A Current Snapshot of the Medicare Part D Prescription Drug Benefit

Medicare Part D is a voluntary outpatient prescription drug benefit for people with Medicare provided through private plans that contract with the federal government. Beneficiaries can choose to enroll in either a stand-alone prescription drug plan (PDP) to supplement traditional Medicare or a Medicare Advantage drug plan (MA-PD) that includes drug coverage and all other Medicare-covered benefits. This brief provides an overview of the Medicare Part D program, plan availability, enrollment, and spending and financing, based on KFF analysis of data from the Centers for Medicare & Medicaid Services (CMS) and other sources. It also provides an overview of changes to the Part D benefit based on provisions in the Inflation Reduction Act. (A separate KFF analysis provides more detail about Part D plan availability, premiums, and cost sharing.)

Takeaways

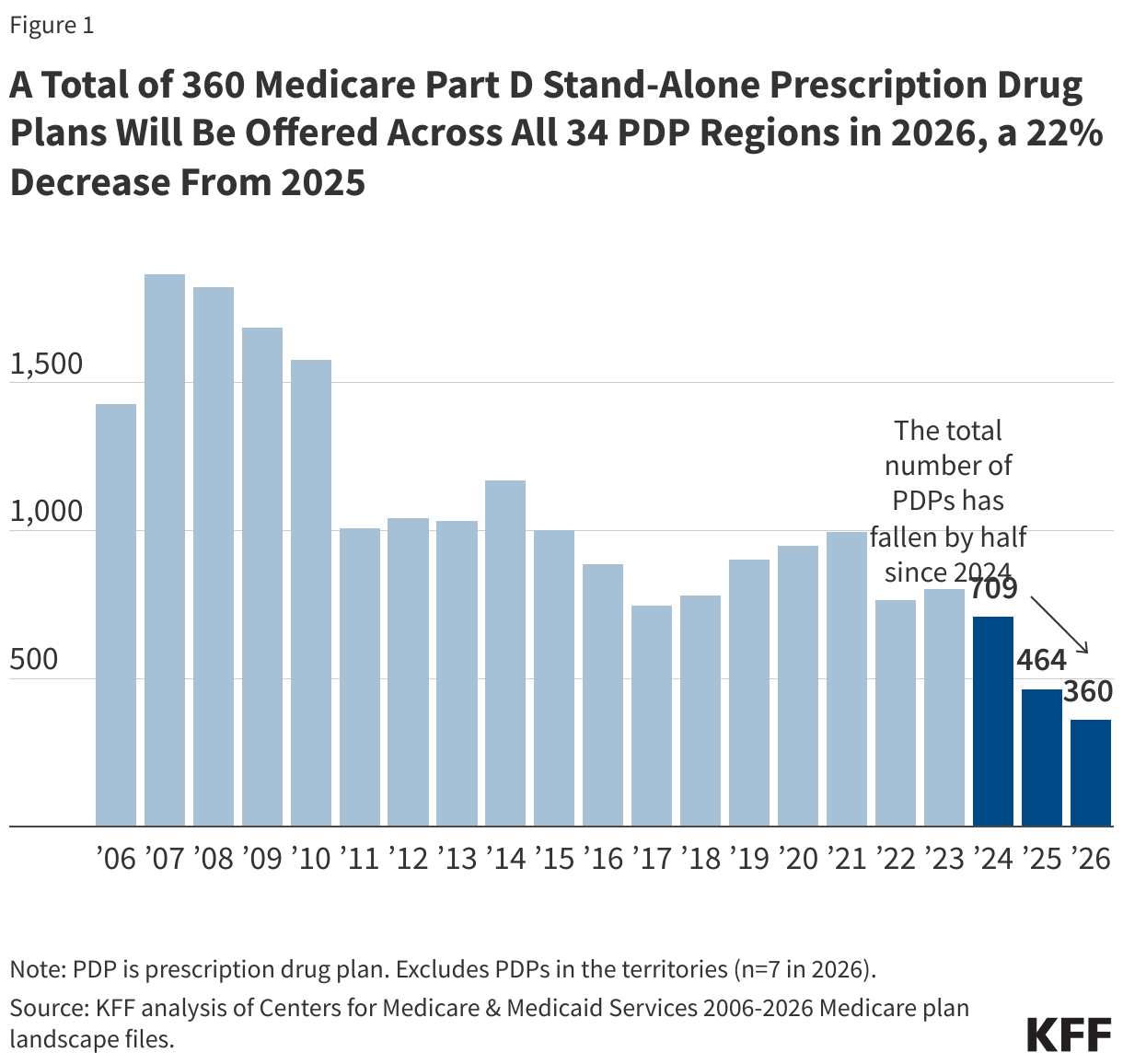

- In 2026, beneficiaries in each state will have a choice of between 8 and 12 Medicare Part D stand-alone prescription drug plans, plus many Medicare Advantage drug plans. A total of 360 PDPs will be offered by 17 different parent organizations across the 34 PDP regions nationwide (excluding 7 PDPs in the territories), a 22% decrease in PDPs from 2025 and 2 fewer parent organizations.

