Kaiser Health Tracking Poll – October 2017: Experiences of the Non-Group Marketplace Enrollees

Findings

KEY FINDINGS:

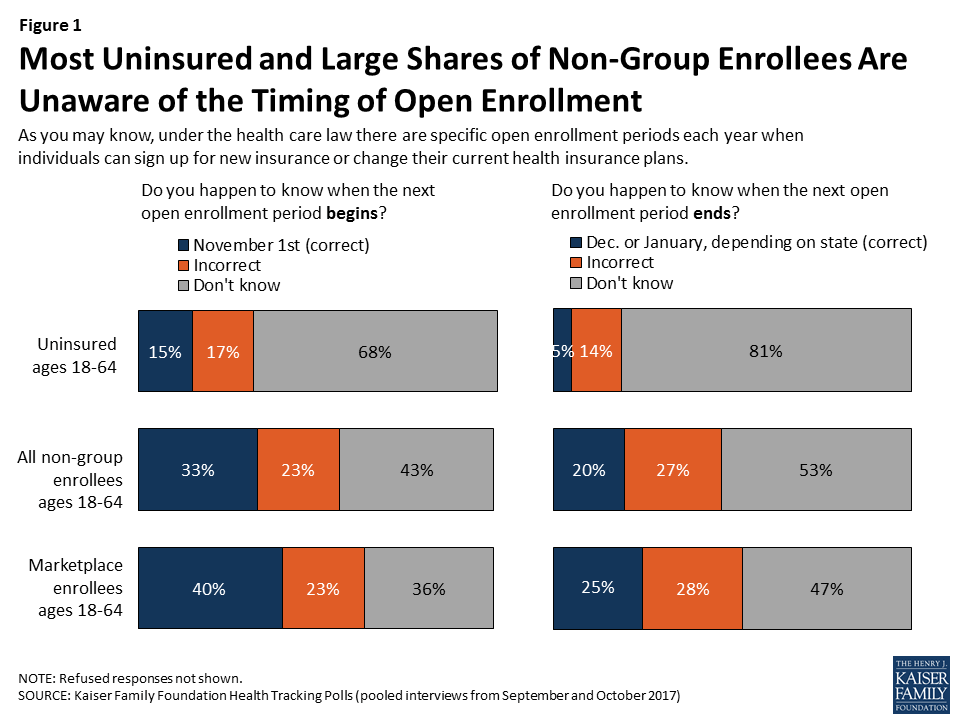

- The start of the open enrollment period for non-group insurance in 2018 is less than one month away, and the majority of individuals who are targets for enrollment – those who currently purchase their own insurance and those who are uninsured – are unaware of the key dates of the next open enrollment period. One-third of non-group enrollees overall and 15 percent of the uninsured are aware of when the next open enrollment period begins. A slightly larger share (40 percent) of marketplace enrollees are aware of the November 1st start date for open enrollment, but still six in ten either give an incorrect answer or say they don’t know when open enrollment begins.

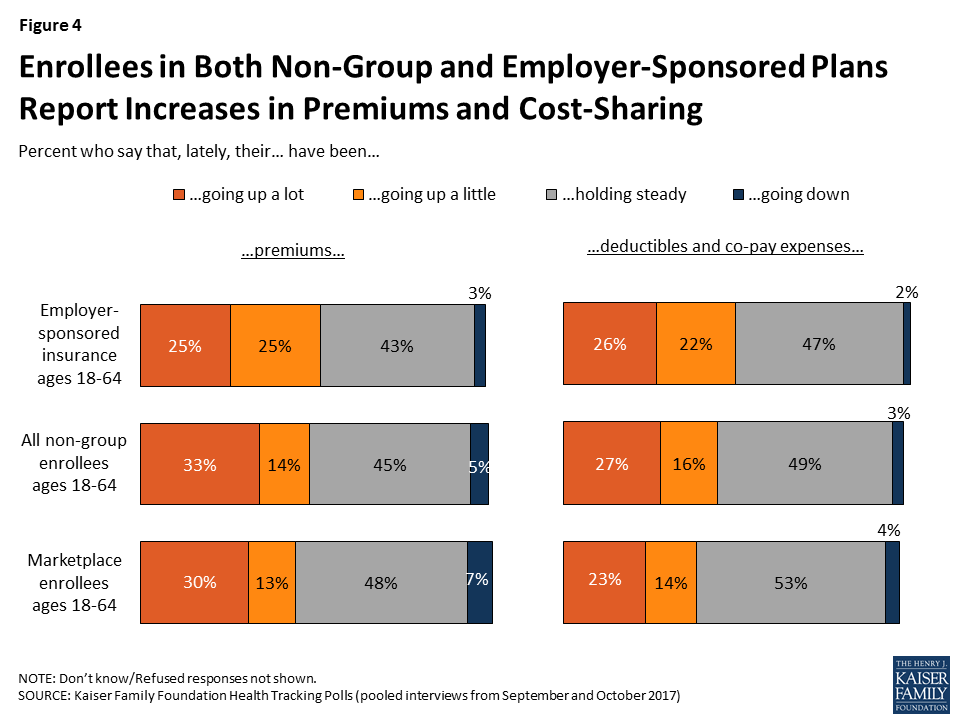

- Overall, the experiences of marketplace enrollees are more similar than different than those with employer coverage when it comes to costs and choices. While nearly half of non-group enrollees (48 percent) and marketplace enrollees (43 percent) say that it seems like their premiums have being going up lately, they are no more likely to say that than those with employer-sponsored insurance (51 percent). When asked about their deductibles and co-pay expenses, about half (49 percent) of those with employer-sponsored insurance say their cost-sharing has gone up lately, as do 43 percent of all non-group enrollees and 37 percent of marketplace enrollees. Yet, marketplace enrollees are more likely to express worry about their future ability to afford insurance and health care services. Six in ten marketplace enrollees say they are worried that their cost sharing will become so high they won’t be able to afford their health care coverage and about half of marketplace enrollees (55 percent) say they are worried their premiums will increase so much that they won’t be able to afford the plan they have now. Worries about increasing cost-sharing and premiums are lower among those with employer coverage (39 percent and 35 percent, respectively).

