The Semi-Sad Prospects for Controlling Employer Health Care Costs

Our 27th employer health benefits survey is out. It’s a moment to reflect on the state of employer efforts to control health care costs because next year we, and others, expect employer premiums to rise much more sharply.

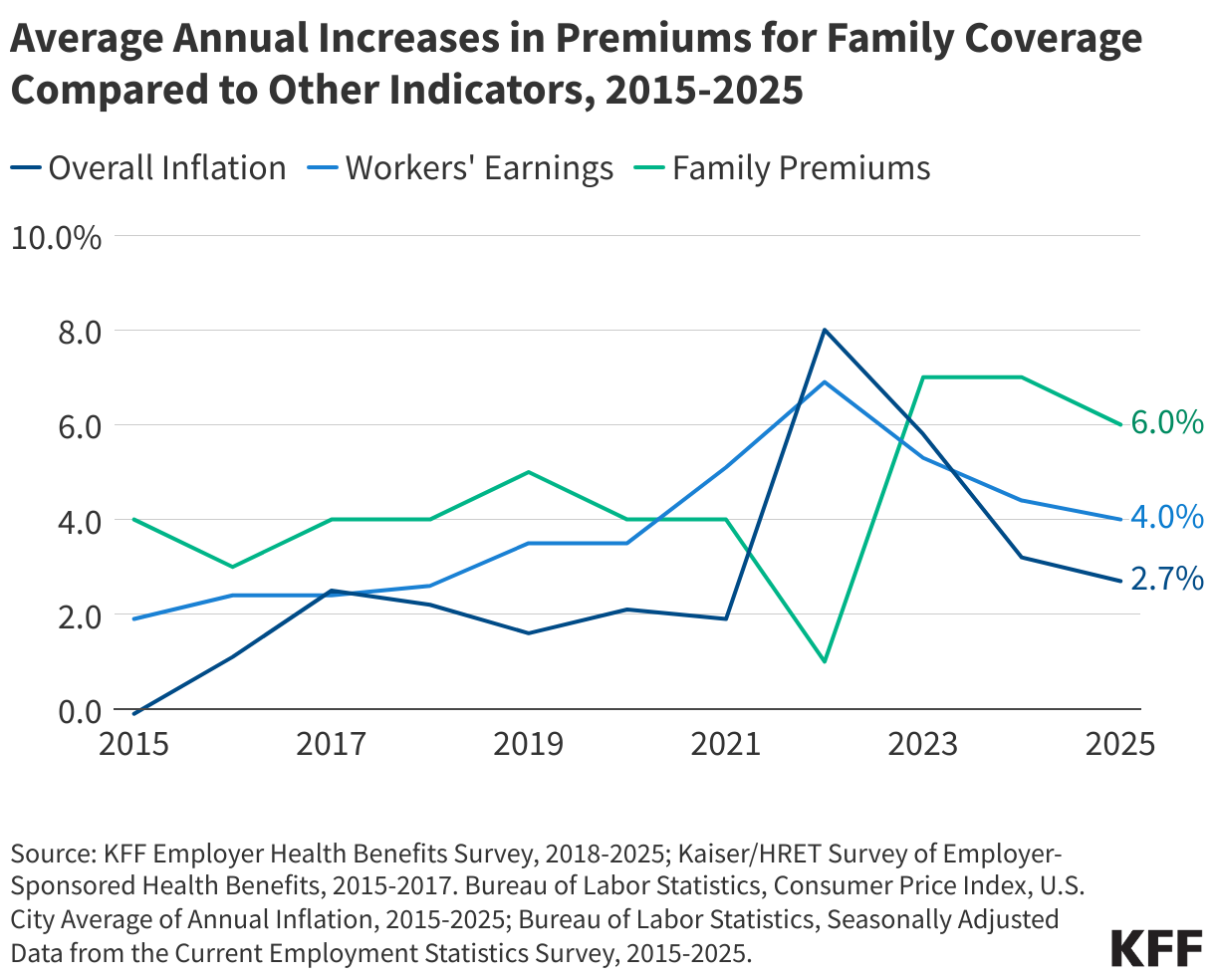

It may not feel like it to employers and employees, but in recent years, employer premiums have been relatively manageable, rising 6% on average this year for family coverage. That’s not a four-alarm fire for those of us who remember years of double-digit premium increases. Still, up is up and the absolute numbers are daunting for employers and employees – almost $27,000 on average for a family policy. You can buy a new Toyota Corolla Hybrid, every year, for less than that.

There is also a new cost challenge facing companies that cover GLP-1s for weight loss and other medical problems. Demand is high and companies are getting skittish about continuing the coverage without more limitations. Other companies are also watching their experiences.

