Analyzing Changes in Medicare Part D Enrollment for 2026

Enrollment in Part D Stand-Alone Prescription Drug Plans Increased, Mainly Due to Growth in Employer Group Plans

For people with Medicare, the Medicare Part D outpatient prescription drug benefit is provided by private plans, either Medicare Advantage plans that offer Part D drug coverage (MA-PDs) or, for those in traditional Medicare, stand-alone prescription drug plans (PDPs). While most beneficiaries are enrolled in Medicare private plans on an individual basis, some have coverage through a group plan sponsored by an employer or union providing retiree health benefits, either group MA plans that cover Medicare Part A and B benefits, which can also include Part D coverage, or group PDPs that cover prescription drugs only.

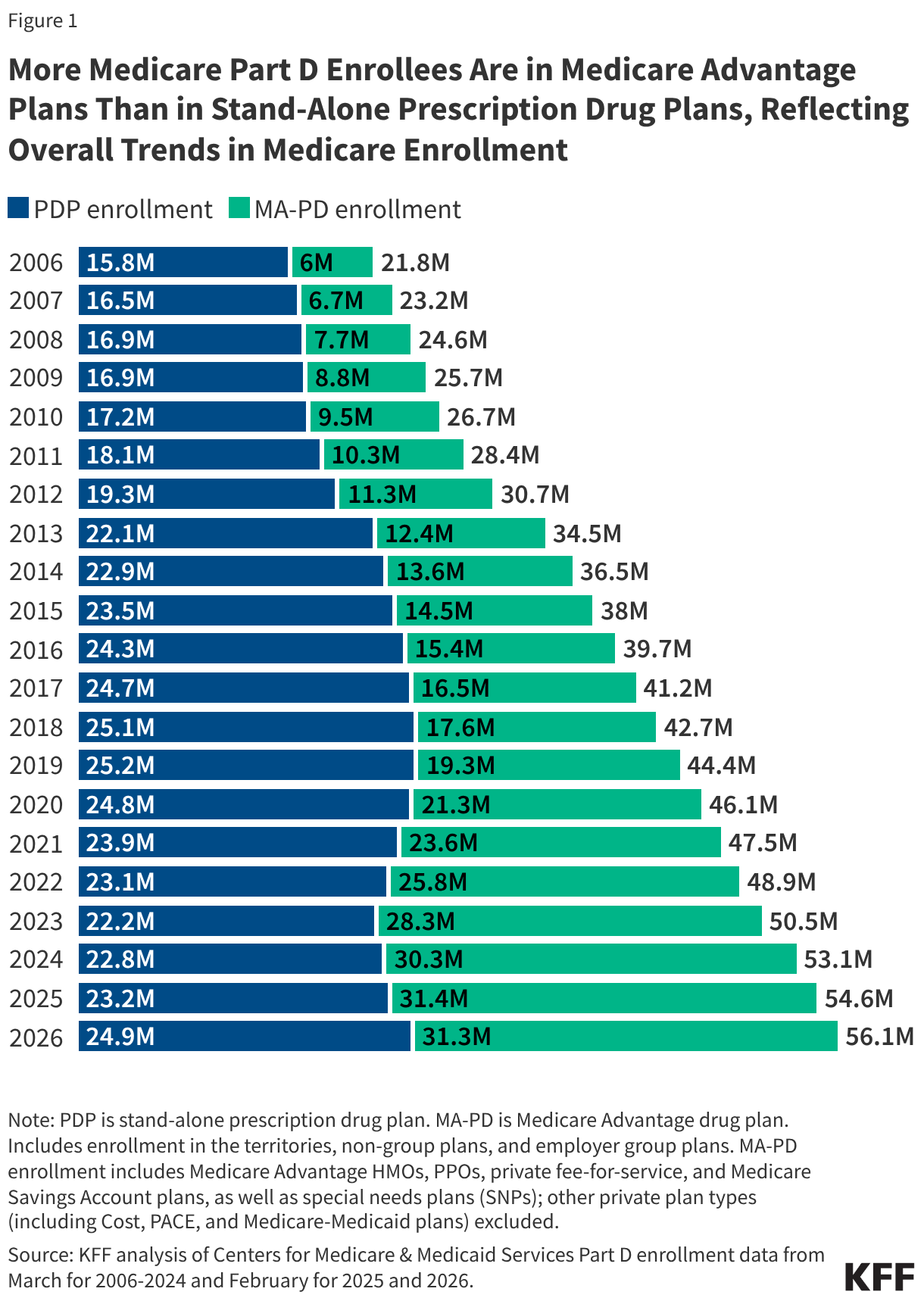

Analysis of recently released data from the Centers for Medicare & Medicaid Services (CMS) shows that 56.1 million people are enrolled in Medicare Part D as of February 2026, including both non-group and group plan enrollment, with more than half of Part D enrollees (56%) in MA-PDs and 44% in stand-alone PDPs, reflecting higher overall enrollment in Medicare Advantage than in traditional Medicare (Figure 1).