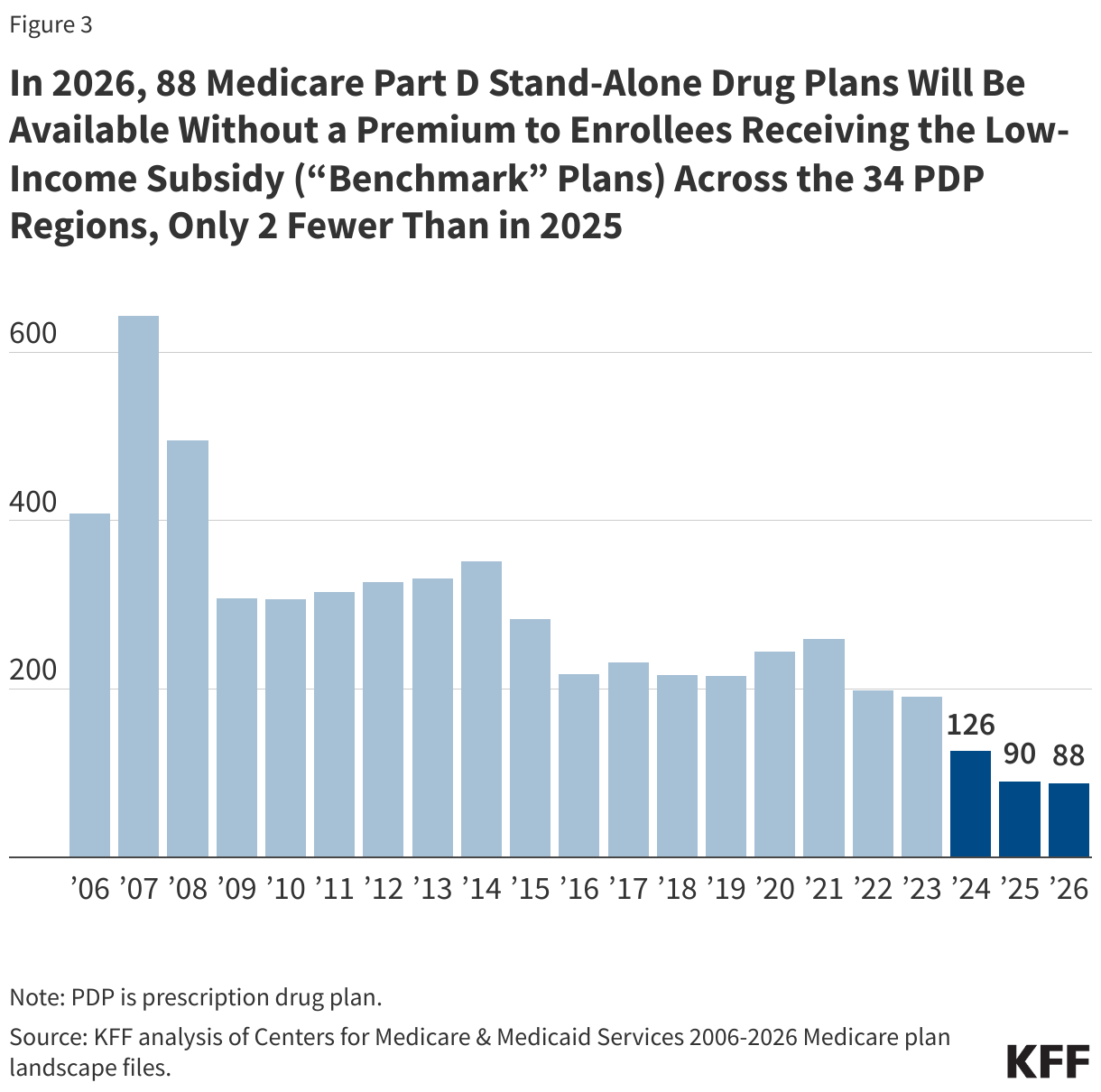

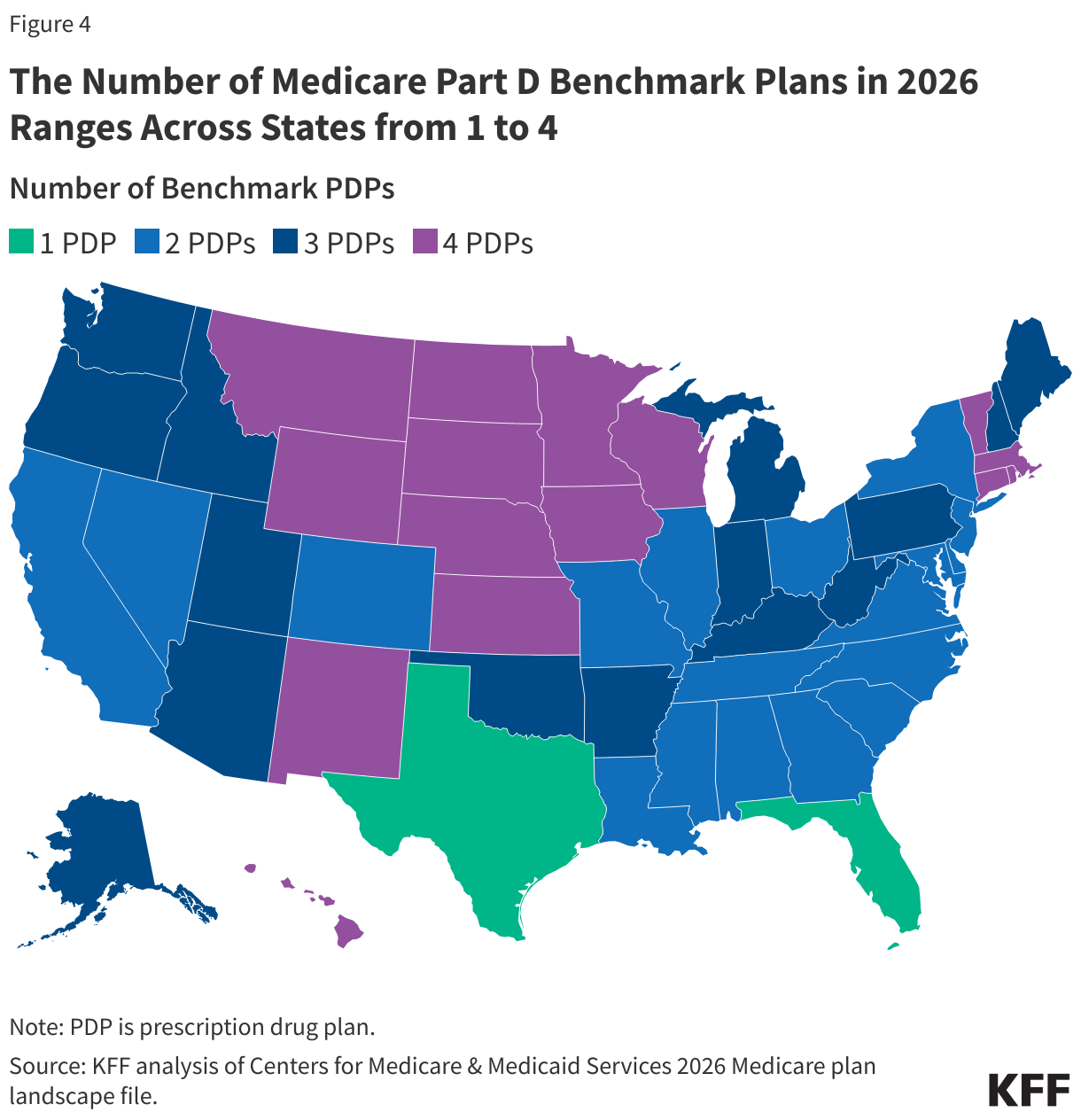

- Roughly the same number of PDPs will be available for enrollment of Part D Low-Income Subsidy (LIS) beneficiaries for no premium (“benchmark” plans) in 2026, varying from 1 to 4 PDPs across states. A total of 88 PDPs will be benchmark plans in 2026, 2 fewer than in 2025.

- Several changes to the Medicare Part D benefit under the Inflation Reduction Act have taken effect, including a cap on out-of-pocket drug spending, which will be set at $2,100 in 2026; an