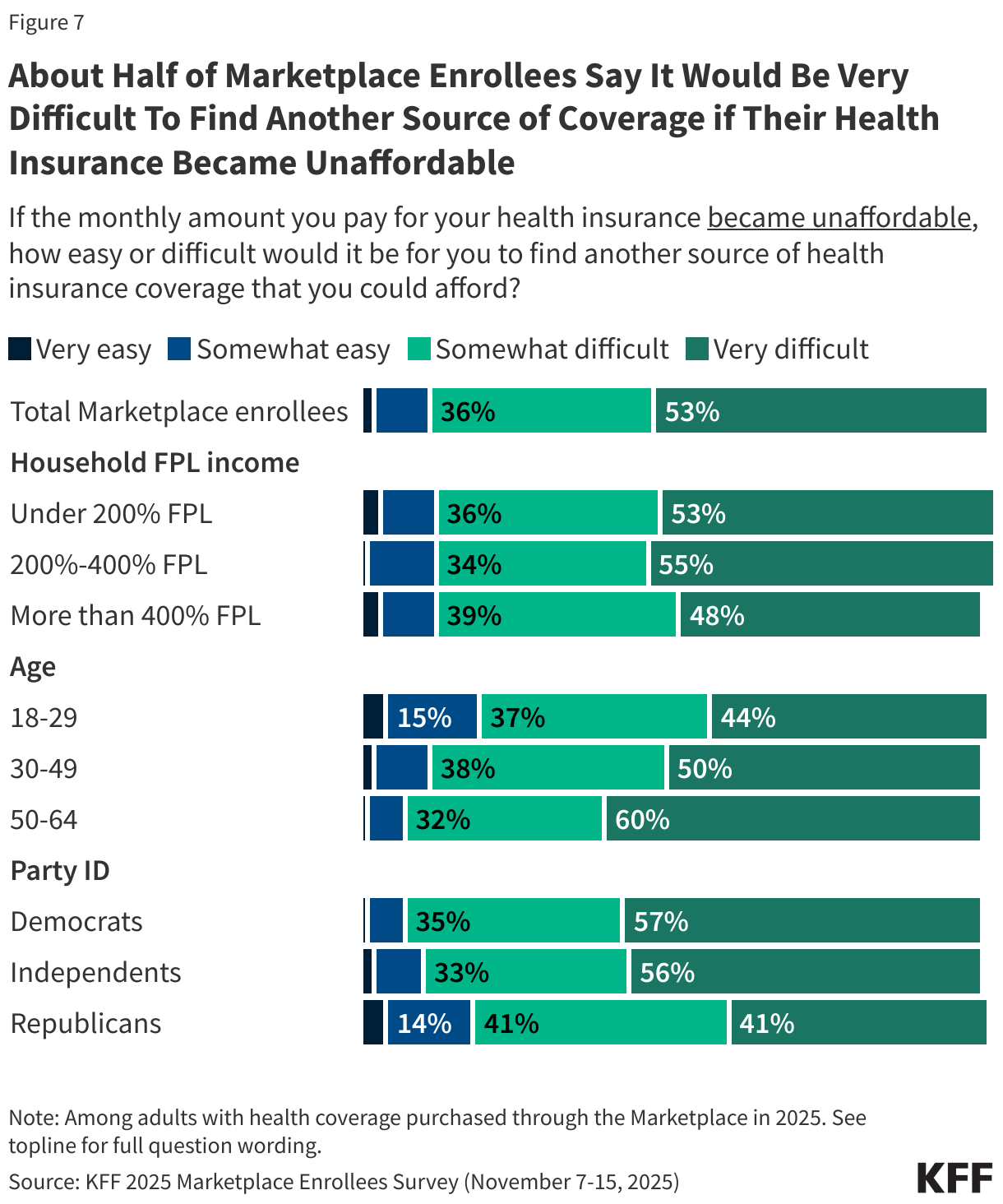

About half of Marketplace enrollees (53%) say it would be “very difficult” for them to find another source of health insurance they could afford if their current coverage became unaffordable, and a further 36% say it would be “somewhat difficult.” Majorities of enrollees, regardless of their household income or age, say it would be at least somewhat difficult to find another source of health insurance coverage.