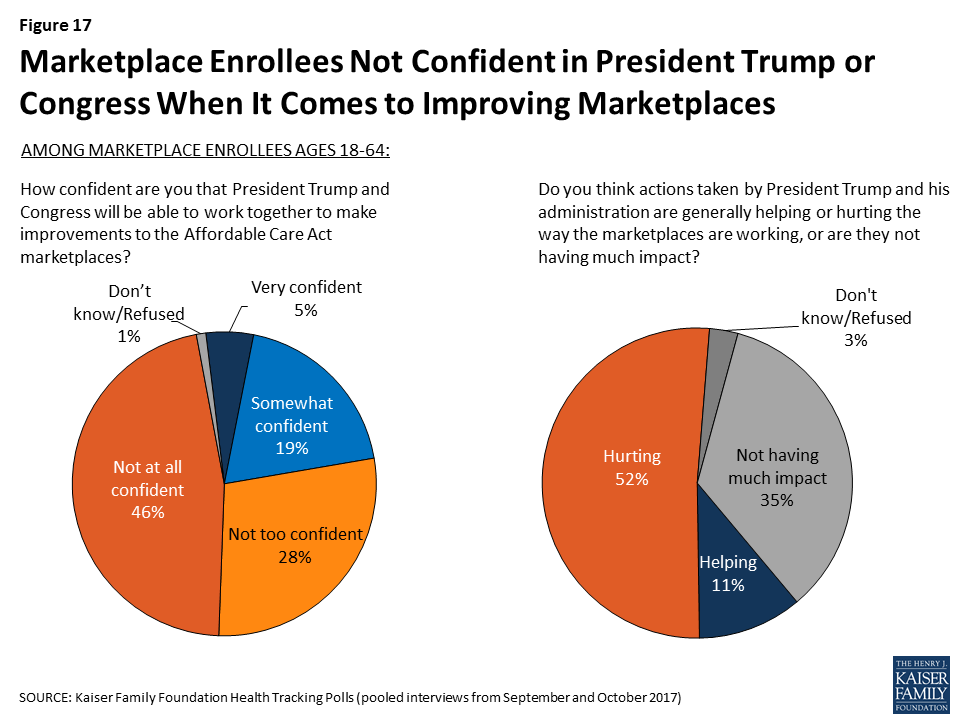

- In light of the ongoing debate about the stability of the ACA marketplaces, about one-fourth of marketplace enrollees are confident President Trump and Congress will be able to work together to improve the marketplaces. Among individuals who purchased plans through the ACA marketplaces, about three-fourths are either “not too confident” (28 percent) or “not at all confident” (46 percent) that President Trump and Congress will be able to work together to make improvements to the marketplaces.

Who Are Non-Group Enrollees?

This report examines people’s experiences with the current health insurance market, with a particular focus on individuals who currently have health insurance they purchased themselves (referred to as “non-group enrollees” throughout the report) which is comprised of individuals who purchase their own insurance through an Affordable Care Act (ACA) marketplace (“marketplace enrollees”) as well as those who purchase their insurance outside of the ACA markets.1 According to the most recent estimates, 10.3 million people have health insurance that they purchased through the ACA exchanges or marketplaces.2 For comparison, the report also examines individuals ages 18-64 without health insurance (“uninsured”) as well as those who get their insurance through their employer (“employer-sponsored insurance”). These extended interviews were conducted as part of the September and October Kaiser Health Tracking Polls and were completed prior to the beginning of the law’s fifth open enrollment period, which begins on November 1st.

The Next Open Enrollment Period

The start of the open enrollment period for non-group insurance in 2018 is less than one month away, and the majority of individuals who are targets for enrollment – those who currently purchase their own insurance and those who are uninsured – are unaware of the key dates of the next open enrollment period. One-third of non-group enrollees overall and 15 percent of the uninsured are aware of when the next open enrollment period begins. A slightly larger share (40 percent) of marketplace enrollees are aware of the November 1st start date for open enrollment, but still six in ten either give an incorrect answer or say they don’t know when open enrollment begins.

Similarly, the majority of the uninsured (95 percent), non-group enrollees overall (80 percent), and marketplace enrollees (75 percent) either give an incorrect answer or say they don’t know when open enrollment ends.3

Few Say They Have Seen Advertisements For Open Enrollment

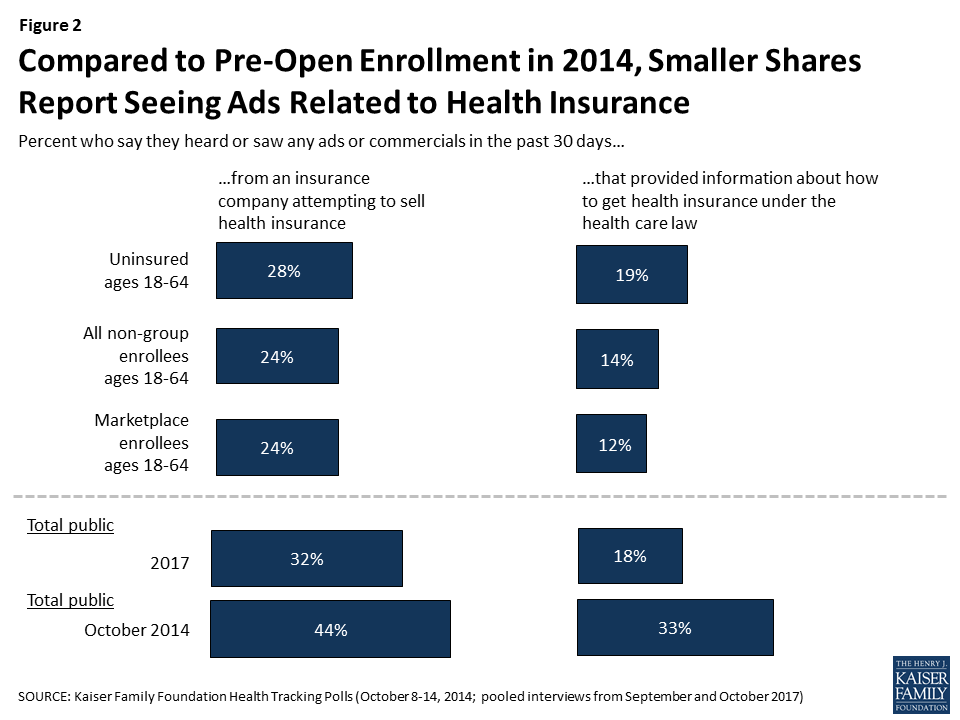

One reason why key populations may not be aware of the dates of the next open enrollment period may be because few report hearing or seeing any ads providing information about how to get insurance under the health care law. About one-fifth of the uninsured (19 percent) and one in ten non-group enrollees (14 percent) or marketplace enrollees (12 percent) say they saw ads in the past 30 days that provided information about how to get insurance. A somewhat larger share say they saw ads from an insurance company attempting to sell insurance in the past 30 days. About three in ten (28 percent) of the uninsured and about one-fourth of non-group enrollees overall (24 percent) and marketplace enrollees (24 percent) say they saw such ads.

Among the general public, the share who reports seeing such ads is lower than it was in the months leading up to the ACA’s second open enrollment period in 2014 (which began on November 15, 2014). Among the public overall, one-third (32 percent) in the October 2017 poll say they have seen ads from an insurance company attempting to sell health insurance in the past 30 days (compared to 44 percent in October 2014) and one in five (18 percent) say they have seen ads that provide information about how to get health insurance under the ACA (down from 33 percent in 2014).