increase in the share of drug costs above the cap paid for by Part D plans and drug manufacturers; and a reduction in Medicare’s share of these costs.

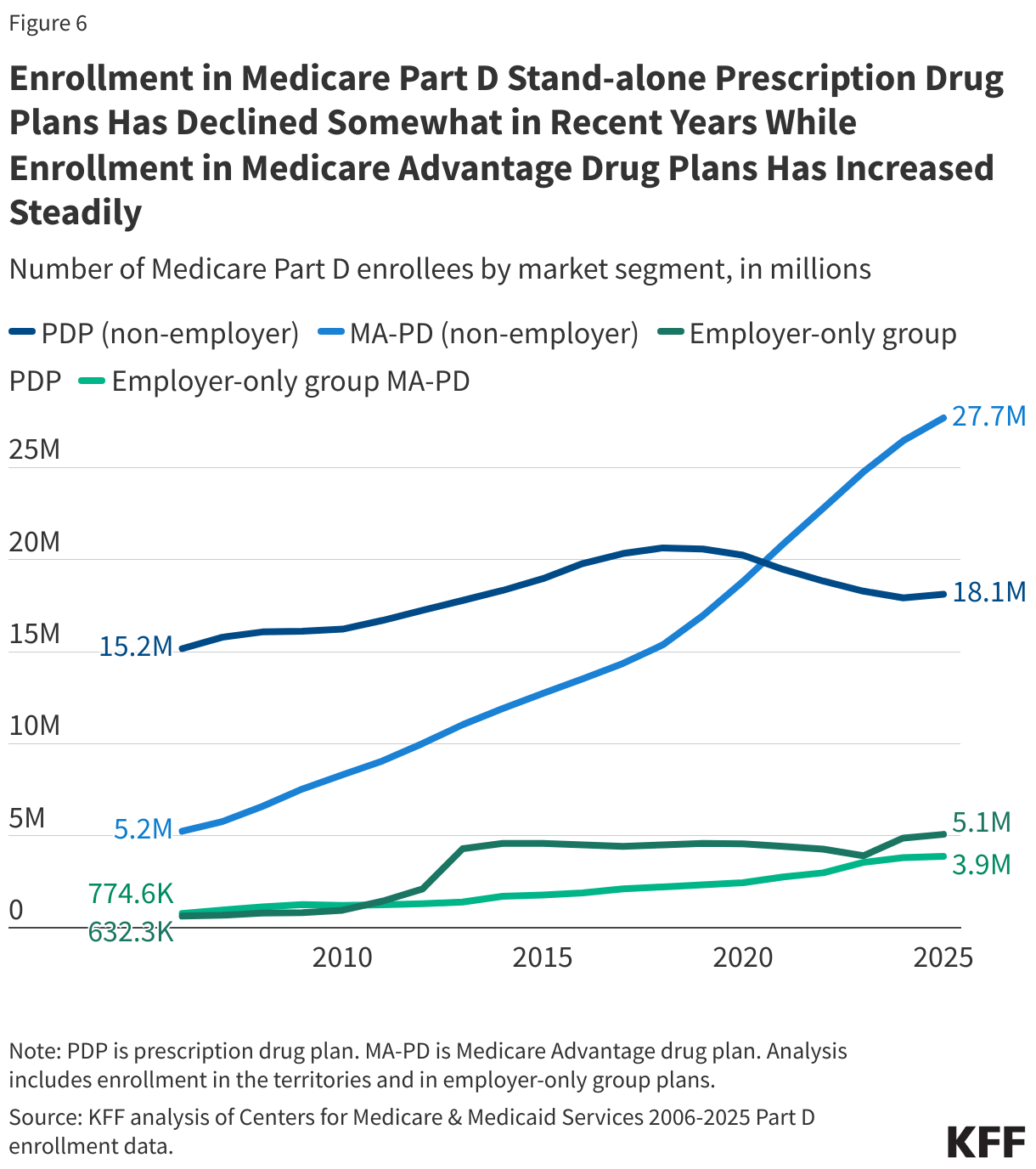

- In 2025, 54.8 million of the 68.8 million Medicare beneficiaries in total are enrolled in Medicare Part D plans, including employer-only group plans; among Part D enrollees, 58% are enrolled in MA-PDs and 42% are enrolled in stand-alone PDPs. As of May 2025, 13.9 million Part D enrollees receive premium and cost-sharing assistance through the LIS program.