Between February 2025 and February 2026, enrollment growth in non-group MA-PDs (including both individual plans and special needs plans, or SNPs) exceeded growth in non-group PDP enrollment, which has flattened out but still increased modestly for 2026 (1 million and 0.5 million, respectively). Reflecting the availability of lower-premium PDPs and likely also shifts in enrollment from higher-premium to lower-premium PDPs, the average monthly enrollment-weighted premium for non-group PDPs fell from $39 to $36 between February 2025 and February 2026 (premiums for employer group plans are not available).

Over the same period, enrollment in group MA-PDs declined for the first time since 2010 and enrollment in group PDPs increased by the largest amount since 2013 (-1.2 million and 1.2 million, respectively). Overall, PDP enrollment increased by 1.7 million between 2025 and 2026, mainly due to the increase in employer group PDP enrollment.

A Total of 56 Million Medicare Beneficiaries Are Enrolled in Part D, Including Both MA-PDs and PDPs, as of Early 2026

As of February 2026, 56.1 million Medicare beneficiaries are enrolled in Part D plans, with more than half (56% or 31.3 million) enrolled in MA-PDs. Enrollment in MA-PDs has generally increased steadily over time, although there was a modest reduction in overall MA-PD enrollment between February 2025 and February 2026 (from 31.4 million to 31.3 million) (Figure 1). This appears to reflect a shift in enrollment among employer group plan enrollees from group MA-PD plans to group MA-only plans with separate PDPs (as discussed below; for more details on Medicare Advantage enrollment in 2026, see KFF analysis “Medicare Advantage Enrollment Grew by About 1 Million People, Mainly Due to Special Needs Plans”).

PDP enrollment now stands at 24.9 million, including beneficiaries in both non-group PDPs and employer group PDPs, or 44% of all Part D enrollees (up slightly from 42% in 2025) (Figure 1). The overall number of PDP enrollees increased for the third year in a row and is up by 1.7 million between February 2025 and February 2026, with most of the growth (1.2 million or 70%) in employer group PDPs.

