Which Congressional Districts Could See the Greatest ACA Premium Payment Increases?

Published: October 9, 2025

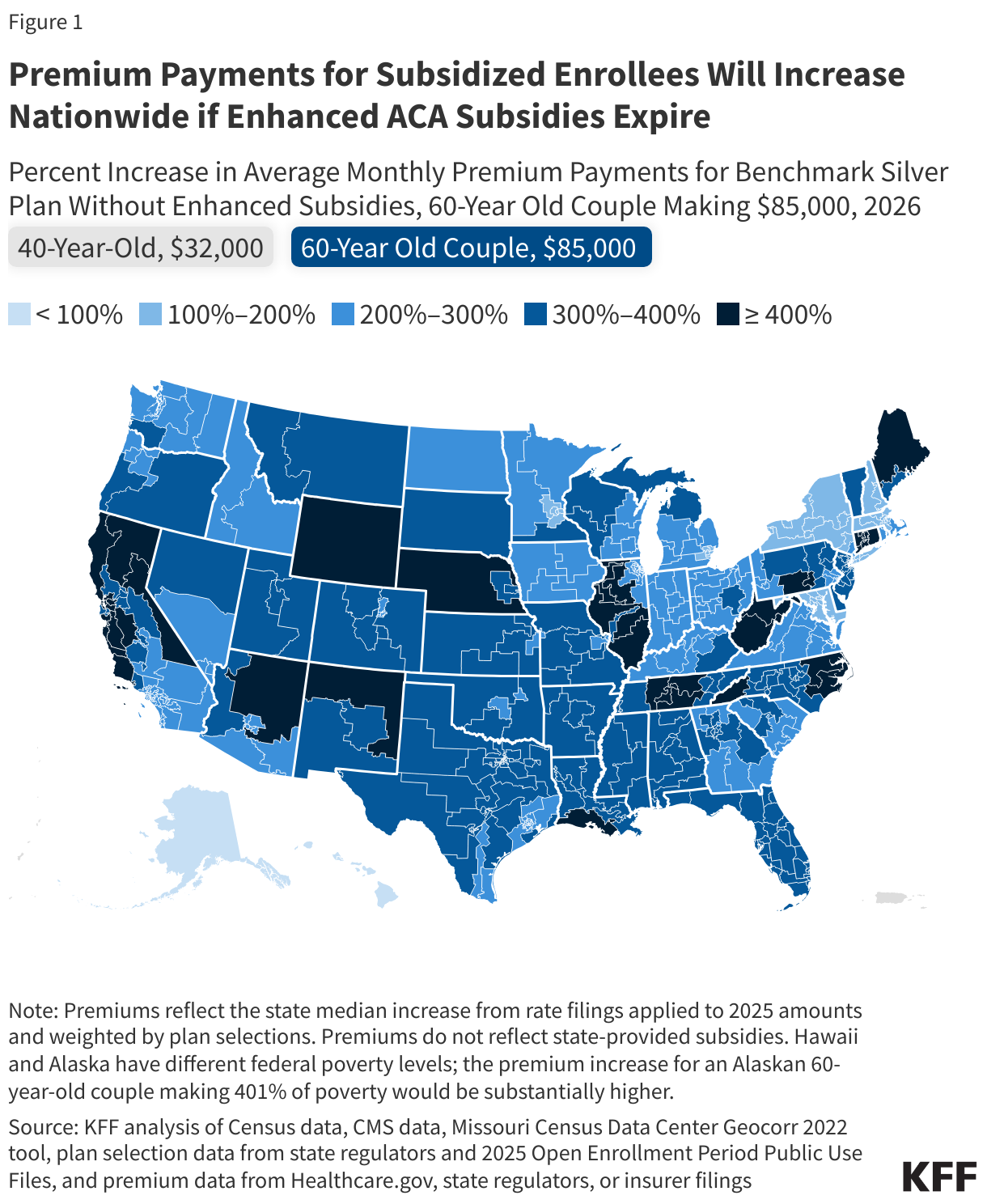

Nationally, individuals and families buying subsidized ACA coverage will see their premium payments more than double on average if the enhanced tax credits expire. Increases for out-of-pocket premium payments are not uniform, however, and older people with incomes over four times poverty would be hit hardest.

How enrollees would experience the premium changes in 2026 varies by income, age, and geography. Without the enhanced tax credits, the out-of-pocket premium for an individual, age 40, with an annual income of $32,000, would rise by $122 per month, or about three times the premium payment with enhanced tax credits. This increase will happen in most congressional districts, except Alaska and Hawaii due to their different poverty level guidelines. In Alaska, monthly premium payments would increase from $15 out-of-pocket to $129 if the enhanced tax credits expire, a similar dollar increase but a jump of nearly 800%.

Premiums would increase most for older adults making just over 400% of the federal poverty level, since they would no longer qualify for any premium tax credits. For a 60-year-old couple making $85,000 a year, losing the enhanced tax credits would increase their premiums by about $1,900 per month, based on a national average premium increase of 18%. There is wide variation in average state-requested premium increases and in insurance costs within congressional districts. Among the five congressional districts with the highest premium increases, premiums will increase by over 500%.

For a 60-year-old couple making $85,000, the congressional districts with the greatest increases per month:

- WY: 693% ($602 to $4,777)

- WV01: 654% ($602 to $4,540)

- WV02: 599% ($602 to $4,210)

- CT04: 537% ($602 to $3,833)

- IL12: 535% ($602 to $3,823)

The congressional districts with the smallest increases in the continental U.S. are all in New York, which uses community rated premiums:

- NY26: 110% ($602 to $1,265)

- NY23: 119% ($602 to $1,317)

- NY24: 142% ($602 to $1,457)

- NY22: 143% ($602 to $1,461)

- NY20: 150% ($602 to $1,505)

The map below shows congressional district level ACA Marketplace out-of-pocket premium increases should the enhanced premium tax credits expire, for a 40-year-old individual making $32,000, and a 60-year-old couple making $85,000.

In Florida, every congressional district will see enrollees over age 60, making just over 400% federal poverty level, face 2026 ACA premiums that would be, on average, at least four times as high if the enhanced premium tax credits expire. Similarly, this effect is predicted for these enrollees in all districts across Alabama, Arkansas, Connecticut, Delaware, District of Columbia, Florida, Louisiana, Maine, Mississippi, Montana, Nebraska, New Jersey, New Mexico, North Carolina, Tennessee, South Dakota, Utah, Vermont, West Virginia, and Wyoming.

The states with the lowest premium increases include Maryland and New Hampshire, where enrollees over age 60 and making $85,000 annually in all congressional districts would see premium increases under 200%.