Simulating the Impact of the Drug Price Negotiation Proposal in the Build Back Better Act

Issue Brief

The Build Back Better Act (BBBA), the budget reconciliation package that passed the House in November 2021 and is currently being considered by the Senate, includes a range of health and other proposals supported by President Biden, including a proposal to allow the federal government to negotiate the price of some prescription drugs covered under Medicare Part B (administered by physicians) and Medicare Part D (retail outpatient drugs). The negotiation proposal in the BBBA would apply to a limited number of drugs or biologics, as well as all insulin products. The negotiated prices for the first set of selected drugs covered under Part D would take effect in 2025. For drugs covered under Part B, the earliest negotiated prices could first take effect is 2027.

Compared to previous legislation passed by the House in 2019, the BBBA scales back the number of drugs that could be eligible for negotiation and also includes specific criteria for excluding drugs from the negotiation process. In additional to negotiating the price of all insulin products starting in 2025, the BBBA allows price negotiation for no more than 10 Part D drugs in 2025, 15 Part D drugs in 2026, 15 Part D and Part B drugs in 2027, and 20 Part D and Part B drugs in 2028 and later years. In contrast, the earlier proposal would have allowed the government to negotiate drug prices for up to 250 single-source Part B and Part D plus all insulin products. Both legislative proposals would negotiate prices only for those drugs lacking generic or biosimilar competitors. The BBBA also exempts drugs from the negotiation process if they are within several years of their FDA approval date – 9 years for small-molecule drugs and 13 years for biologics – an exemption not included in the earlier proposal.

This brief illustrates the potential scope of the drug price negotiation proposal in the BBBA. In the first part of our analysis, we show the 20 drugs covered under Medicare Part B and Part D that, along with all insulin products, would be subject to negotiation under the BBBA if the proposal was fully implemented this year (rather than in 2028). This analysis is designed to highlight the types of Medicare-covered drugs that could be subject to negotiation. Because the actual implementation date is 2025 (for Part D drugs) and 2027 (for Part B drugs), the list of Part B and Part D drugs that would be subject to negotiation if the BBBA was enacted would likely be different than what our analysis shows, since it would be based on future spending and market dynamics (in particular, the introduction of generic equivalents).

In the second part of our analysis, we show which of the current top-spending drugs covered by Part B and Part D could be subject to price negotiation, and in what years, starting in 2025 (Part D) and 2027 (Part B) when the BBBA proposal would take effect, assuming no generic or biosimilar entry in the intervening years. We also highlight which of the current top-spending drugs would not be subject to negotiation at any point due the BBBA provision that excludes drugs with generic or biosimilar equivalents from the negotiation process.

To derive our list of 20 negotiated drugs, we followed the selection process specified in the BBBA. Drugs were selected for negotiation if they ranked among the top 20 drugs in a combined ordering of Part B and Part D drugs based on Medicare drug spending data for 2019 (the most current publicly available data), ranked by total gross spending for drugs and biological products without generic or biosimilar equivalents, after eliminating products exempt from negotiation based on criteria specified in the BBBA. The gross spending amount used to determine top-spending Part D drugs under the BBBA includes Medicare spending and beneficiary liability but does not exclude the value of rebates. (See Methods for additional details on our analysis.)