- Medicare’s actuaries estimate that spending on Part D benefits (net of premiums paid by enrollees) will total $140 billion in 2026, representing 11% of total spending on all Medicare-covered benefits. Funding for Part D comes from federal government contributions (75%), beneficiary premiums (13%), and state contributions (12%).

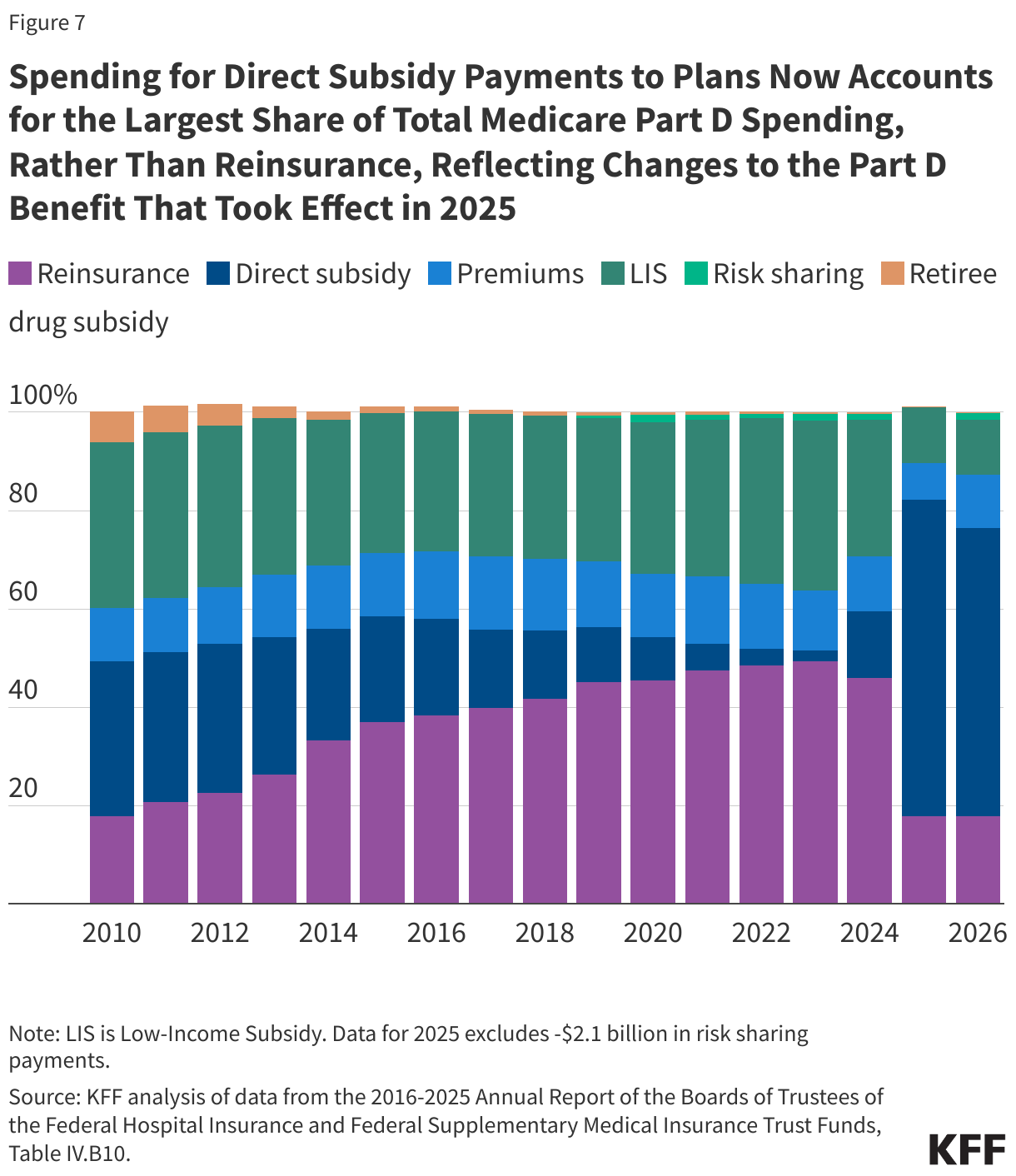

- Medicare’s payments to Part D plans to subsidize the cost of basic Part D benefits per enrollee are projected to account for roughly three-fourths of Medicare’s total reimbursement per enrollee in 2026, while reinsurance payments (to subsidize a portion of drug spending for enrollees with high drug costs) will equal one-fourth. This is a reversal from 2024, when reinsurance accounted for three-fourths of total reimbursement per enrollee. This change reflects the increased generosity of the standard Part D benefit with the addition of an out-of-pocket spending cap in 2025, along with the reduction in Medicare’s liability for catastrophic drug costs from 80% in 2024 to 20% for brands and 40% for generics in 2025. Part D plans and drug manufacturers now bear greater responsibility for catastrophic coverage costs.

Medicare Prescription Drug Plan Availability in 2026

In 2026, a total of 360 PDPs will be offered by 17 different parent organizations across the 34 PDP regions nationwide (excluding the territories), a 22% decrease in PDPs from 2025 (and nearly half as many as in 2024) and 2 fewer parent organizations (Figure 1). While the availability of stand-alone PDPs has been trending downward over time, the availability of Medicare Advantage drug plans has expanded in recent years, and more people in Medicare are now getting Part D drug coverage through Medicare Advantage plans.