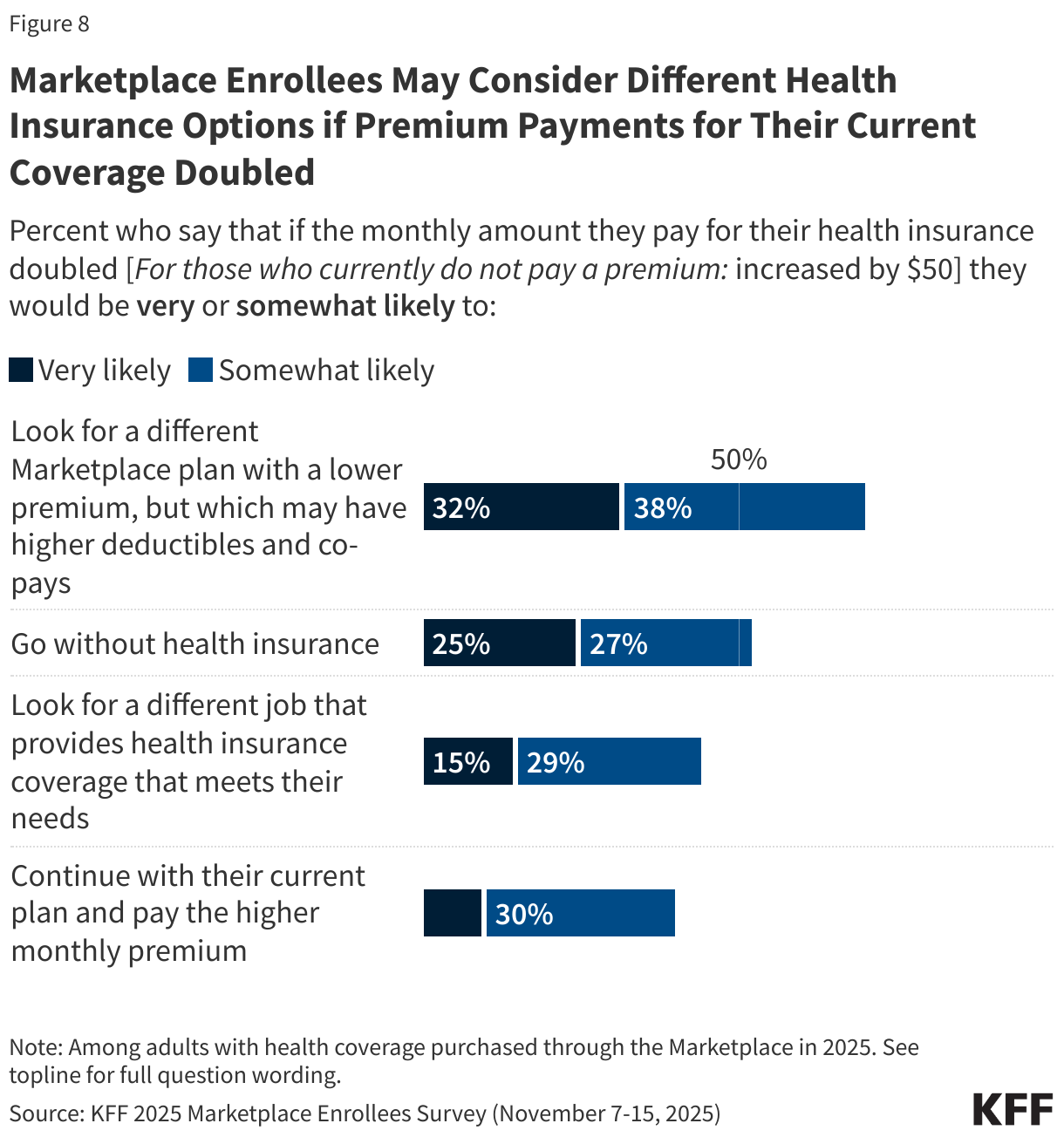

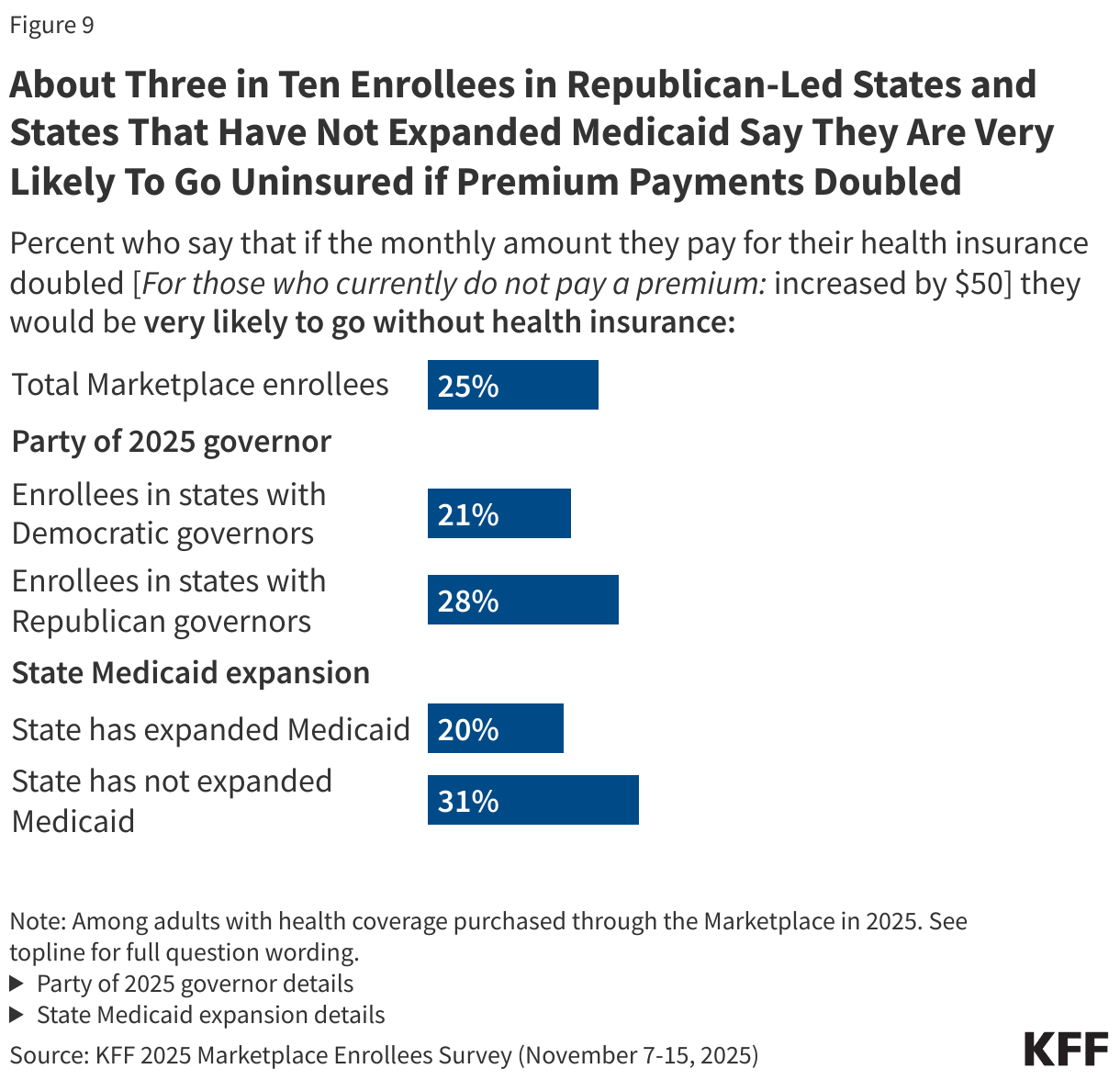

Marketplace enrollees may respond to a projected increase in premiums in different ways. If the monthly amount enrollees pay for their health insurance doubled (or increased by $50 for those who currently do not pay a premium), about a third (32%) say they would be “very likely” to look for a different Marketplace plan with a cheaper premium, but higher deductibles and co-pays. A quarter of enrollees (25%) say they would be “very likely” to go without health insurance. About one in seven (15%) say they would be “very likely” to look for a different job that provides health insurance that meets their needs and only 10% say they are “very likely” to stay with their current insurance plan if their monthly premium payments doubled.