Findings

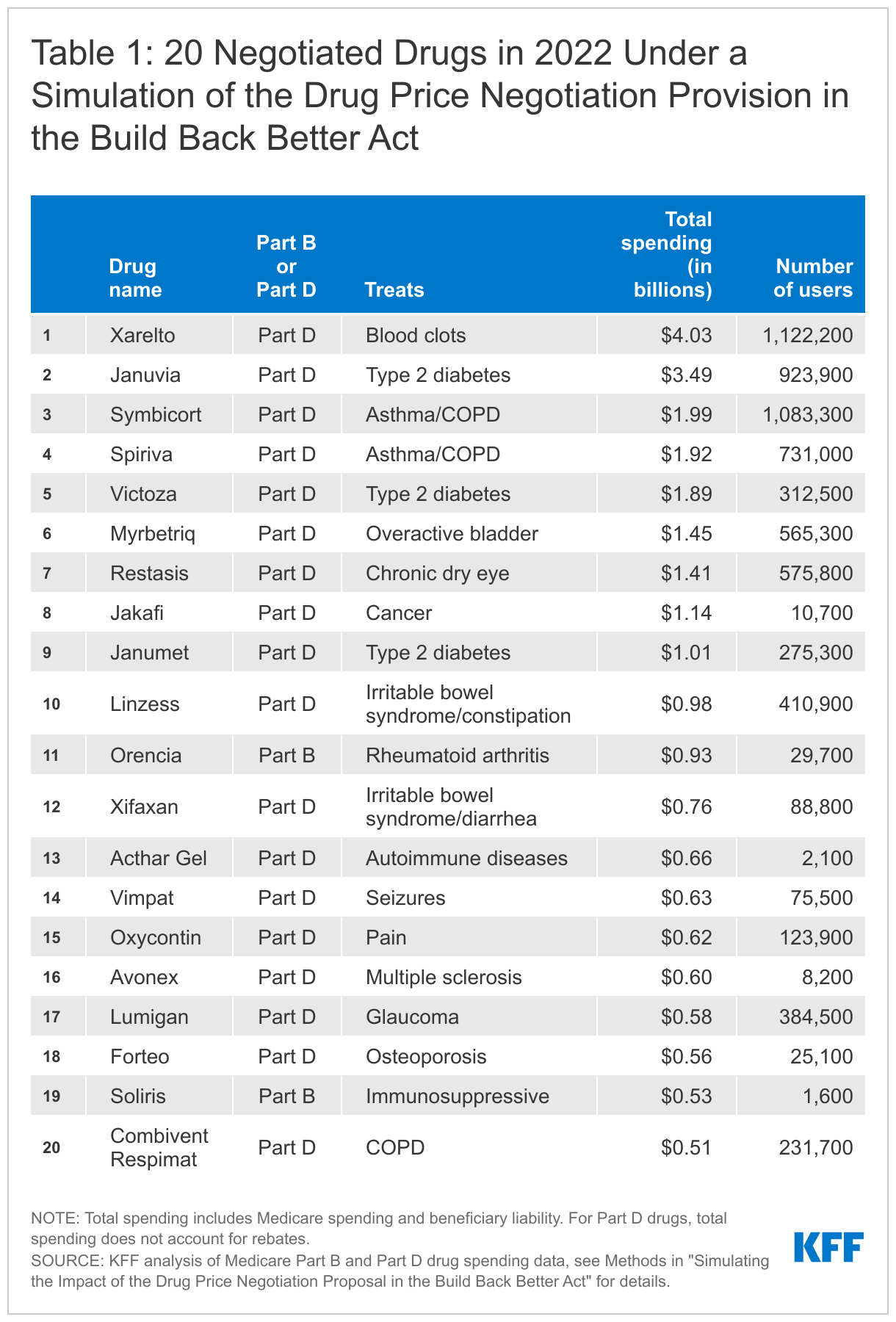

If the drug price negotiation proposal in the BBBA was fully implemented in 2022, the 20 negotiated drugs based on total gross spending would include 18 Part D drugs and 2 Part B drugs, in addition to 42 insulin products. These drugs were used by 8.5 million Medicare beneficiaries in 2019.

- Total gross spending on the 20 Part B and Part D negotiated drugs in our simulation in 2019 ranged from a high of $4.0 billion for Xarelto, a Part D drug used to treat blood clots, down to $0.5 billion for Combivent Respimat, a Part D drug for chronic obstructive pulmonary disease (Table 1). The number of beneficiaries who used these 20 drugs in 2019 ranged from a high of 1.1 million Part D enrollees using Xarelto down to 1,600 Part B enrollees using Soliris, an immunosuppressive drug.