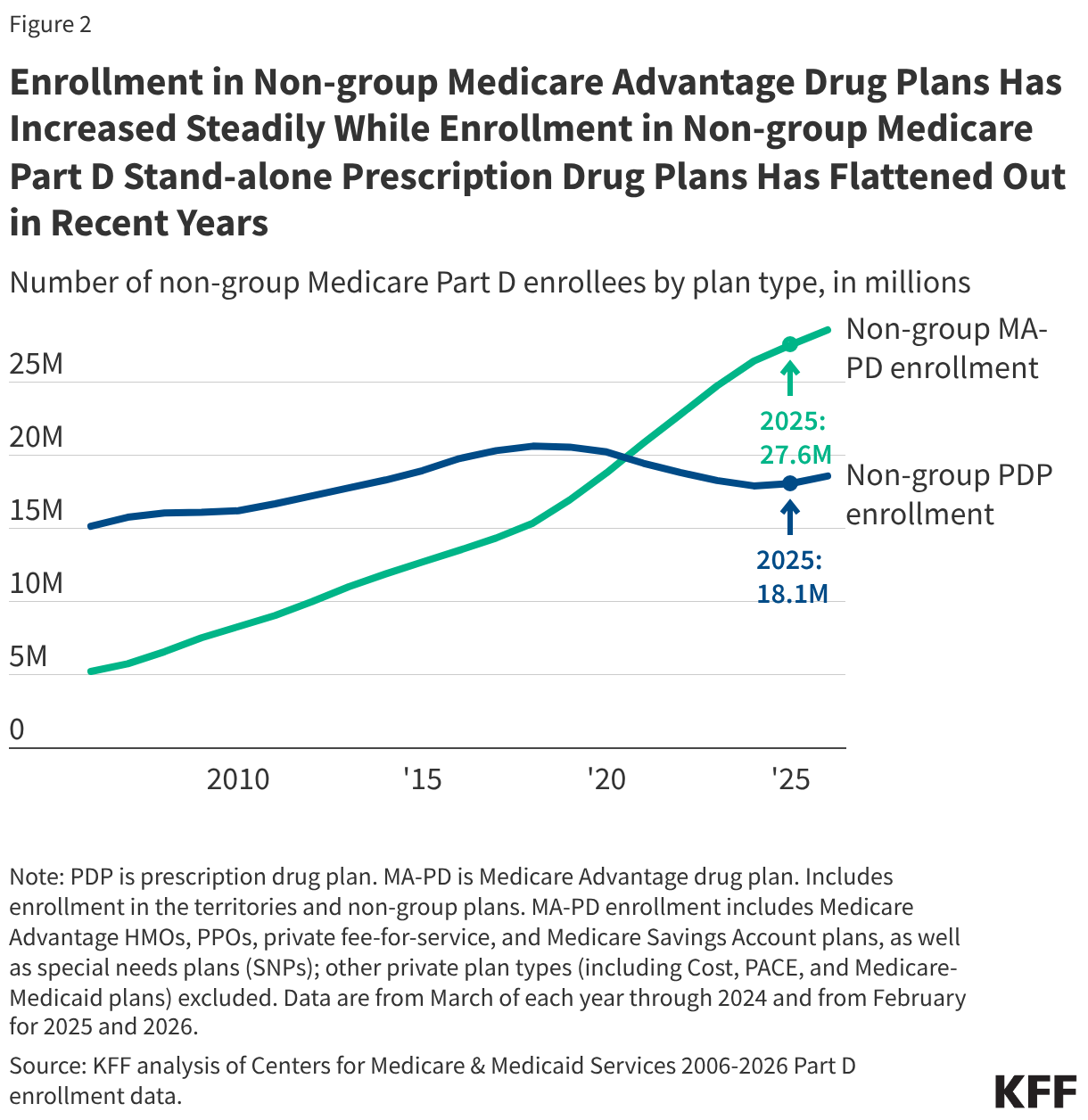

Growth in Non-Group MA-PDs Continues To Outpace Growth in Non-Group PDPs

Among non-group Part D plans, enrollment in non-group MA-PDs stands at 28.6 million as of February 2026, up 1.0 million from 2025, while enrollment in non-group PDPs now stands at 18.6 million, up by 0.5 million from 2025 (Figure 2). Enrollment in non-group PDPs is lower than its peak of 20.6 million in the late 2010s but modestly higher than in 2024, when 17.9 million enrollees were in non-group PDPs. Modest growth in non-group PDP enrollment for 2026 occurred even as the overall number of PDPs fell for the third year in a row and the number of non-group PDP options for the average Medicare beneficiary dropped from 14 in 2025 to 11 in 2026. (By comparison, the average Medicare beneficiary has 32 non-group MA-PD options in 2026, excluding SNPs.)