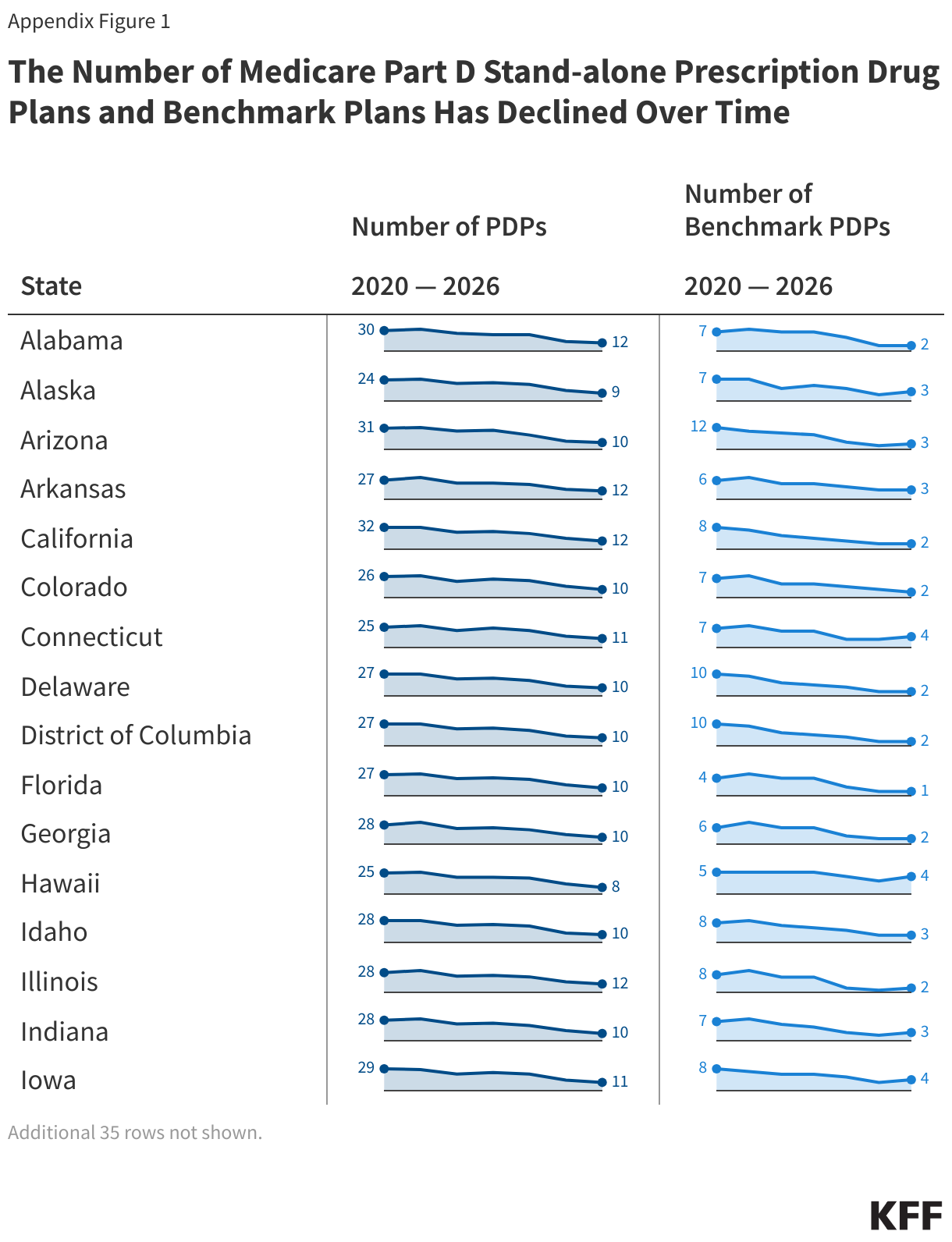

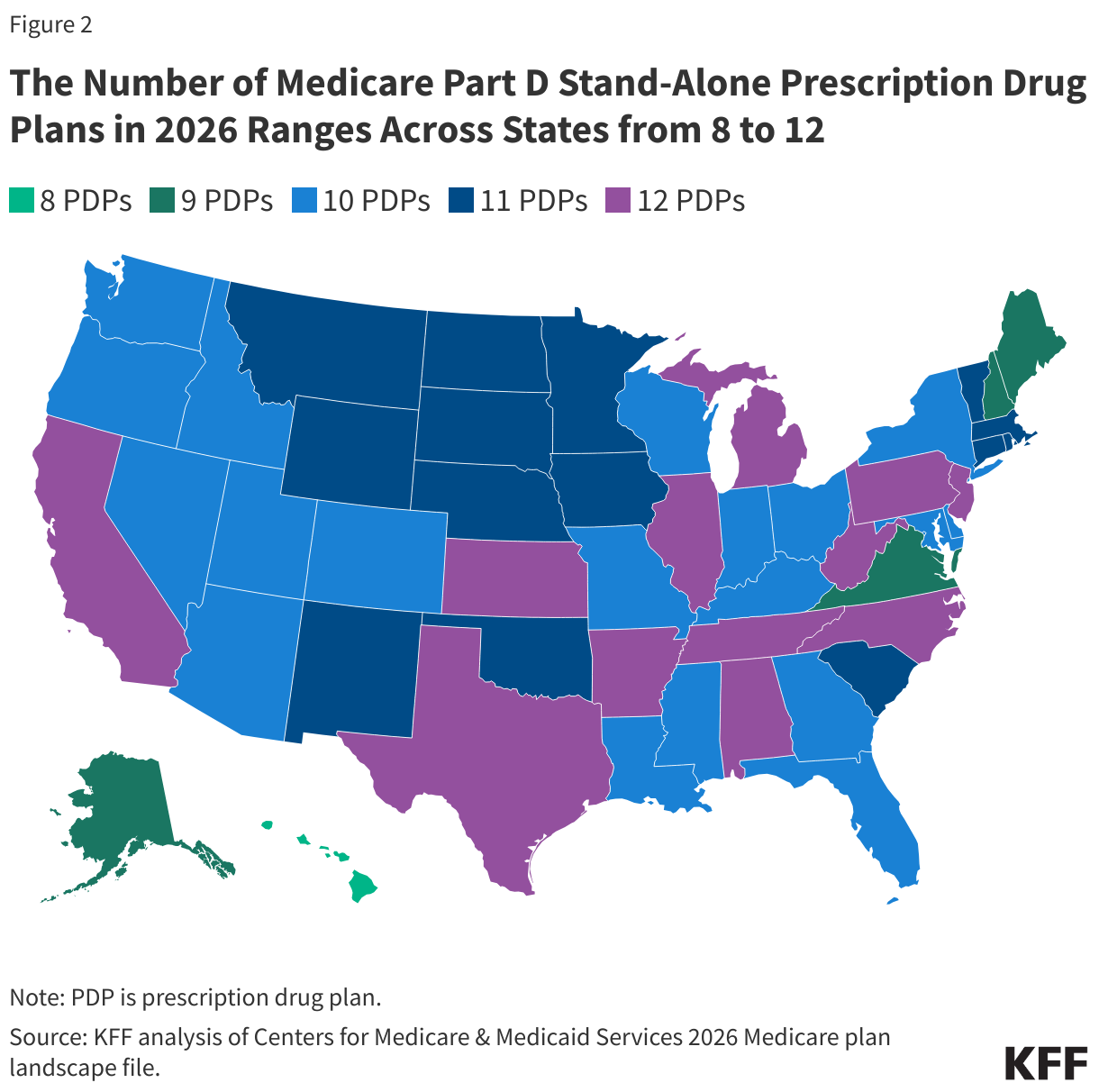

Despite a reduction in the number of PDPs overall, beneficiaries in each state will have a choice of between 8 and 12 stand-alone PDPs offered by between 4 and 6 parent organizations in each state (Figure 2, Appendix Figure 1). In addition, beneficiaries will be able to choose from among many MA-PDs available at the county level.

Low-Income Subsidy Plan Availability in 2026

Beneficiaries with low incomes and modest assets are eligible for assistance (“extra help”) with Part D plan premiums and cost sharing. Through the Part D Low-Income Subsidy (LIS) program, additional premium and cost-sharing assistance is available for Part D enrollees with low incomes (less than 150% of poverty, or $23,475 for individuals/$31,725 for married couples in 2025) and modest assets (up to $17,600 for individuals/$35,1300 for couples in 2025). People who qualify for the LIS program pay modest copayments for prescription drugs, no drug deductible, and no premium for drug coverage in premium-free “benchmark” plans.

In 2026, roughly the same number of plans will be available for enrollment of LIS beneficiaries for no premium (benchmark plans) compared to 2025 – 88 plans (2 fewer than in 2025), but the lowest number of benchmark plans available since Part D started (Figure 3). Overall, one quarter (24%) of PDPs in 2026 are benchmark plans.

At the PDP region level, the number of PDP choices overall remains more robust than the number of premium-free benchmark PDPs. In 2026, the number of premium-free PDPs ranges across states from 1 plan in 2 states (Florida and Texas) to 4 plans in 15 states (Figure 4, Appendix Figure 1). LIS enrollees can select any plan offered in their area, but if they are enrolled in a non-benchmark plan, they may be required to pay some portion of their plan’s monthly premium.

Changes to Part D Under the Inflation Reduction Act