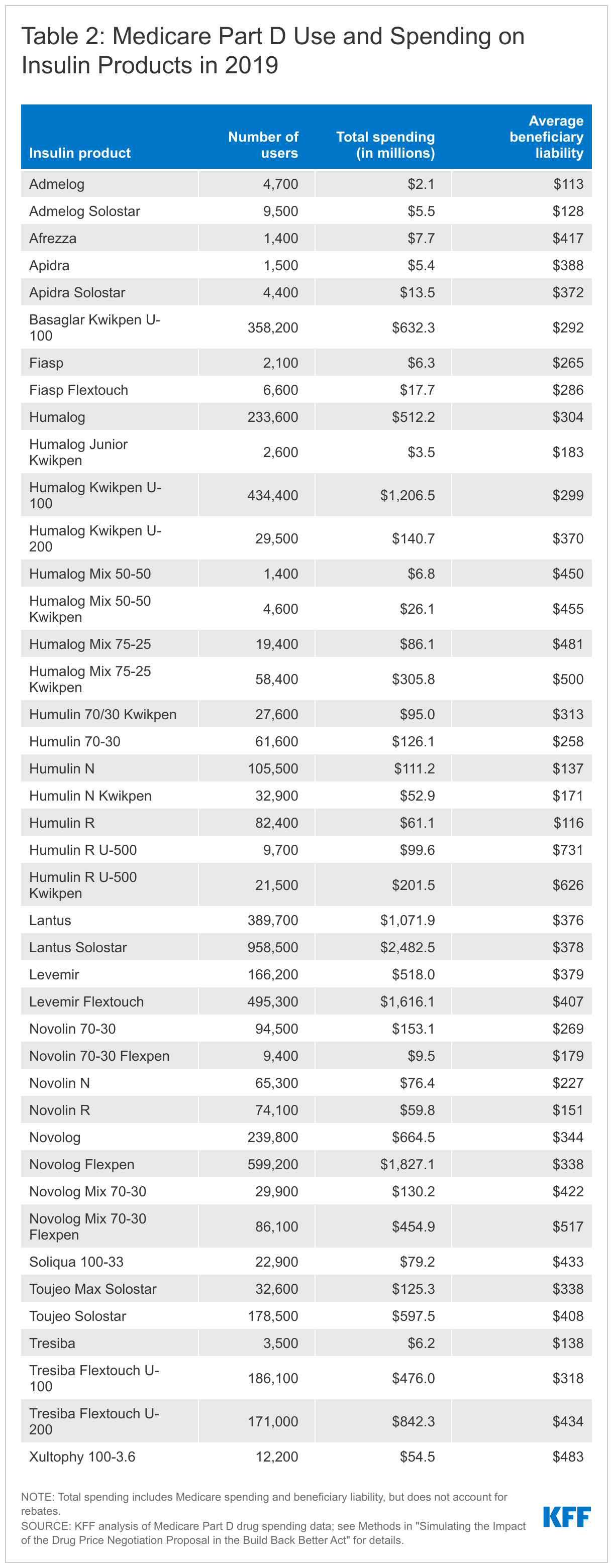

- In total, 3.2 million Medicare beneficiaries enrolled in Part D used one of the 42 insulin products covered under Part D in 2019 that would be subject to price negotiation, including 1.7 million beneficiaries who did not receive low-income subsidies (Table 2). In addition to the potential for cost savings attributable to lower negotiated prices, Part D enrollees who do not receive low-income subsidies may see lower out-of-pocket costs for insulin products based on the BBBA proposal requiring Part D plans to charge no more than a $35 monthly copayment or 25% of the negotiated price for insulin.