Most Non-Group Enrollees Plan to Sign Up for Health Insurance in 2018

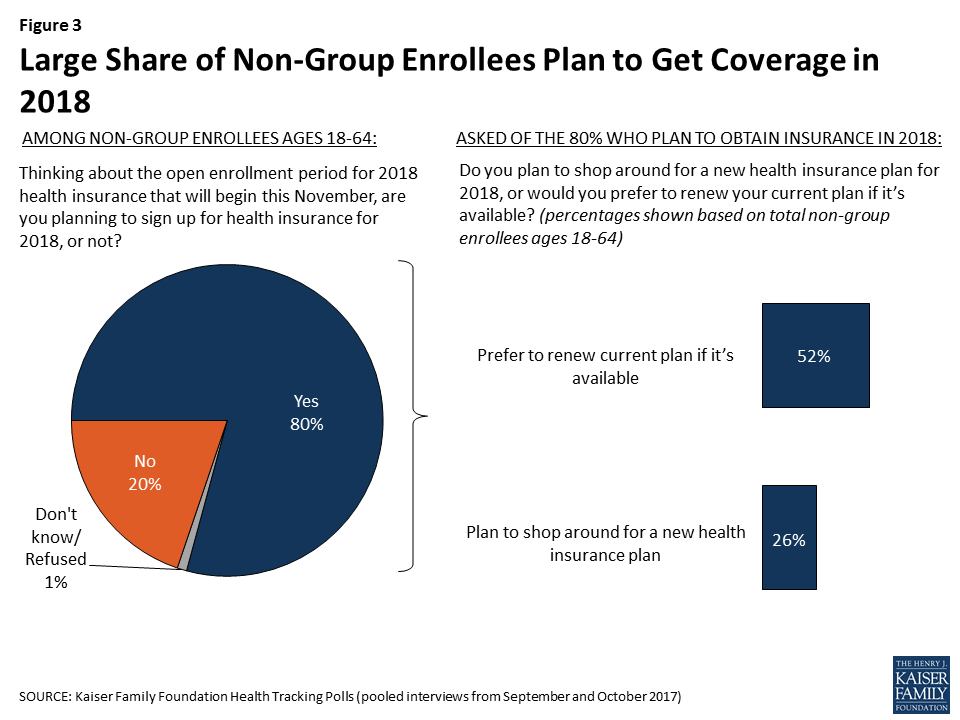

Despite the lack of awareness surrounding the dates of the next open enrollment period, eight in ten non-group enrollees say they plan to sign up for health insurance during the next open enrollment period and most (65 percent) prefer to renew their current plan if it is available while one-third plan to shop around. Similar shares of marketplace enrollees plan to sign up for health insurance in 2018 (85 percent) and 64 percent prefer to renew their current plan.

The Experiences of Individuals With Private Insurance

By focusing on marketplace enrollees, this report is able to compare the experiences of individuals who purchase their own insurance through an ACA marketplace with the current health insurance market to those who get their insurance through their employer. Overall, the experiences of marketplace enrollees are more similar than different than those with employer coverage when it comes to costs and choices. However, marketplace enrollees are more likely to express worry about their future ability to afford insurance and health care services.

Premiums and Cost-Sharing

While nearly half of non-group enrollees (48 percent) and marketplace enrollees (43 percent) say that it seems like their premiums have being going up lately, they are no more likely to say that than those with employer-sponsored insurance (51 percent). When asked about their deductibles and co-pay expenses, about half (49 percent) of those with employer-sponsored insurance say their cost-sharing has gone up lately, as do 43 percent of all non-group enrollees and 37 percent of marketplace enrollees.

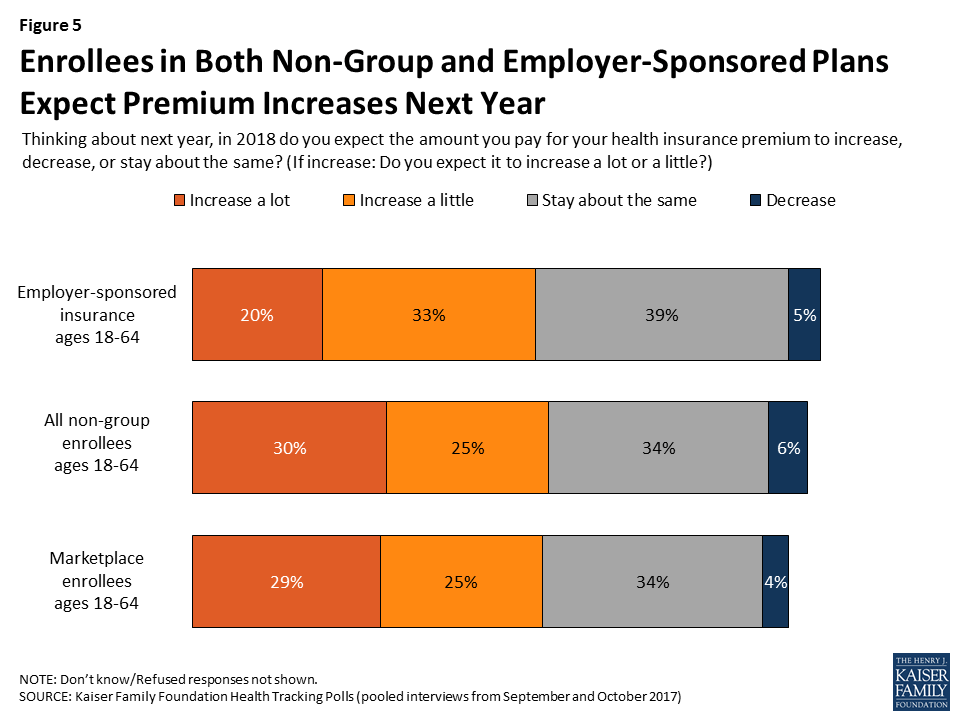

More individuals with private insurance – regardless of how they get their insurance – expect their premiums to increase either “a lot” or “a little” next year rather than decrease or stay the same. About six in ten (58 percent) non-group enrollees expect the amount they pay for their health insurance premiums to increase next year, as do 57 percent of marketplace enrollees and about half (54 percent) of individuals with employer-sponsored insurance. Three in ten non-group enrollees and two in ten of those with employer coverage expect their premiums to increase “a lot.”

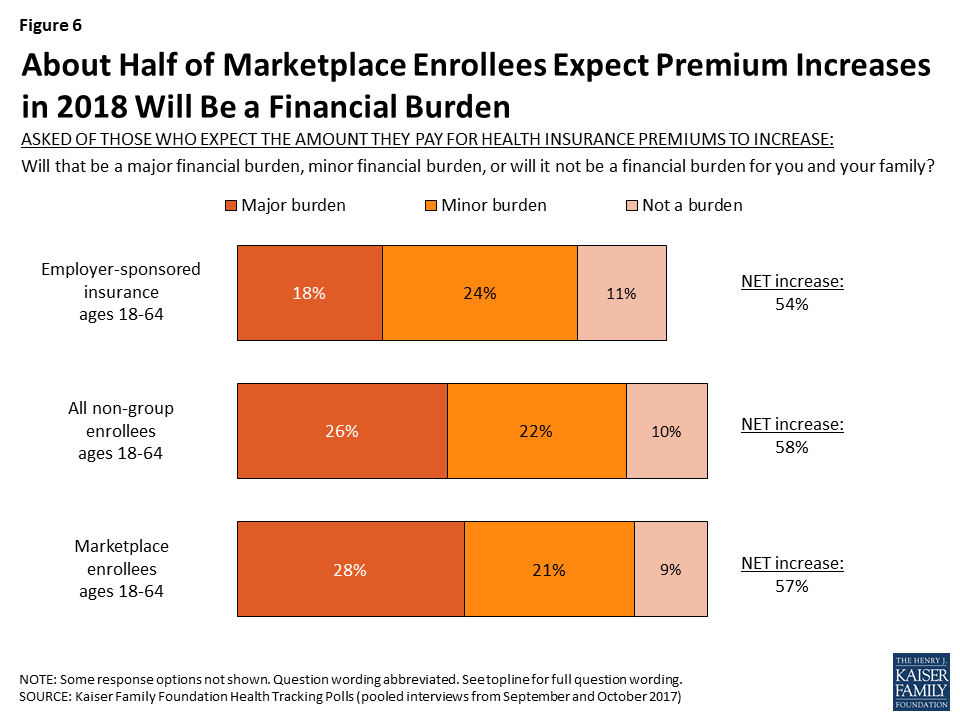

Among those who expect an increase in their insurance premium, most say it will be at least a minor financial burden on their family. About half of all non-group enrollees overall (48 percent) and marketplace enrollees (49 percent) who expect their premiums to increase next year expect this increase to be a financial burden, including about a quarter who expect it to be a “major burden.” A slightly smaller share (18 percent) of individuals with employer-sponsored insurance expect this increase to be a “major burden” while an additional 24 percent expect it to be a “minor burden.”