Notably, about three in ten (28%) Marketplace enrollees from states with current Republican governors say they are “very likely” to go uninsured if the monthly amount they pay for health insurance doubles, as expected on average, if the tax credits are not extended. Among Marketplace enrollees in states that have not expanded Medicaid coverage under the ACA, where more people with incomes just above the poverty level are eligible to enroll in Marketplace coverage with premium tax credits, three in ten (31%) say they are very likely to go uninsured if faced with a doubling of their monthly health insurance premiums.

In Their Own Words: Why some current Marketplace enrollees aren’t planning on buying health insurance coverage for 2026

“Without the subsidies, my monthly premiums will increase by nearly $750 a month, or $9000 for the year. My budget is tight as it is, and there’s no way I can afford that additional hit. The only way I will be able to continue with my health insurance is if Congress restores the subsidies.” — 63-year-old man, Democrat, California

“I was paying $0 then it went up to over $600 for 2026. My husband has to continue coverage in order to avoid going blind. I’m going to drop myself off the coverage and just have insurance for him so he can continue to work and pay for the insurance.” — 60-year-old woman, Republican, Missouri

“We cannot afford it. Our premium went from being $25 with subsidy to $300 for the same plan. With everything increasing in price like groceries, we simply cannot afford it” — 39-year-old woman, Democrat, Oklahoma

“Premiums are too high for my usage, will switch to cost sharing like medishare or Samaritans” — 42-year-old woman, Republican, North Carolina

“The cost of the same plan is going to be exponentially higher than the current plan and I would have to go with a “bronze” plan in order to be able to keep my premiums somewhat reasonable.” — 54-year-old woman, Democrat, Texas

“Way too expensive. There was a $231 increase in the premium!” — 46-year-old woman, independent, Indiana

“If subsidies are not extended, I can’t afford it.” — 56-year-old man, independent, Nevada

“I cannot afford the premium increase for the incredibly bad insurance.” — 55-year-old man, Republican, Idaho

How a $1,000 Annual Increase Would Affect Marketplace Enrollees

Regardless of what they decide to do about their health insurance coverage for next year, the vast majority of current Marketplace enrollees are likely to face an increase in their overall health care expenses in 2026. Those who choose to stay with their current insurance plan may face substantial premium payment increases, those who switch to a lower-premium plan will likely face increased out-of-pocket costs through higher deductibles and co-pays, and those who go uninsured may face costly medical bills if they need care.