The Inflation Reduction Act of 2022 contained several provisions to lower prescription drug spending by Medicare and beneficiaries, including major changes to the Medicare Part D program, which started to take effect in 2023. These changes were designed to address several concerns, including the lack of a hard cap on out-of-pocket spending for Part D enrollees; the inability of the federal government to negotiate drug prices with manufacturers; a significant increase in Medicare “reinsurance” spending for Part D enrollees with high drug costs; prices for many Part D covered drugs rising faster than the rate of inflation; and the relatively weak financial incentives faced by Part D plan sponsors to control high drug costs. Provisions in the law include:

- Limiting the price of insulin products to no more than $35 per month in all Part D plans and makes adult vaccines covered under Part D available for free, as of 2023.

- Requiring drug manufacturers to pay a rebate to the federal government if prices for drugs covered under Part D and Part B increase faster than the rate of inflation, with the initial period for measuring Part D drug price increases running from October 2022-September 2023.

- Expanding eligibility for full benefits under the Part D Low-Income Subsidy program in 2024.

- Adding a hard cap on out-of-pocket drug spending under Part D by eliminating the 5% coinsurance requirement for catastrophic coverage in 2024 and capping out-of-pocket spending at $2,000 in 2025 (increasing to $2,100 in 2026).

- Shifting more of the responsibility for catastrophic coverage costs to Part D plans and drug manufacturers, starting in 2025.

- Authorizing the Secretary of the Department of Health and Human Services to negotiate the price of some drugs covered under Medicare, with negotiated prices first available for 10 Part D drugs in 2026.

Part D Plan Premiums and Benefits in 2026

Premiums

The 2026 Part D base beneficiary premium – which is based on bids submitted by both PDPs and MA-PDs and is not weighted by enrollment – is $38.99, a 6% increase from 2025. Annual growth in the base beneficiary premium is capped at 6% due to a provision in the Inflation Reduction Act. Because the base premium is an average across both types of plans and reflects the cost of basic benefits only, this amount does not equal what a Part D enrollee will pay for coverage in any given Part D plan.