Choice of Plans or Insurers

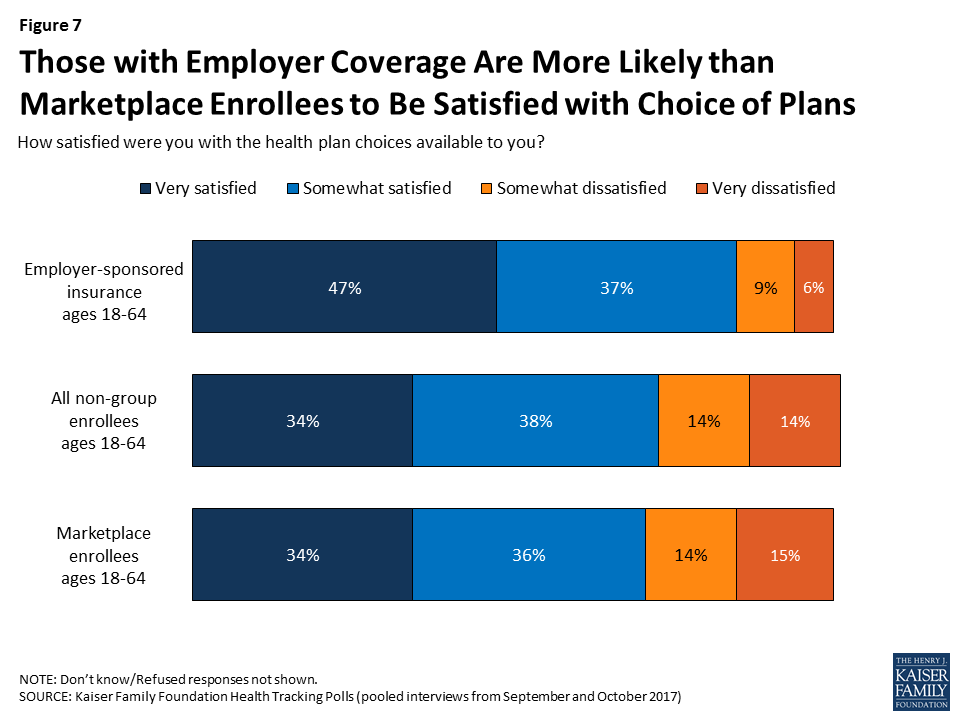

About three-quarters (77 percent) of those with marketplace coverage say they had a choice of health plans from different insurance companies when they bought their current plan, while about one-sixth (17 percent) say there was only one insurer selling plans in their area. Similarly, seven in ten (69 percent) of those with employer-sponsored insurance say they had a choice of different health plans while three in ten (29 percent) say their employer only offered one plan.

While a majority of all non-group enrollees (71 percent) and marketplace enrollees (70 percent) report being satisfied with their insurance choices with about one-third of each reporting being “very satisfied,” fewer marketplace enrollees report being satisfied as those with employer coverage. Individuals with employer-sponsored insurance are more likely to report being satisfied (85 percent) with nearly half (47 percent) reporting they are “very satisfied.”

Worries About The Cost of Health Coverage

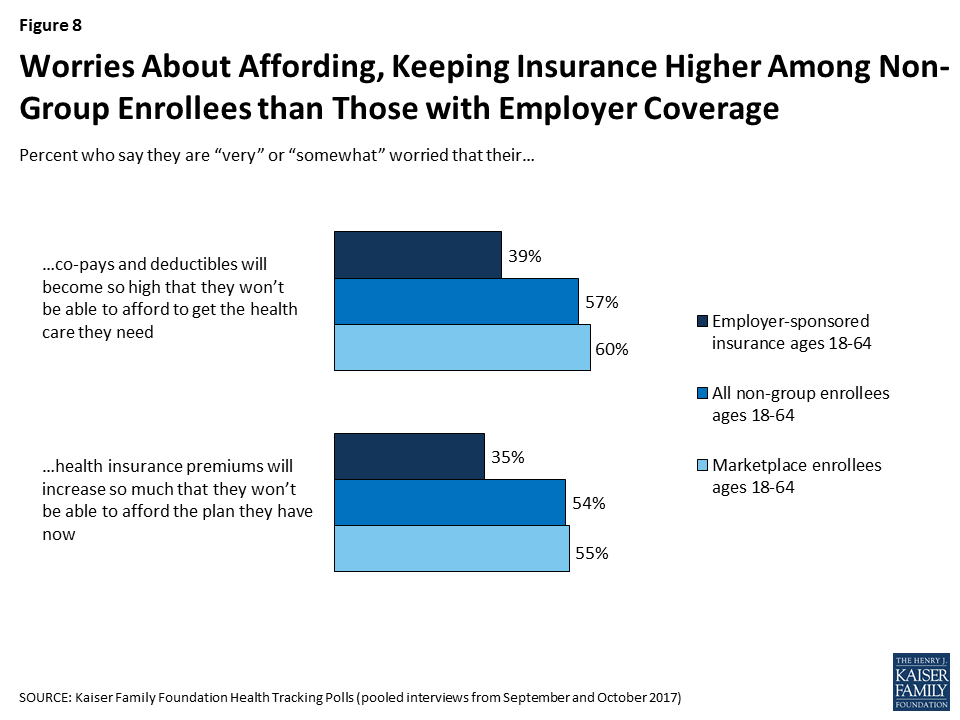

The survey indicates that those who purchase their own insurance are more likely than those with employer coverage to express worry about their future ability to afford insurance and health care services. Six in ten marketplace enrollees say they are worried that their cost sharing will become so high they won’t be able to afford their health care coverage. In addition, about half of marketplace enrollees (55 percent) say they are worried their premiums will increase so much in 2018 that they won’t be able to afford the plan they have now. Worries about increasing cost-sharing and premiums are lower among those with employer coverage (39 percent and 35 percent, respectively).