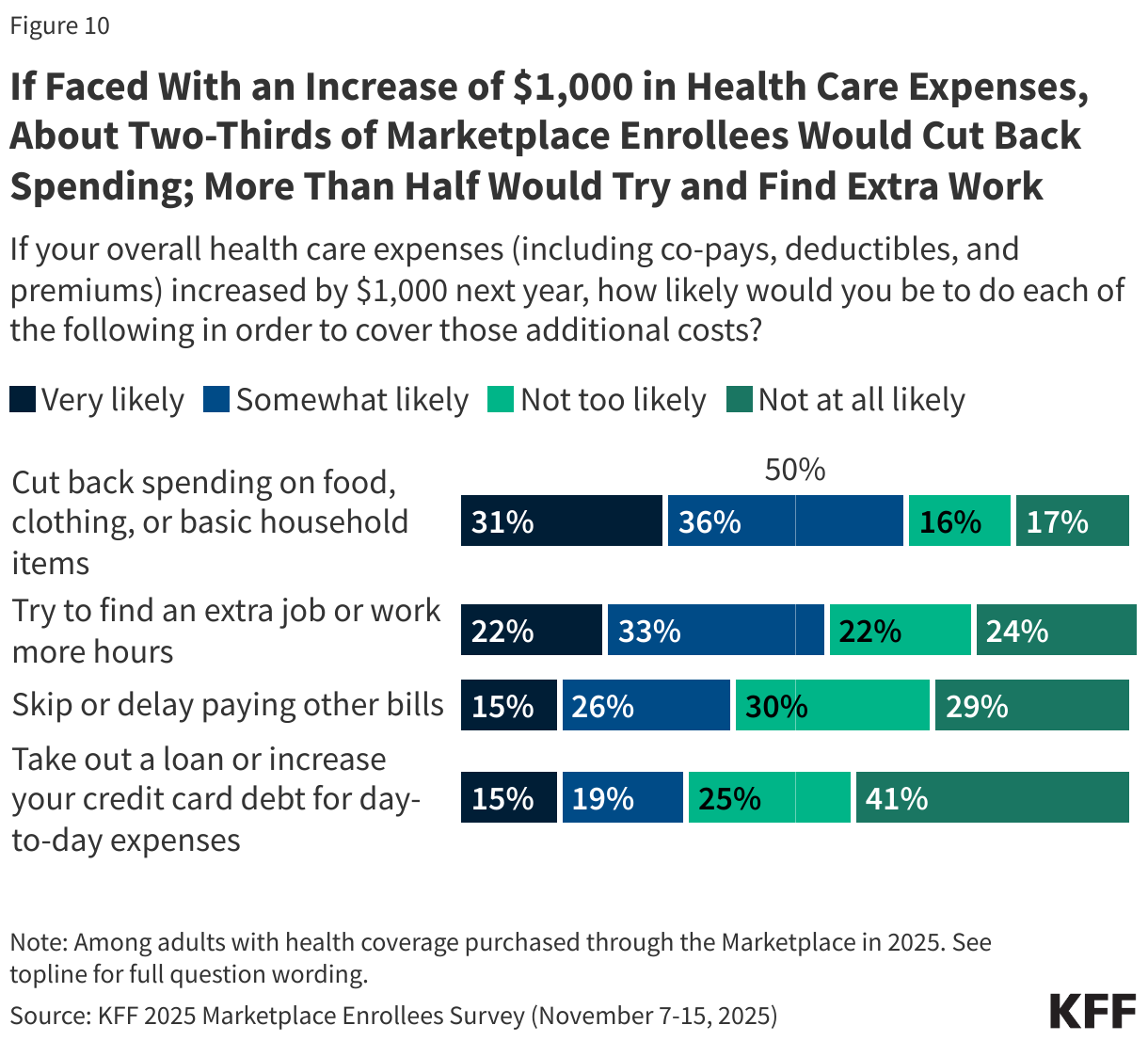

If faced with an annual increase of $1,000 in health care expenses, most Marketplace enrollees (67%) say they are very or somewhat likely to cut back spending on food, clothing, or basic household items in order to cover additional health care costs. More than half (54%) say they would be very or somewhat likely to try to find an extra job or work more hours to cover an increase in health care expenses. About four in ten (41%) say they would skip or delay paying other bills and about a third (34%) say they would take out a loan or increase their credit card debt for day-to-day expenses if faced with an increase of $1,000 in health care expenses.

Assessing the Political Implications of Failing To Extend the Tax Credits

On October 1st, the federal government was shut down when Democratic senators attempted to negotiate a vote for continued government funding in exchange for the extension of the enhanced premium tax credits for adults who purchase their own insurance through the ACA Marketplace. As part of a deal to end the