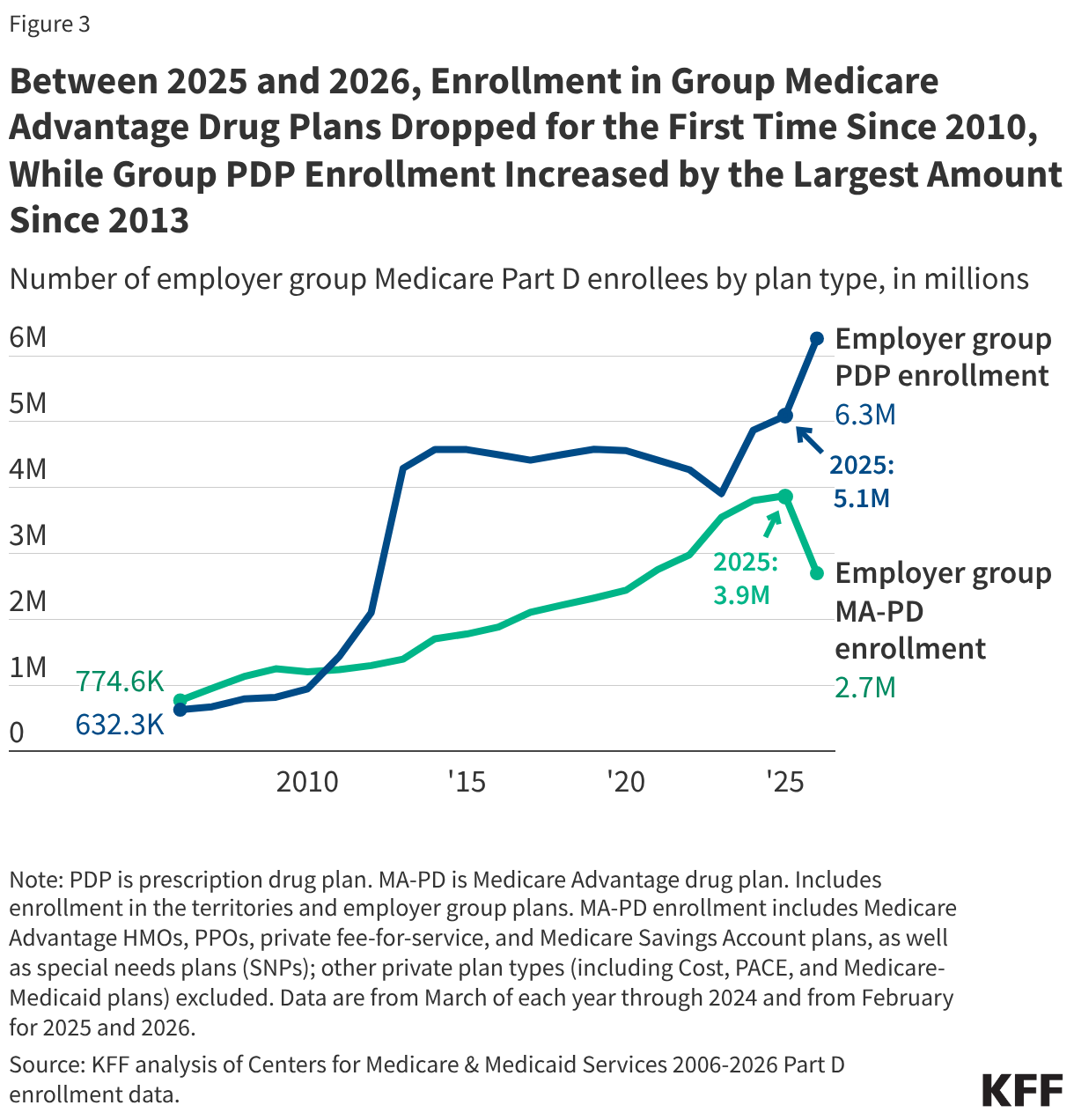

Among Employer Group Plans, Enrollment Decreased in Group MA-PDs and Increased in Group PDPs

Among employer group Part D plans, enrollment in group MA-PDs decreased by 1.2 million between 2025 and 2026 (down from 3.9 million to 2.7 million), while group PDP enrollment increased by 1.2 million (from 5.1 million to 6.3 million) (Figure 3). This was the first year-over-year reduction in employer group MA-PD enrollment since 2010, and the largest year-over-year increase in employer group PDP enrollment since 2013. That year, employer group PDP enrollment increased by 2.2 million (from 2.1 million to 4.3 million) as a result of the ACA’s elimination of the tax deductibility of federal subsidies for retiree drug coverage and the availability of manufacturer price discounts during the coverage gap in employer group plans, which changed the financial incentives around traditional retiree drug coverage and prompted a shift to employer group PDP coverage.

The decline in employer group MA-PD enrollment and concurrent growth in employer group PDP enrollment for 2026 may reflect a strategy among employer/union groups of converting retiree health benefit offerings from contracts with MA-PDs that combine both medical and prescription drug benefits to contracting separately for medical benefits from MA-only plans and prescription drug benefits from stand-alone PDPs. This strategy would enable groups to take advantage of the Part D premium stabilization demonstration and receive additional premium subsidies provided by the federal government, which are available only to PDPs that choose to participate, not MA-PDs. For employer group PDPs, participation in the demonstration in 2026 provides a $10 per member per month premium subsidy.