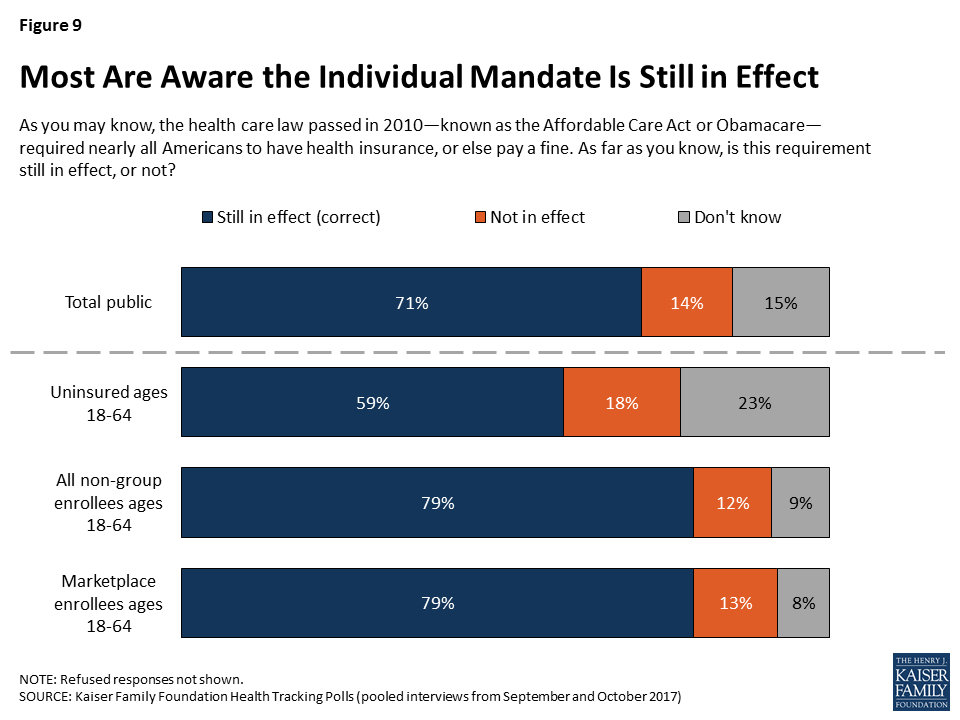

The Role of the Individual Mandate

The majority of the public (71 percent) – including eight in ten non-group enrollees (79 percent) and marketplace enrollees (79 percent) – are aware the individual mandate for all individuals to either have health insurance or else pay a fine is still in effect. While 59 percent of the uninsured are aware the individual mandate is still in effect, about one in five (18 percent) believe it is not in effect and one-fourth (23 percent) are unsure.

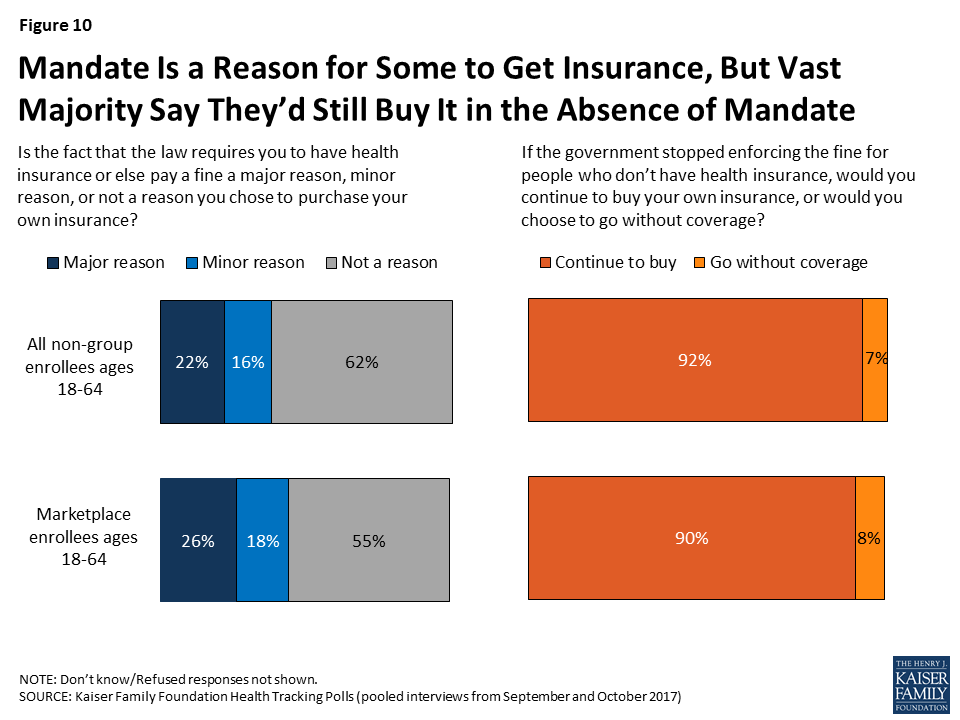

While most are aware the mandate is still in effect, few report that it is a strong motivator to buy their own coverage. While two in ten non-group enrollees overall (22 percent) and a quarter of marketplace enrollees (26 percent) say the fact that the law requires them to have health insurance or else pay a fine is a “major reason” they chose to purchase coverage, most (62 percent overall and 55 percent of marketplace enrollees) say it is “not a reason.” Further, the vast majority of both groups (92 percent and 90 percent, respectively) say they would continue to buy their own insurance even if the government stopped enforcing this requirement.

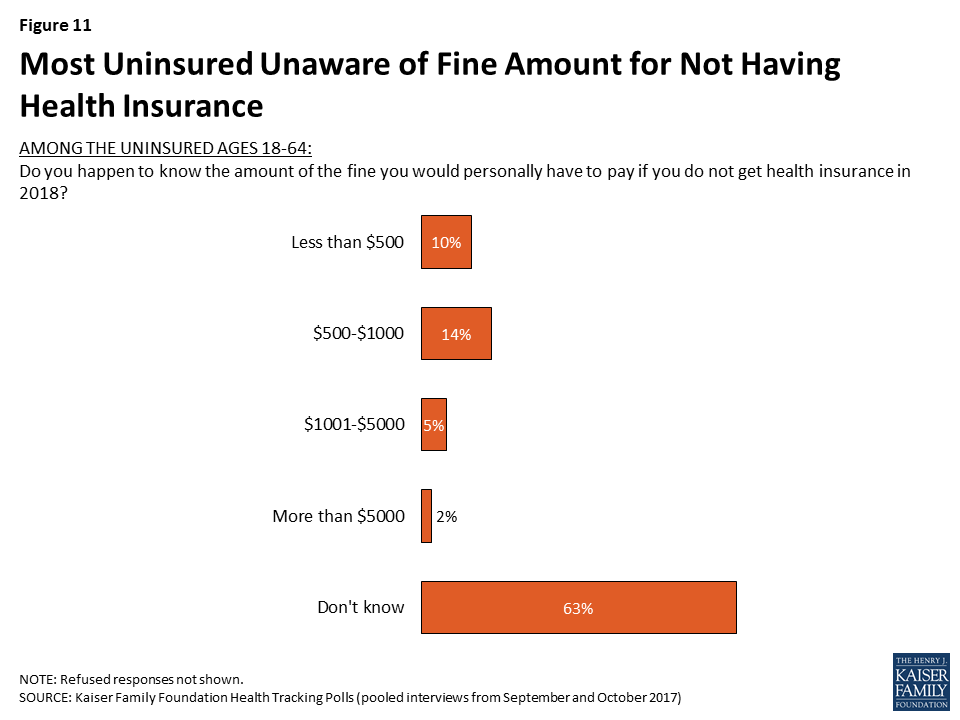

A lot of confusion remains over the amount of the fine individuals will have to pay if they don’t get insurance in 2018 with most uninsured (63 percent) unaware of the amount and some offering amounts as low as $25 and as high as $25,000.