recent federal government shutdown, Republican Congressional leaders have promised Democrats a vote on the ACA Marketplace enhanced premium tax credits in December.

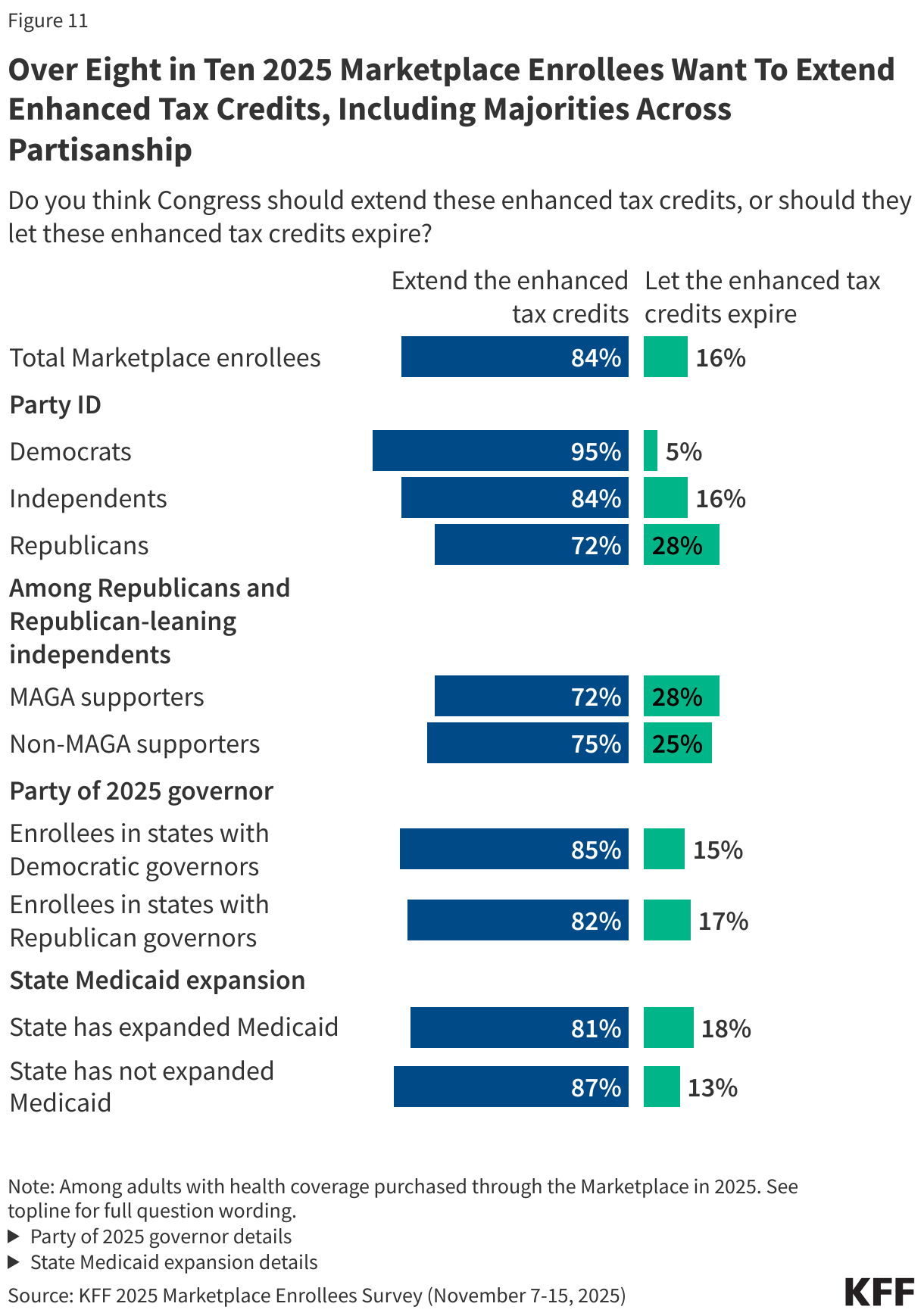

More than eight in ten (84%) Marketplace enrollees say that Congress should extend the enhanced tax credits, while one in six (16%) think they should let the tax credits expire. Majorities across partisanship want to extend the enhanced premium tax credits, including nearly all Democrats (95%), about eight in ten independents (84%), and about seven in ten Republicans (72%) enrolled in Marketplace plans. About seven in ten (72%) Republicans or Republican-leaning independents who support the MAGA movement and get insurance through the Marketplaces want to extend the credits, while about three in ten (28%) want to let them expire. Majorities of Marketplace enrollees, regardless of where they live, including those living in states that haven’t expanded their Medicaid programs or living in states with Republican governors, want to see Congress extend these tax credits.