Because the monthly amount that Part D enrollees pay for individual Part D plans is different from the base beneficiary premium, enrollees may see their premium increase by more or less than 6%, or even decrease, if they stay in the same plan for 2026. A Part D premium stabilization demonstration for PDPs is also helping to moderate premium increases that Part D enrollees might otherwise have faced in 2026, as insurers continue to adjust to higher costs associated with the new out-of-pocket spending cap and increased liability for drug costs above the cap. The Part D premium demonstration was established in 2024 by the Biden administration ahead of the major redesign of the Part D benefit that took effect in 2025. For the first year of the demonstration, the federal government provided participating PDPs with an across-the-board monthly premium subsidy of up to $15 and limited the monthly premium increase for 2025 to $35, along with a narrowing of the risk corridors to mitigate the risk of losses for participating PDPs. For 2026, the Trump administration reduced the monthly premium subsidy from $15 to $10, raised the limit on the PDP monthly premium increase to $50, and eliminated the risk corridor component of the demonstration.

Actual monthly premiums paid by Part D enrollees in stand-alone PDPs in 2026 will vary considerably, ranging from $0 to $100 or more in most regions. In addition to the monthly premium, Part D enrollees with higher incomes ($106,000/individual; $212,000/couple) pay an income-related premium surcharge, ranging from $13.70 to $85.80 per month in 2025 (depending on income).

Most MA-PD enrollees pay no premium beyond the monthly Part B premium (although high-income MA enrollees are required to pay a premium surcharge). MA-PD sponsors can use rebate dollars from Medicare payments to lower or eliminate their Part D premiums, so the average premium for drug coverage in MA-PDs is heavily weighted by zero-premium plans. In 2025, the enrollment-weighted average monthly portion of the premium for drug coverage in MA-PDs is substantially lower than the average monthly PDP premium ($7 versus $39).

Benefits

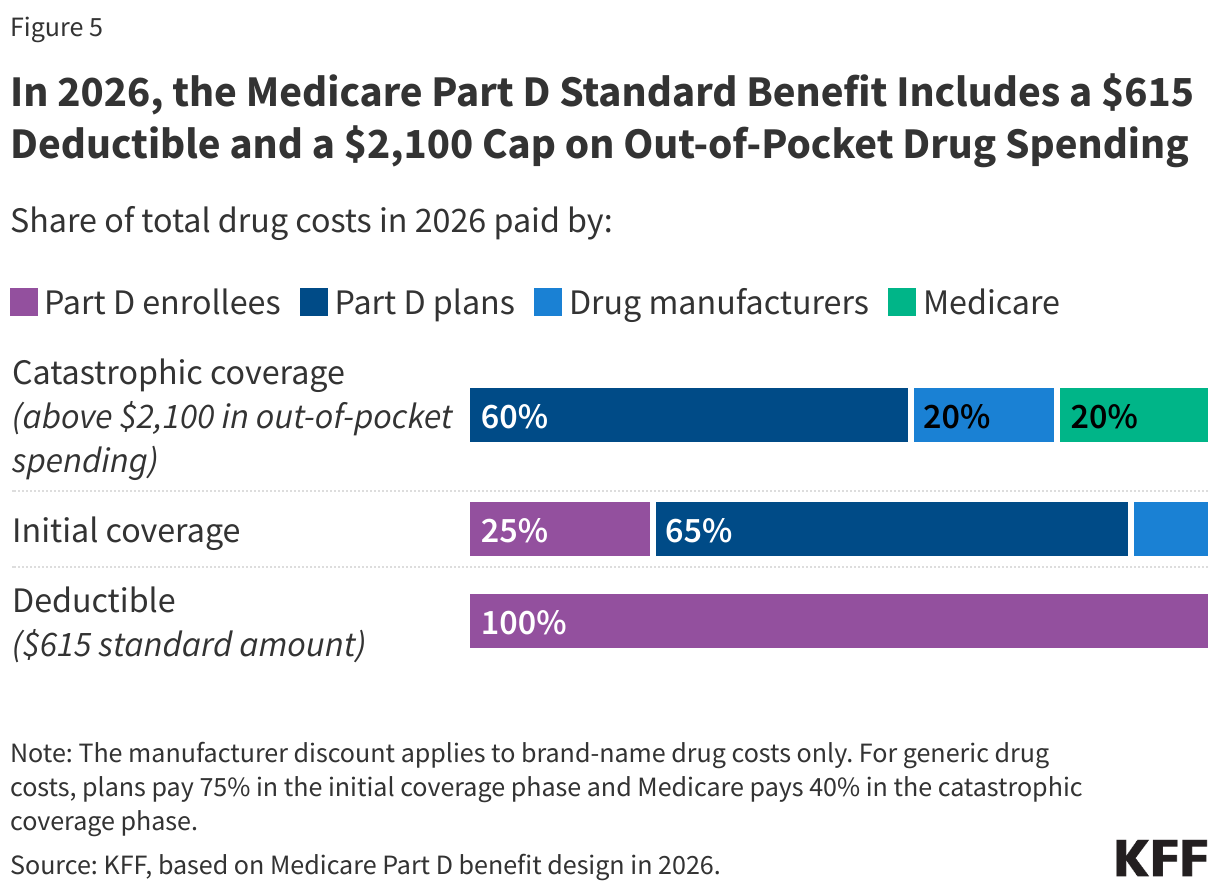

The Part D defined standard benefit changed substantially in 2025 and now includes a cap on out-of-pocket drug spending. The benefit has three phases, including a deductible, an initial coverage phase, and catastrophic coverage. For 2026, under the standard benefit, Part D enrollees will pay a deductible of $615 (up from $590 in 2024), and will then pay 25% of their drug costs in the initial coverage phase until their out-of-pocket spending totals $2,100 (Figure 5). At that point, they qualify for catastrophic coverage and pay no additional out-of-pocket costs.

Part D plans must offer either the defined standard benefit or an alternative equal in value (“actuarially equivalent”) and can also provide enhanced benefits. Both basic and enhanced benefit plans vary in terms of their specific benefit design, coverage, and costs, including deductibles, cost-sharing amounts, utilization management tools (i.e., prior authorization, quantity limits, and step therapy), and which drugs are covered on their formularies. Plan formularies must include drug classes covering all disease states, and a minimum of two chemically distinct drugs in each class. Part D plans are required to cover all drugs in six “protected” classes: immunosuppressants, antidepressants, antipsychotics, anticonvulsants, antiretrovirals, and antineoplastics.