The Experiences of the Uninsured

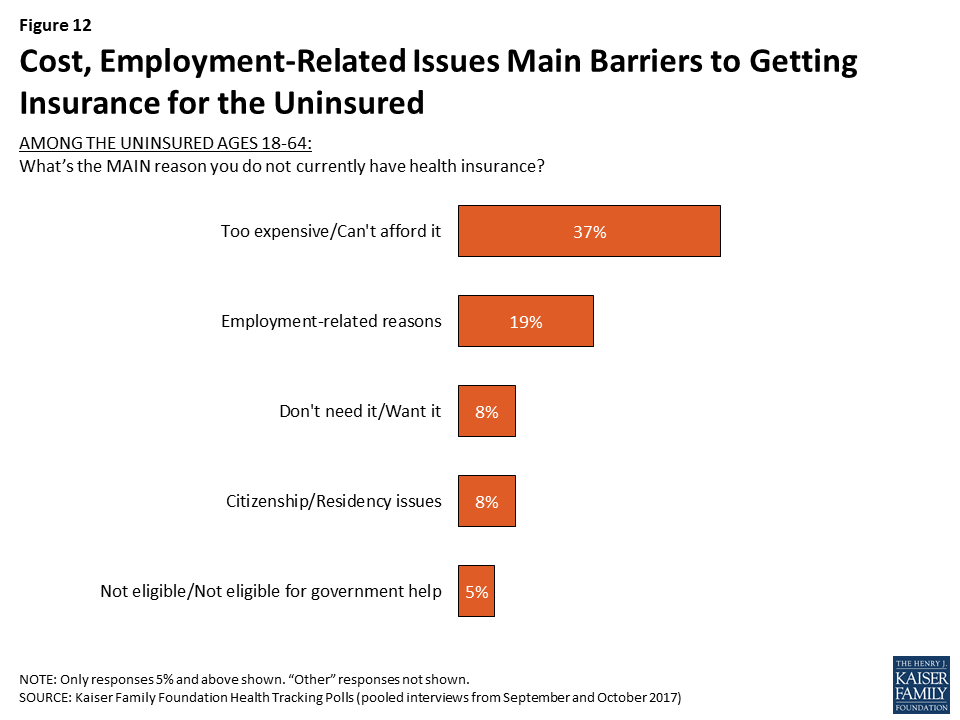

This report also examines the experiences of the uninsured, a group that is a potential target for marketplace enrollment. When the uninsured are asked about the main reason they don’t have coverage, the most common response offered is that it is too expensive and they can’t afford it (37 percent), followed by job-related issues such as unemployment or their employer doesn’t offer health insurance (19 percent). Fewer offer they don’t need or want health insurance (8 percent) or that citizenship or residency issues have prevented them from getting it (8 percent).

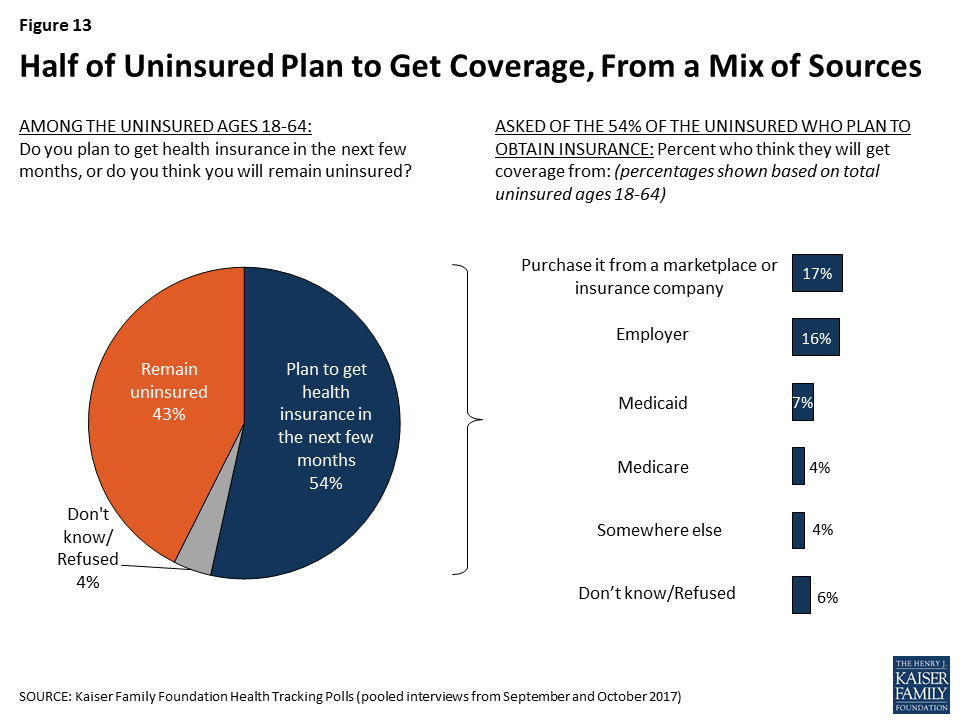

Just over half (54 percent) of the uninsured say they plan to get health insurance in the next few months, while four in ten (43 percent) expect to remain uninsured. Among those who plan to get insurance, one in five say they expect to purchase it from a marketplace or from an insurance company (17 percent) or say they expect to get coverage from an employer (16 percent). About one in ten (7 percent) say they expect to get coverage from Medicaid, the government health insurance and long-term care program for low-income adults.

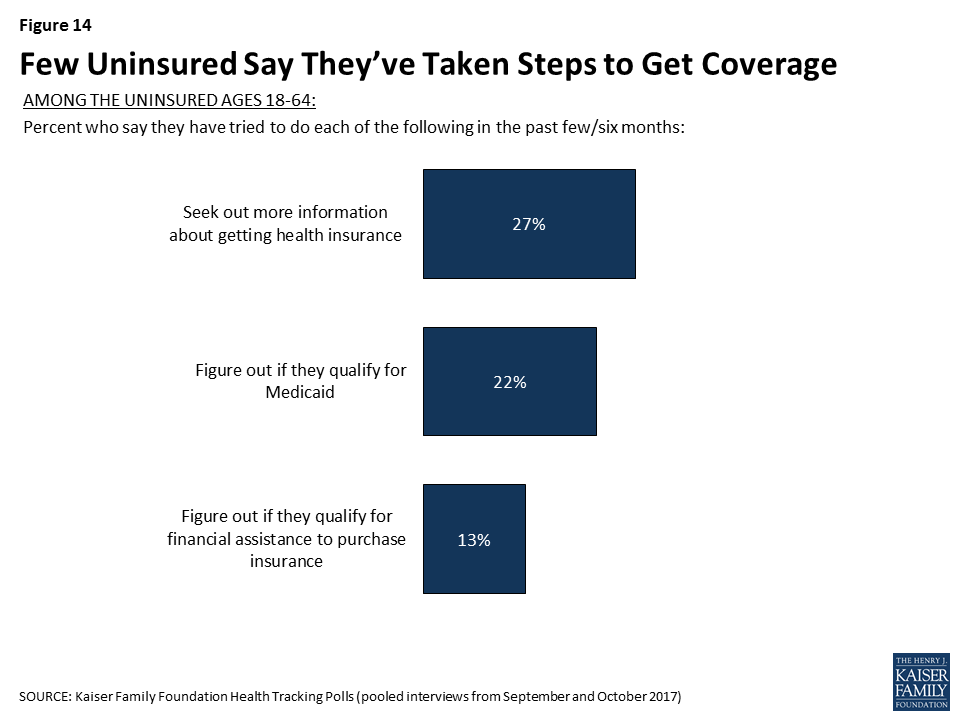

Despite the fact that over half of the uninsured say they plan to get health insurance in the next few months, few report having taken steps to get coverage in the past six months. About three in ten (27 percent) say they have sought out more information about getting health insurance, two in ten (22 percent) say they have tried to figure out if they qualify for Medicaid, and one in ten (13 percent) report they have tried to figure out if they qualify for financial assistance to purchase insurance on their own.