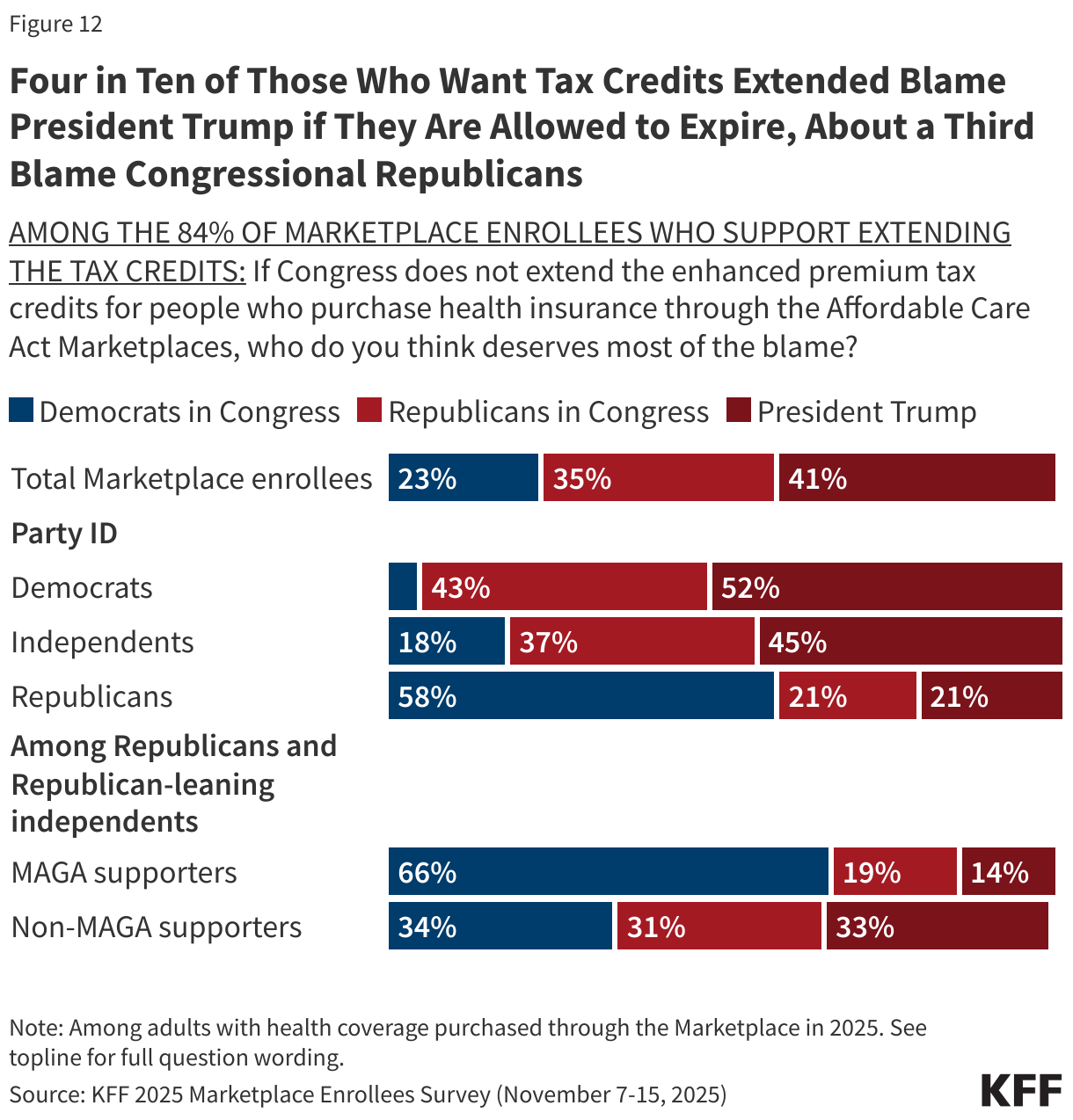

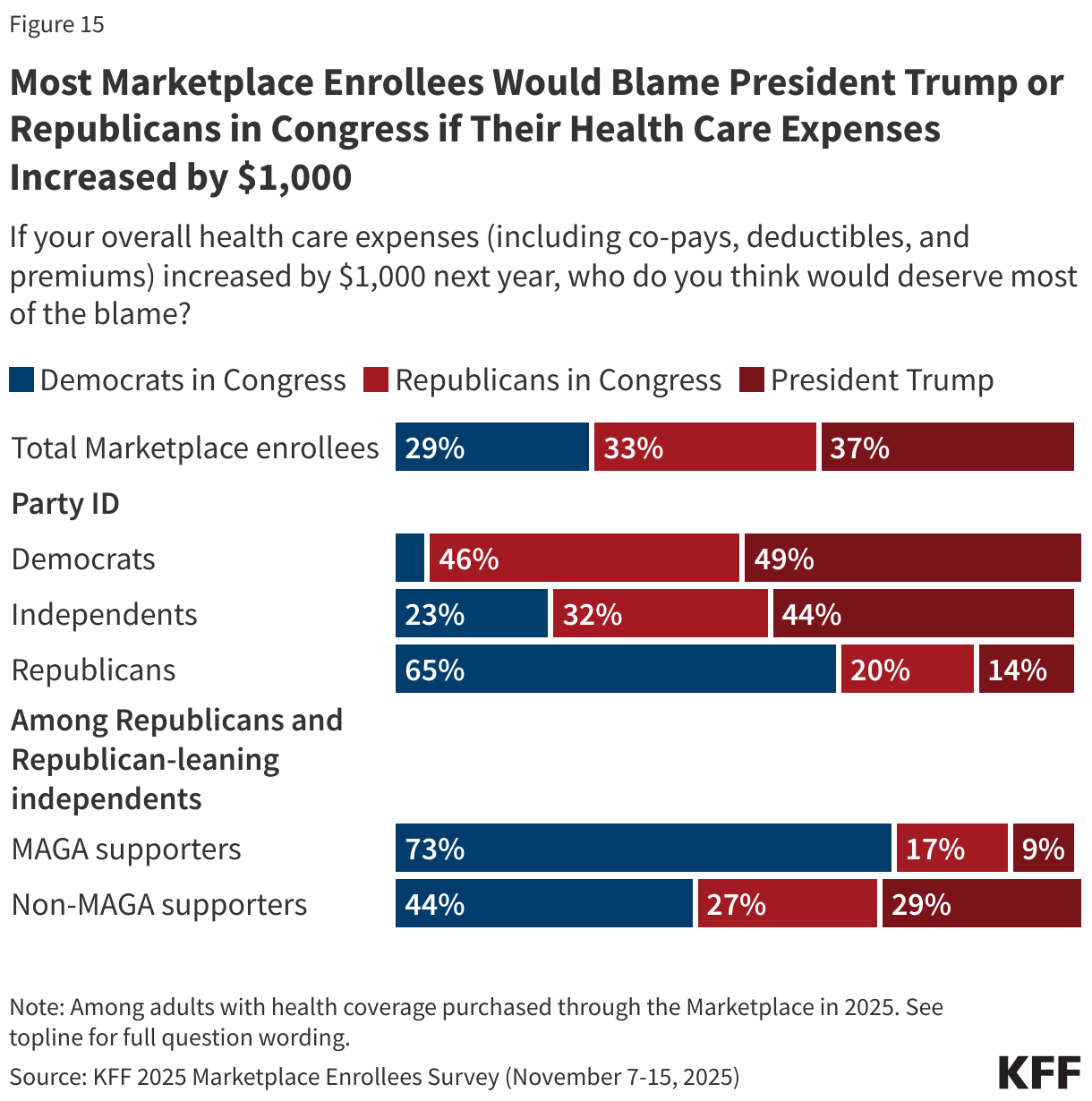

If the enhanced premium tax credits are not extended, those who want to see them extended are most likely to blame Republican leaders, including President Trump. Four in ten of those who support extending the premium tax credits say that if they are not extended, President Trump deserves most of the blame (41%, or 34% of all Marketplace enrollees) and about a third (35%, or 29% of all enrollees) say Republicans in Congress deserve most of the blame. A smaller share (23%, 19% of all enrollees) says Democrats in Congress deserve most of the blame for not extending the credits.

Unsurprisingly, partisans are most likely to say the other party deserves the blame if Congress doesn’t extend the enhanced premium tax credits. However, four in ten Republican enrollees who want to see the tax credits extended say they will either place most of the blame on President Trump (21%) or Republicans in Congress (21%). Even among the most ardent supporters of President Trump, 14% of MAGA supporters say he will deserve most of the blame if the tax credits are not extended, and an additional one in five MAGA supporters (19%) say Republicans will deserve most of the blame.

Marketplace Enrollees Are About Equally Divided Across Political Affiliation

Recent KFF analysis shows that since 2020, ACA Marketplace enrollment has seen a particularly high rate of growth in a number of southern states and enrollment has grown faster in states won by President Trump in 2024 than those won by Kamala Harris. KFF’s 2025 Marketplace Enrollees Survey finds that about four in ten Marketplace enrollees (39%) are Republicans or Republican-leaning independents, including 24% who say they are supporters of the Make America Great Again (MAGA) movement. Just over four in ten Marketplace enrollees (45%) identify as Democrats or Democratic-leaning independents, while 17% do not identify or lean toward either political party.