But overall, the story has not really changed since I started studying corporate efforts to control health care costs when I was at MIT long before founding KFF, a time when it was normal for premiums to rise annually by double digits. Employers use everything in their toolbox to try to stem cost increases, but they stop short of using any strategy so much that blowback from employees causes the company a real problem. Employers are also lone actors in a sector that is fragmented without real bargaining power. They don’t have control over industry consolidation, rising prices, or the many other factors that drive their rising health care costs. The biggest companies, like Walmart, are often spread out across the country, diluting their bargaining power further and if they are not self-insured, limiting their choice of insurer. Smaller employers have limited ability to figure out what is driving their costs.

Corporations also have not meaningfully supported government cost-containment efforts over the years. That’s partly because corporate CEOs have too many other big problems to worry about. With the exception of a few who rise up from time to time, such as Howard Shultz at Starbucks or Walter Wriston decades ago at Citicorp, CEOs care far less about their health costs than their health benefits folks do; they have too many other fish to fry and too many personal ties with leaders in the health care system. Many are politically conservative and don’t support government regulation, or don’t want government regulating other aspects of their business, so they steer clear of it in health, too (think big tech). Overall, their bark far exceeds their bite.

This was the conclusion that colleagues and I reached in a study we published after interviewing countless CEOs about health costs when I was at MIT, wait for it, back in 1979:

“We found in our interviews that corporations were neither greatly concerned nor strongly motivated to do much about their health benefit costs. In our view, the opportunity for a close collaboration between business and government to contain health care costs simply does not seem to exist. To be sure, firms are no longer totally passive about health care costs; continual expenditure increases could provoke stronger action than what we have observed. However, firms are not now nor are they likely to be the force for system reform that some have imagined. Major corporations are under no illusion that they can do much individually to alter their health benefit costs. The benefits have long since been given to employees and cannot now be called back without risking more employee dissatisfaction than most of these firms appear willing to tolerate. Moreover, once the benefits are established, the level of costs the corporation will incur is largely determined outside the firm by health care providers, physicians, and hospitals interacting in the overall health care system. The firm’s ability to influence the system is not thought to be great. The political risks of attempting anything ambitious is believed to outweigh any savings the firm might achieve.”

A glitzy new initiative occasionally generates hype, such as when Amazon, Berkshire Hathaway and JP Morgan launched Haven Health. Predictably—to me—it fell apart pretty quickly and accomplished little.

Over the years, favorite strategies have come and gone, never disappearing but remaining in the toolbox with less hype surrounding them. Companies pushed HMOs until employees resisted tighter networks and utilization management. Chronic care management had its moment in the sun. Wellness programs—a catchall for many kinds of programs—rose in prominence and mostly crashed and burned. Companies have tried and continue to try price transparency initiatives to make employees better shoppers, with very limited success. Some large, self-insured firms directly contract with health systems or bypass PBMs and contract for drug purchases with outfits such as Mark Cuban’s Cost Plus Drugs. Employers have tried narrower networks, often dressed up as “higher performing networks” or with similar high-minded descriptions. That’s always a hard sell if the top hospitals and specialists are not available to your employees when they get sick. And then there is the tried-and-true strategy (really the only one) to quickly lower employer premiums—increasing cost sharing and deductibles. Deductibles increased sharply over the years but more recently have plateaued with smaller annual increases.

None of this means that corporate health benefits officers are not doing their utmost or that their company’s increases would not be somewhat higher without them. They face the realities of corporate politics and, ultimately, the value placed on health benefits by employees and management. They don’t control most of the drivers of the health costs they seek to moderate. They deploy the latest incremental delivery and payment reforms, but there is only so much they do to push back against a largely consolidated health care industry and rising prices. Consultants push the latest solutions on firms, who have little ability to separate the promise from the hype. (One promising initiative to help: https://phti.org/.)

Now there is a quiet alarm bell going off. With GLP-1s, increases in hospital prices, tariffs and other factors, we and pretty much everyone who monitors employer health costs expect employer premiums to rise more sharply next year. I am not predicting a return to low double-digit increases, but it would not shock me. Employers have nothing new to throw at the problem and that could result in a new wave of increasing deductibles and other forms of employee cost sharing, the strategy neither employers nor employees like but employers resort to in a pinch to produce quick savings. Rising premiums may also result in a temporary halt in the expansion of coverage for GLP-1s.

Meanwhile, the federal government just chopped a trillion dollars out of its own spending over the next 10 years for Medicaid, shifting spending burdens to the states, who are also trying to reduce their own health spending at the same time. None of these government spending cuts address rising health care prices or underlying health care costs or help employers or consumers with their health care bills. With the prospect that premiums may rise more sharply next year, cost containment could and maybe should be the next big health agenda item in Washington. A few states are doing what they can to mount hospital cost containment initiatives, but beyond pinprick solutions, there is no agreement about how to address the problem in Washington and little appetite for taking on the health care industry.