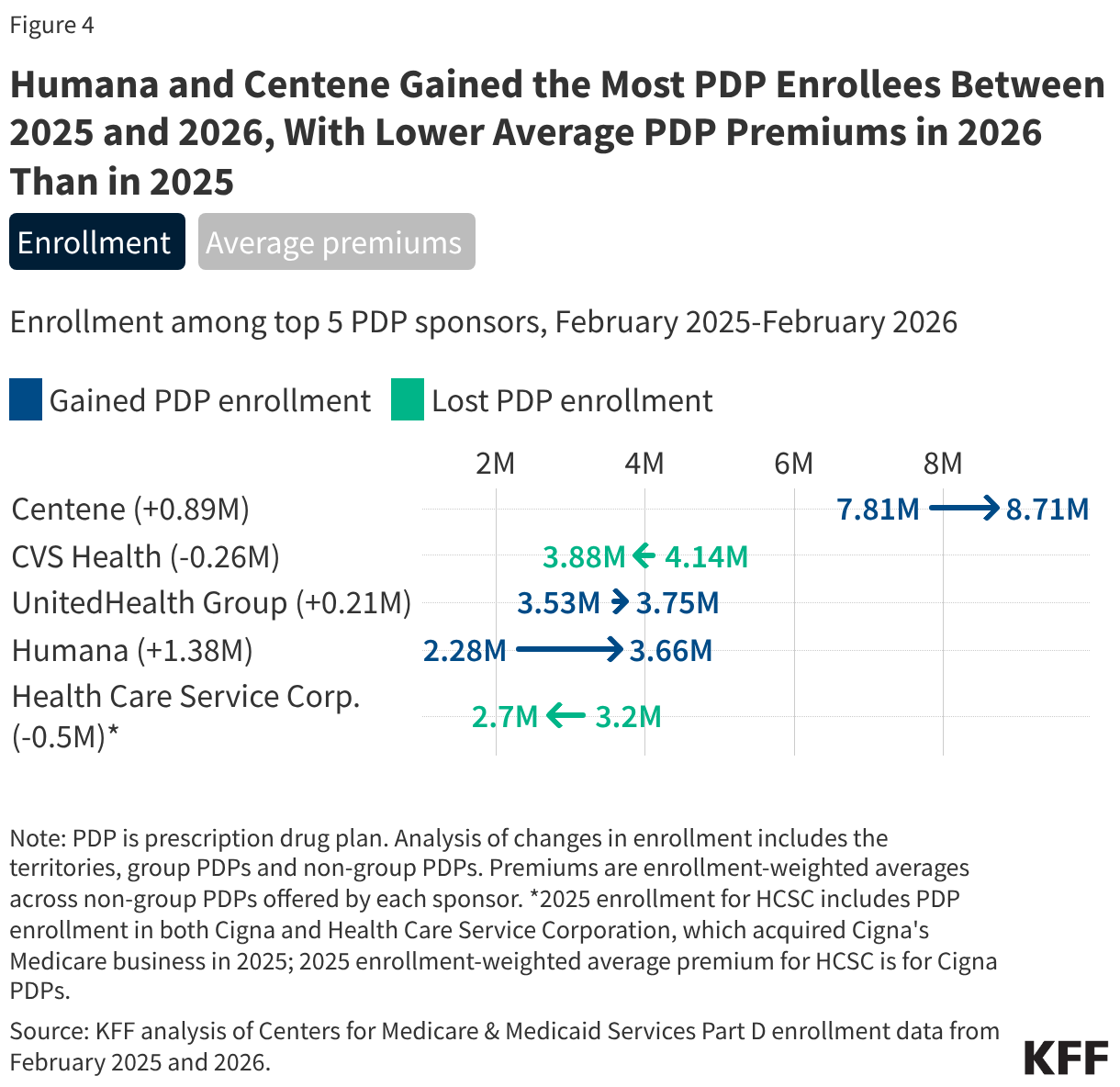

Humana and Centene Saw the Largest Increases in PDP Enrollment in 2026

Part D enrollees faced wide PDP premium changes and variation across plans for 2026, as in previous years, triggering shifts in PDP enrollment. Several national PDPs are charging premiums well below $10 in many regions in 2026, giving current beneficiaries, as well as people new to Medicare, options for relatively low-cost drug coverage if they want to remain in (or choose to enroll in) traditional Medicare. This is the case even as some PDPs charged premium increases of up to $50 for 2026, the maximum increase allowed for plans participating in the Part D premium stabilization demonstration. Reflecting the availability of lower-premium PDPs and likely also shifts in enrollment from higher-premium to lower-premium plans, the average monthly enrollment-weighted premium for non-group PDPs fell from $39 to $36 between February 2025 and February 2026 (premiums for employer group plans are not available).

Humana and Centene (sponsor of WellCare PDPs) gained the most PDP enrollees between February 2025 and February 2026, likely due to reducing monthly premiums for some or all of their PDPs in many regions between 2025 and 2026 and offering low or zero premium PDP options in several regions. Enrollment in Humana’s PDPs increased by 61% (1.4 million) from 2.3 million to 3.7 million, while Centene’s PDP enrollment increased by 11% (0.9 million) from 7.8 million to 8.7 million (Figure 4, “Enrollment” tab). (Humana also gained the most Medicare Advantage enrollees overall for 2026 among all Medicare Advantage plan sponsors.) Both Humana and Centene have lower average enrollment-weighted premiums across their non-group PDP offerings in 2026 than in 2025 (Figure 4, “Average premiums” tab).

Other plan sponsors experienced smaller changes in enrollment over this period. CVS Health and Health Care Service Corporation, which lost PDP enrollees between 2025 and 2026, and UnitedHealth Group, which had a modest increase in PDP enrollment, have higher enrollment-weighted average premiums across their non-group PDP offerings in 2026 than in 2025.