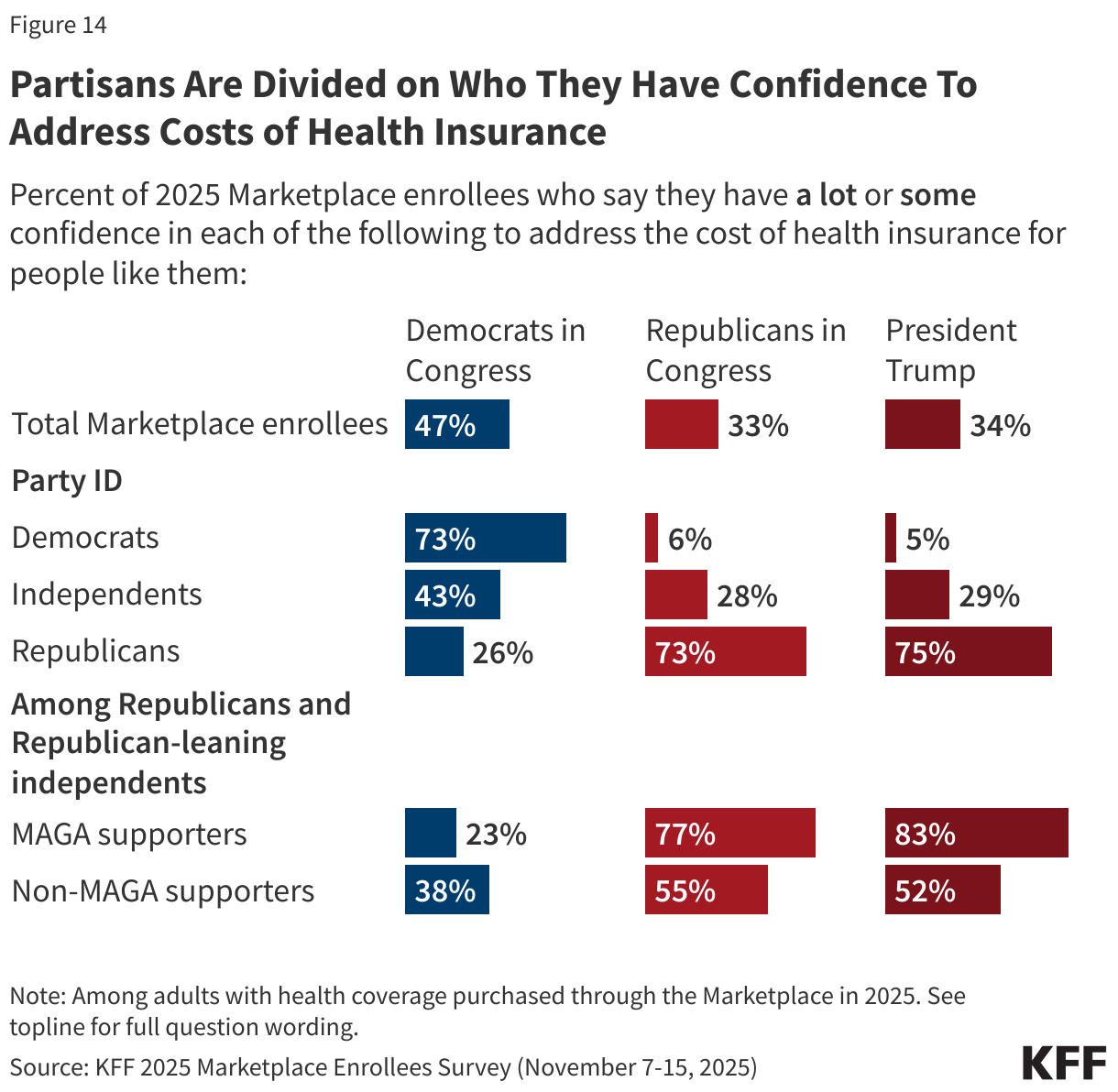

Overall confidence that Congress and President Trump can address the cost of health insurance is low. About two-thirds of Marketplace enrollees say they have “not too much” or no confidence in President Trump (66%) nor in Republicans in Congress (67%) to address health insurance costs for people like them. Congressional Democrats fare only slightly better. Just over half (53%) of enrollees say they have not much or no confidence in Democrats in Congress to address the cost of health insurance for people like them. About half (47%) of Marketplace enrollees express at least some confidence in Congressional Democrats to address insurance costs. About a third say the same about President Trump (34%) and Republicans in Congress (33%).

Unsurprisingly, partisans are more likely to express at least some confidence in lawmakers from their own party. For example, about three in four (73%) Democrats with Marketplace insurance say they have at least some confidence in Democrats in Congress to address the cost of insurance for people like them. On the other hand, about three-quarters of Republicans with Marketplace coverage say they have at least some confidence in Congressional Republicans (73%) and in President Trump (75%) to address the cost of health insurance. Nearly eight in ten (78%) Democrats and nearly half (48%) of independents say they have “no confidence” in President Trump to address the cost of health insurance for people like them.

Large shares of Republicans and Republican-leaning independents with Marketplace coverage who support the MAGA movement express at least some confidence in President Trump (83%) and in Republicans in Congress (77%) to address health insurance costs; yet notably, about one in four MAGA supporters (23%) do say they have “a lot” or “some” confidence in Democrats in Congress to address this issue.

Increases in Health Care Expenses May Impact How Enrollees Approach the 2026 Elections

If current Marketplace enrollees are faced with increased health care expenses next year, there may also be some notable political implications. More than a third of Marketplace enrollees (37%) say President Trump would deserve most of the blame if their personal health care expenses increased by $1,000 next year. A third (33%) say the Republicans in Congress would be most to blame, while about three in ten (29%) place most of the blame on Democrats in Congress.

Democrats with Marketplace insurance say they would largely blame Republicans in Congress (46%) or President Trump (49%) if their health care expenses increase by $1,000 next year. Among independents, more than four in ten (44%) would blame the President, while about a third (32%) would blame Congressional Republicans, and about one in four (23%) would put most of the blame on Democrats in Congress.

Though most Republicans (65%) would blame Congressional Democrats if their health care costs increased by $1,000 next year, about a third say they would blame either Republicans in Congress (20%) or President Trump (14%). Among MAGA supporters, 17% say they would blame Republicans in Congress and a further 9% would blame President Trump if their health care expenses increase by $1,000 next year.