Part D plans are also required to cover all drugs that have been selected for Medicare drug price negotiation, including all dosage forms and strengths. CMS will use the annual formulary review process to ensure that all Part D plans cover all dosages and formulations of selected drugs. Negotiated prices for the first 10 drugs that were selected for negotiation will take effect for Medicare beneficiaries on January 1, 2026.

Part D and Low-Income Subsidy Enrollment in PDPs and MA-PDs

Enrollment in Medicare Part D plans is voluntary, except for beneficiaries who are eligible for both Medicare and Medicaid and certain other low-income beneficiaries who are automatically enrolled in a PDP if they do not choose a plan on their own. Beneficiaries face a penalty equal to 1% of the national average premium for each month they delay enrollment unless they have drug coverage from another source that is at least as good as standard Part D coverage (“creditable coverage”).

In 2025, 54.8 million Medicare beneficiaries are enrolled in Medicare Part D plans, including employer-only group plans; of the total, 58% are enrolled in MA-PDs and 42% are enrolled in stand-alone PDPs (Figure 6). Another 0.7 million beneficiaries are estimated to have drug coverage through employer-sponsored retiree plans where the employer receives a subsidy from the federal government equal to 28% of drug expenses between $615 and $12,650 per retiree in 2026. Several million beneficiaries are estimated to have other sources of drug coverage, including employer plans for active workers, FEHBP, TRICARE, and Veterans Affairs (VA). Around 11% of people with Medicare are estimated to lack creditable drug coverage.

Recent years have seen a growing divide in the Part D plan market between stand-alone PDPs, where the number of plans has generally been trending downward over time in conjunction with a reduction in PDP enrollment, and MA-PDs, where plan availability and enrollment have grown steadily in recent years. The widespread availability of low or zero-premium MA-PDs, while PDPs charge substantially higher premiums on average, could tilt enrollment even more towards Medicare Advantage plans in the future.

As of May 2025, 13.9 million Part D enrollees receive premium and cost-sharing assistance through the LIS program. As with overall Part D enrollment, more LIS enrollees are in MA-PDs than PDPs. Beneficiaries who are dual-eligible individuals, those enrolled in Medicare Savings Programs (QMBs, SLMBs, QIs), and those who receive Supplemental Security Income payments from Social Security automatically qualify for the additional assistance, and they are automatically enrolled in PDPs with premiums at or below the regional Low-Income Subsidy benchmark premium amount if they do not choose a plan on their own. Other beneficiaries can apply for the Low-Income Subsidy through either the Social Security Administration or Medicaid and are subject to both an income and asset test.

Part D Spending and Financing

Part D Spending

Medicare’s actuaries estimate that spending on Part D benefits (net of premiums paid by enrollees) will total $141 billion in 2026, representing 11% of total Medicare benefits spending.

In general, Part D spending depends on several factors, including the total number of Part D enrollees, their health status and the quantity and type of drugs used, the number of high-cost enrollees (those with drug spending above the catastrophic threshold), the number of enrollees receiving the Low-Income Subsidy, the price of drugs covered by Part D and the ability of plan sponsors to negotiate discounts (rebates) with drug companies and preferred pricing arrangements with pharmacies, and to manage use (e.g., promoting use of generic drugs, prior authorization, step therapy, quantity limits, and mail order). Part D spending is also affected by the level of price discounts that the federal government negotiates under the Medicare Drug Price Negotiation Program, as well as the effect of the inflation rebate provision of the IRA on price growth for existing drugs and launch prices for new drugs.

Part D Financing

Financing for Part D comes from federal government contributions (75%), beneficiary premiums (13%), and state contributions (12%). Medicare subsidizes 74.5% of basic Part D benefit costs through a monthly capitated payment to Part D plans for each enrollee, based on an average of bids submitted by plans for their expected basic benefit costs, though this share may be higher with the Inflation Reduction Act’s 6% base beneficiary premium cap and the temporary Part D premium stabilization program in effect. Enrollee premiums for basic benefits were initially set to cover 25.5% of the cost of standard (basic) drug coverage, but with premium stabilization measures in effect, enrollees are paying a lower share of costs overall. Higher-income Part D enrollees pay a larger share of standard Part D costs, ranging from 35% to 85%, depending on income.

Payments to Plans

For 2026, Medicare’s actuaries estimate that Part D plans will receive direct subsidy payments from the federal government for the cost of basic Part D benefits (plus administrative expenses and profits) that average $1,710 per enrollee overall, $522 in reinsurance payments for very high-cost enrollees, and $1,337 in subsidy payments for enrollees receiving the LIS. Employers are expected to receive, on average, $561 in federal subsidies for retirees in employer-subsidy Part D plans. Part D plans also receive additional risk-adjusted payments based on the health status of their enrollees, and plans’ potential total losses or gains are limited by risk-sharing arrangements with the federal government (“risk corridors”).

As of 2025, Medicare’s reinsurance payments to plans for total spending incurred by Part D enrollees above the catastrophic coverage threshold subsidize 20% of brand-name drug spending and 40% of generic drug spending, down from 80% in previous years, due to a provision in the Inflation Reduction Act. With this change in effect, Medicare's aggregate reinsurance payments to Part D plans are projected to account for 18% of total Part D spending in 2026, based on KFF analysis of data from the 2025 Medicare Trustees report. This is a substantial reduction from 2024, when reinsurance spending had grown to account for close to half of total Part D spending (46%) (Figure 7). Currently, the largest portion of total Part D spending is accounted for by direct subsidy payments to plans (59% of total spending in 2026).

Appendix