Current Views of the ACA Marketplaces

With the start of open enrollment less than a month away, this report finds there is still some confusion over the ACA marketplaces with the public unsure of the stability of these marketplaces and who is affected by issues within the marketplaces. In addition, the public has little confidence in President Trump and Congress to be able to work together to improve the ACA marketplaces.

Are the ACA Marketplaces Collapsing? Depends on Who You Ask

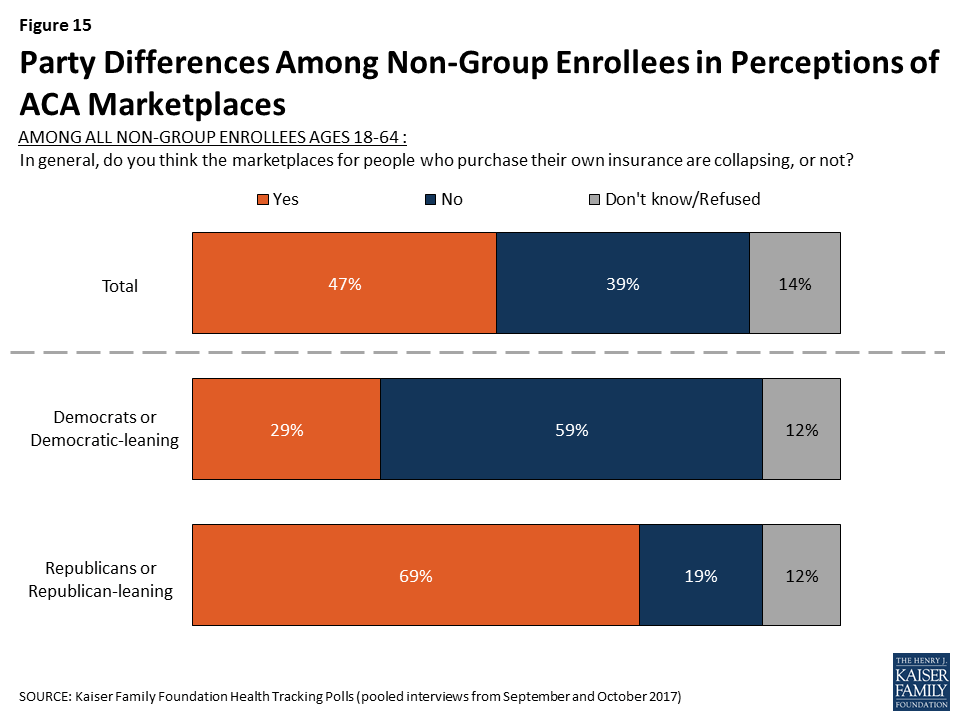

While many experts4 say the marketplaces where people can shop for insurance are not currently collapsing, about half of the uninsured (52 percent), the overall public (48 percent), and those who purchase their own insurance (47 percent) believe, in general, the marketplaces are collapsing. Attitudes about the health of the marketplaces across the country are largely driven by party, even among those who are enrolled in the non-group market. The majority of Republicans and Republican-leaning independents (69 percent) who purchase their own insurance believe the nation’s marketplaces are collapsing, compared to three in ten Democrats and Democratic-leaning independents (29 percent).

Worries about Future Insurers’ Participation in Marketplaces

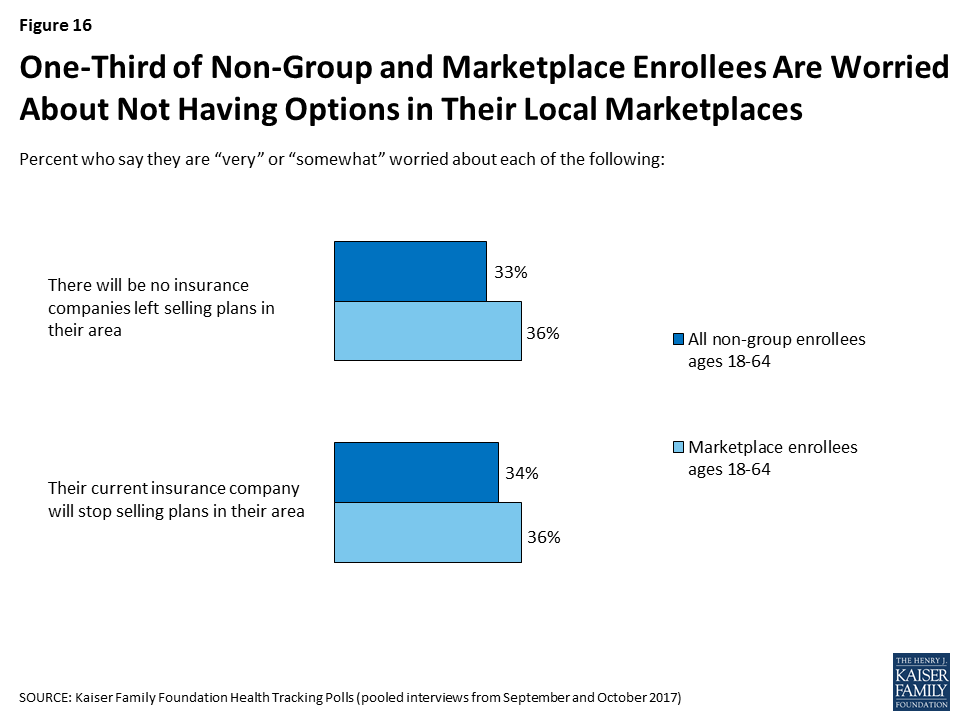

When asked about insurers’ participation in the marketplace in 2018, about one-third of non-group enrollees and marketplace enrollees report being worried that there will either be no insurance companies left selling plans in their area (33 percent and 36 percent, respectively) or their current insurance company will stop selling plans in their area (34 percent and 36 percent, respectively). In comparison, about one-fifth (18 percent) of those with employer-sponsored insurance are worried their employer will stop offering them health insurance.

Low Confidence in President Trump and Congress Working Together to Stabilize the Marketplaces

In light of the ongoing debate about the stability of the ACA marketplaces, few marketplaces enrollees are confident President Trump and Congress will be able to work together to improve the marketplaces. Among individuals who purchased plans through the ACA marketplaces, about three-fourths are either “not too confident” (28 percent) or “not at all confident” (46 percent) that President Trump and Congress will be able to work together to make improvements to the marketplaces. Fewer, about one-fourth (24 percent), express confidence in President Trump and Congress’ ability to work together. In addition, half of marketplace enrollees (52 percent) say the actions taken by President Trump and his administration are generally “hurting” the way the marketplaces are working. Fewer say the actions are either “not having much impact” (35 percent) or “helping” (11 percent) the marketplaces.