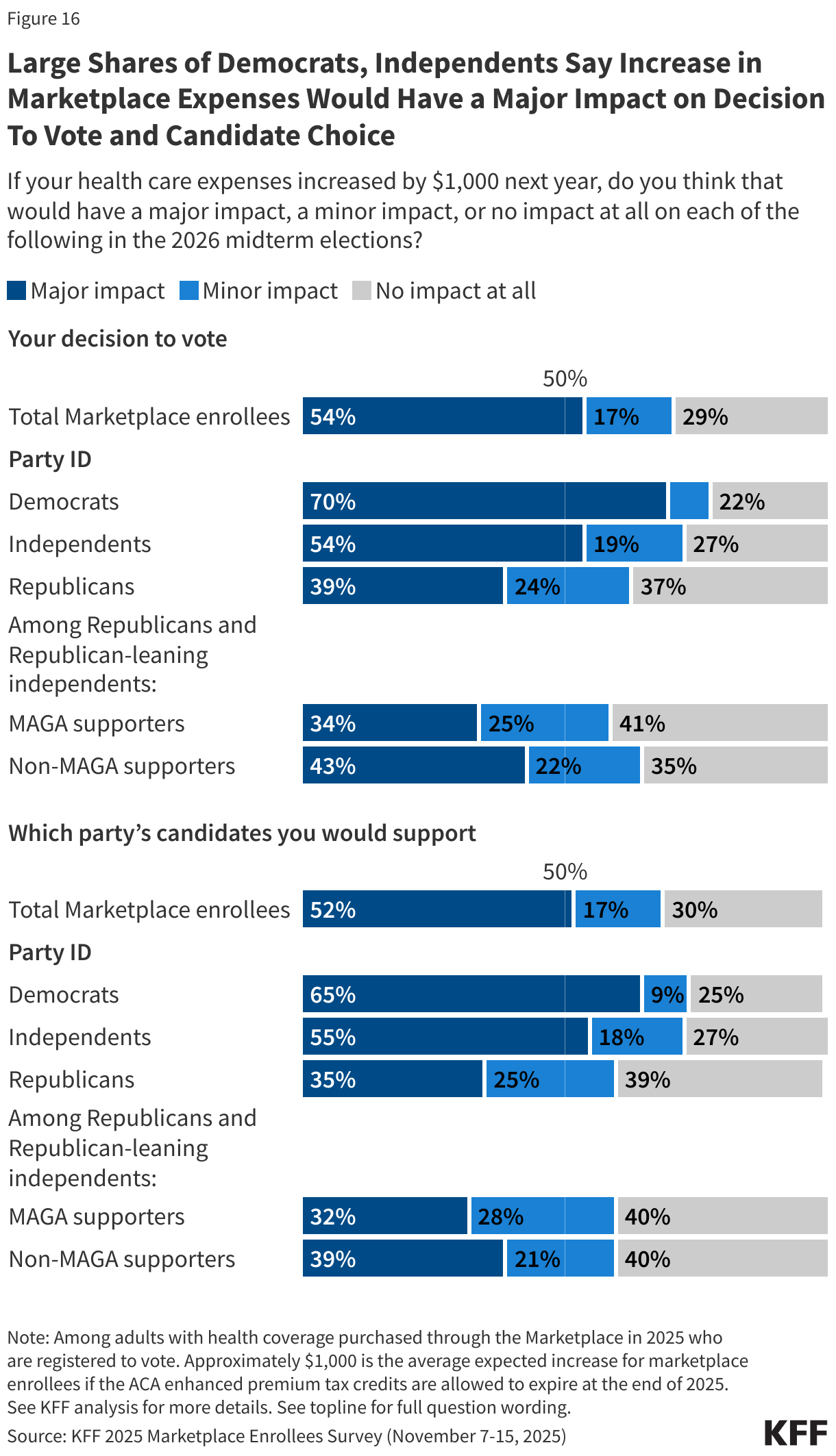

Additionally, for some Marketplace enrollees, an increase in health care expenses may affect how they approach the 2026 midterm elections. If their overall health care expenses, including co-pays, deductibles, and premiums, increased by $1,000 next year, about half of Marketplace enrollees who are registered to vote say it would have a “major impact” on their decision to vote in the 2026 midterm elections (54%) or which party’s candidate they will vote for (52%). About one in five say an increase in their expenses would have a “minor impact” on their decision to vote (17%) or which party they vote for (17%).

Democratic voters with Marketplace coverage are much more likely to say that a $1,000 increase in their health expenses would have a major impact on the 2026 midterm elections, both in terms of turnout and candidate choice, compared with Republican and independent voters with Marketplace coverage. Seven in ten Democrats (70%) and just over half of independents (54%) say an increase in their health care expenses would have a “major impact” on their decision to vote, as do about four in ten (39%) of Republicans. In addition, about two-thirds of Democrats (65%) as well as a slight majority of independents (55%), say an increase of $1,000 in their health care expenses next year would have a “major impact” on which party’s candidate they would support, compared to about a third of Republicans (35%). Four in ten MAGA Republican enrollees who are registered to vote say that if their health care expenses increased by $1,000 next year, it would have “no impact at all” on which party’s candidate they support in the 2026 midterm elections (40%) or whether they vote (41%).

Methodology

This KFF 2025 Marketplace Enrollees Survey was designed and analyzed by public opinion researchers at KFF. The survey was conducted November 7-15, 2025, online and by telephone among a nationally representative sample of 1,350 U.S. adults ages 18-64 who are covered by a plan purchased through the Affordable Care Act Marketplace, in English (n=1,301) and in Spanish (n=49). To qualify for the survey respondents needed to indicate that they were 18-64 years old, covered by health insurance purchased directly from an insurance company, health insurance broker or a state or federal marketplace and not covered by COBRA extension of employer-based health insurance. The sample includes 972 adults (n=24 in Spanish) reached through the SSRS Opinion Panel either online (n=944) or over the phone (n=28). The SSRS Opinion Panel is a nationally representative probability-based panel where panel members are recruited randomly in one of two ways: (a) Through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) provided by Marketing Systems Groups (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS); (b) from a dual-frame random digit dial (RDD) sample provided by MSG. For the online panel component, invitations were sent to panel members by email followed by up to three reminder emails.

An additional 350 adults ages 18-64 who are currently covered by direct-purchase insurance were reached through the IPSOS Knowledge Panel online in English (n=325) and in Spanish (n=25). The IPSOS Knowledge Panel is a nationally representative probability-based panel where panel members are recruited randomly through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS). Another 28 adults ages 18-64 currently covered by direct-purchase insurance that were previously recruited to complete the KFF Health Tracking Polls in 2024-2025 were reached via their prepaid cell phone number. Among this prepaid cell phone component, 11 were interviewed by phone and 17 were invited to the web survey via short message service (SMS).

Respondents in the prepaid cell phone sample who were interviewed by phone received a $15 incentive via a check received by mail. Respondents in the prepaid cell phone sample reached via SMS received a $10 electronic gift card incentive. SSRS Opinion Panel respondents received a $5 electronic gift card incentive (some harder-to-reach groups received a $10 electronic gift card). Ipsos operates an incentive program that includes raffles and sweepstakes with both cash rewards and other prizes to be won. An additional incentive is usually provided for longer surveys. In order to ensure data quality, cases were removed if they failed two or more quality checks: (1) attention check questions in the online version of the questionnaire, (2) had over 30% item non-response, or (3) had a length less than one quarter of the mean length by mode. Based on this criterion, there were no cases removed.

The combined cell phone and panel samples were weighted to match the sample’s demographics to the national U.S. adult population 18-64 who are currently covered by direct-purchase insurance using data from the Census Bureau’s 2025 Current Population Survey (CPS). The demographic variables included in weighting are gender, age, education, census region, number of adults in household, and home tenure. The sample was also weighted to match the proportion of responses by individuals living in a Medicaid expansion state. Additionally, the weights account for differences in the probability of selection for each sample type (prepaid cell phone, IPSOS Knowledge Panel, and SSRS Opinion Panel). This includes adjustment for ownership of a prepaid cellphone and the design of the panel-recruitment procedure (IPSOS Knowledge Panel and SSRS Opinion Panel).

The margin of sampling error including the design effect for the full sample is plus or minus 3.3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available on request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. KFF public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

| Group | N (unweighted) | M.O.S.E. |

|---|---|---|

| Total 2025 Marketplace enrollees | 1,350 | ± 3 percentage points |

| Party ID | ||

| Democrats | 445 | ± 6 percentage points |

| Independents | 460 | ± 6 percentage points |

Republicans | 367 | ± 6 percentage points |

| Age | ||

| 18-29 | 178 | ± 8 percentage points |

| 30-49 | 557 | ± 5 percentage points |

| 50-64 | 615 | ± 5 percentage points |