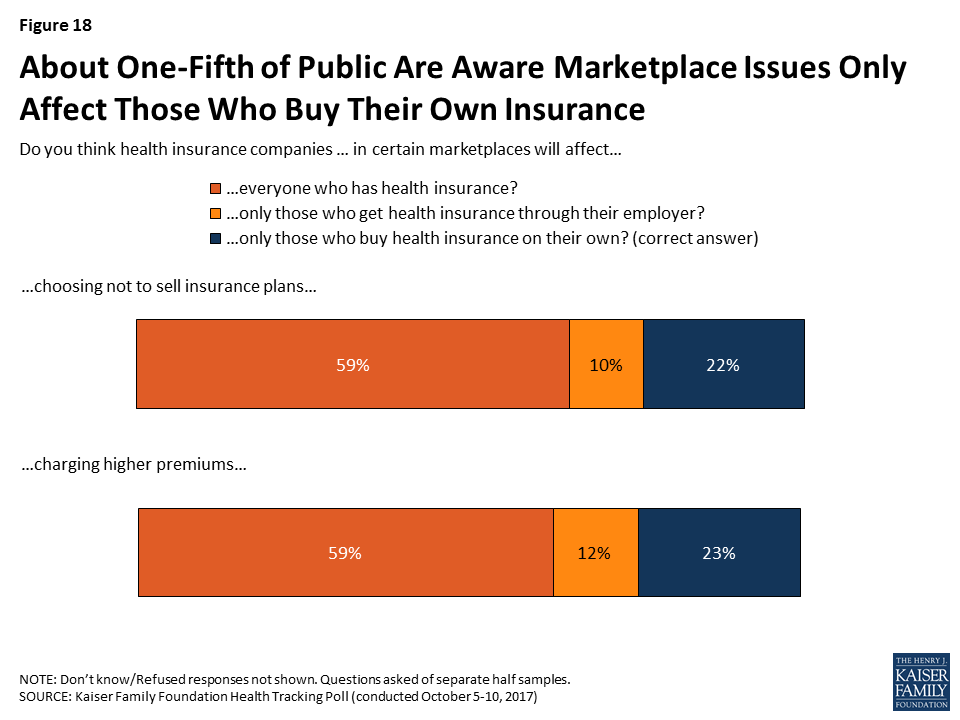

Uncertainty Remains on Who is Affected by ACA Marketplace Issues

Similar to previous surveys conducted by Kaiser Family Foundation, this month’s tracking poll finds about one-fifth of the public are aware that problems facing the ACA marketplaces only will affect those who buy health insurance on their own. When asked who will be affected by health insurance companies choosing not sell insurance plans in certain marketplaces, seven in ten incorrectly say it will affect either “everyone who has health insurance” or “only those who get their health insurance through their employer.” This is similar to the share who say the same about health insurance companies charging higher premiums in certain marketplaces.

Methodology

This survey was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). Interviews were conducted by telephone from September 13th-24th and October 5th-10th, 2017 among a nationally representative random digit dial telephone sample of 2,505 adult U.S. residents. This includes interviews conducted as part of the September and October Kaiser Health Tracking Polls, as well as an oversample of respondents who purchase their own insurance (Non-Group Enrollees). Computer-assisted telephone interviews conducted by landline (867) and cell phone (1,638 including 1,041 who had no landline telephone) were carried out in English and Spanish by SSRS. For the landline sample, respondents were selected by asking for the youngest adult male or female currently at home based on a random rotation. If no one of that gender was available, interviewers asked to speak with the youngest adult of the opposite gender. For the cell phone sample, interviews were conducted with the adult who answered the phone. KFF paid for all costs associated with the survey.

Respondents were considered Non-Group Enrollees if they were between the ages of 18-64 and their main source of healthcare coverage is health insurance that they purchase themselves (excluding small business owners whose self-purchased insurance covers non-related employees). To efficiently obtain a sufficiently large sample of Non-Group Enrollees, given their overall low incidence in the general adult population, the sample included a subsample of respondents who had previously completed interviews on the SSRS Omnibus poll, and indicated that they met the specifications of Non-Group Enrollees (n=111). All RDD landline and cell phone samples were generated by Marketing Systems Group (MSG). The SSRS Omnibus poll involves a similar overlapping frame design.

A multi-stage weighting process was applied to ensure an accurate representation of the national population overall, and of non-group enrollees in particular. The first stage of weighting involved corrections for sample design, including accounting for the likelihood of non-response for the re-contact sample, number of eligible household members for those reached via landline, and a correction to account for the fact that respondents with both a landline and cell phone have a higher probability of selection.

In the second weighting stage, demographic adjustments were applied to account for systematic non-response along known population parameters. First, interviews conducted as part of the Health Tracking Poll (excluding the Non-Group Enrollee oversample) were weighted to match estimates for the national population using data from the Census Bureau’s 2015 American Community Survey (ACS) on sex, age, education, race, Hispanic origin, and region along with data from the 2010 Census on population density and current patterns of telephone use from the July-December 2016 National Health Interview Survey. This weighted sample was used to estimate the population share of Non-Group Enrollees, as defined for this study. The combined sample of Non-Group Enrollees (from both the Health Tracking Poll and the oversample) was then weighted separately, and scaled down to the proportion of Non-Group Enrollees in the weighted general population sample.

No reliable administrative data were available for creating demographic weighting parameters for Non-Group Enrollees, since the most recent Census figures could not account for the changing demographics of this group, specifically as they are defined in this study. Therefore, demographic benchmarks were derived by compiling a sample of all respondents ages 18-64 interviewed on the SSRS Omnibus survey between March 1 and August 27, 2017 (N=24,818) and weighting this sample to match the national 18-64 year-old population based on the 2017 U.S. Census Current Population Survey March Supplement parameters for age, gender, education, race/ethnicity, region, population density, and marital status, as well phone use based on the most recent estimates from the National Health Interview Survey (NHIS). This weighted sample was then filtered to include respondents meeting the definition of Non-Group Enrollee (N=2,245), and the demographics of this group were used as post-stratification weighting parameters for the combined Non-Group enrollee sample. Finally, weighted samples were combined and a final adjustment was applied to account for the over-representation of Non-Group Enrollees in the sample.

The margin of sampling error including the design effect for the full sample is plus or minus 2 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

| Group | N (unweighted) | M.O.S.E. |

| Total | 2,505 | ±2 percentage points |

| Non-Group Enrollees ages 18-64 | 295 | ±7 percentage points |

| Age 18-64 with Employer Insurance | 935 | ±4 percentage points |

| Uninsured ages 18-64 | 206 | ±7 percentage points |

| Marketplace Enrollees ages 18-64 | 195 | ±9 percentage points |

Endnotes

- Sixty-six percent of non-group enrollees in this survey are marketplace enrollees. ↩︎

- Kaiser Family Foundation, as of October 12, 2017. http://modern.kff.org/health-reform/state-indicator/total-marketplace-enrollment-and-financial-assistance/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D ↩︎

- There are seven states that have open enrollment periods that end in January 2018 (CA, CO, D.C., MA, MN, NY, WA). For all other states, the open enrollment periods ends on December 31, 2017. ↩︎

- The Jama Forum, Is the Affordable Care Act Imploding? April 2017. https://newsatjama.jama.com/2017/04/17/jama-forum-is-the-affordable-care-act-imploding/ ↩︎