- Taken altogether, a total of 8.5 million Medicare beneficiaries in 2019 used one or more of the 20 drugs that would be subjection to negotiation based on their gross spending amount and the 42 insulin products that would also be subject to negotiation, accounting for nearly one in five (18%) of the 47.7 million Medicare Part D enrollees in 2019. This total includes 4.8 million beneficiaries who did not receive low-income subsidies, accounting for 14.4% of the 33.7 million Part D enrollees not receiving low-income subsidies in 2019.

Of the top 20 Part B drugs and top 20 Part D drugs with the highest total Medicare spending in 2019, negotiated prices could be available for nearly half of these drugs starting in 2025 for Part D drugs or 2027 for Part B drugs if no generics or biosimilars come to market and they remain among the top spending drugs.

- Among the top 20 Part D drugs ranked by total gross spending in 2019, 11 drugs would meet the criteria for negotiated prices beginning in 2025 and 1 would meet the criteria in 2028 if no generics or biosimilars come to market and they remain among the top Part D drugs by total spending (Table 3). (Note, however, that the BBBA only allows negotiated prices for up to 10 Part D drugs in 2025.) However, 8 of the top 20 Part D drugs would not qualify for negotiation at any time because they are a reference product for a generic or biosimilar. This includes several drugs with relatively high average out-of-pocket spending by Part D enrollees, such as Revlimid, Imbruvica, and Humira.

- Among the top 20 Part B drugs ranked by total spending in 2019, 7 drugs could be eligible for negotiated prices in 2027 and 6 could be eligible between 2028 and 2031 if no generics or biosimilars come to market, they remain among the top Part B drugs by total spending, and they rank high enough in a combined ranking of Part B and D drugs (Table 4). However, 7 drugs would not qualify for negotiation at any time because they are a reference product for a generic or biosimilar, including Part B drugs with relatively high average beneficiary liability, such as Rituxan, Alimta, and Herceptin.

Discussion

This analysis shows the potential reach of the BBBA drug price negotiation proposal, under the scenario that negotiated prices for 20 Part B and Part D drugs were to take effect in 2022, rather than in 2028. We find that most drugs selected for negotiation in our simulation would be Part D drugs, not Part B drugs. This is not unexpected since most Medicare-covered drugs are covered under Part D, rather than Part B. We also find that nearly 1 in 5 Part D enrollees in 2019 used one of the 20 negotiated drugs or 42 insulin products in our analysis. In addition, we find that more than half of the 20 Part B drugs and 20 Part D drugs with the highest gross total spending in 2019 would meet the criteria for negotiation between 2025 and 2028 (for Part D) or between 2027 and 2031 (for Part B) if no generics or biosimilars come to market. At the same time, many of the top-spending drugs covered under Medicare currently have generic or biosimilar equivalents, and therefore are not eligible for negotiation under the BBBA criteria.

Overall, our analysis suggests that the negotiation proposal in the Build Back Better Act could help to lower drug prices for some of the top-spending drugs covered under Medicare Part B and Part D, but some of the drugs with the highest total Medicare spending currently would be exempt from the negotiation process. These selection and exclusion criteria help to explain why the Congressional Budget Office estimated significantly lower 10-year federal savings from the drug price negotiation proposal in the BBBA (~$80 billion) compared to earlier legislation (~$450 billion).

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Tables

Methods

For this analysis, we simulated the process of selecting negotiation eligible drugs under the approach proposed in the Build Back Better Act (BBBA), using 2020 as the first year of selecting products for negotiation. Using the same two-year timeframe as the negotiation process in the BBBA, drugs selected for negotiation in 2020 would have their negotiated price available in 2022. We determine whether any of those drugs would be eligible for the negotiation process based on the approval date, orphan drug status and indications, whether the total expenditure exceeds the $200 million expenditure floor, and status as a reference product for a biosimilar/generic.

For top-spending Part B and Part D drugs, negotiation eligible drugs would be a selected drug in 2020 based on the following criteria:

- for biologics, approved/licensed prior to 2009 (since that is at least 11 years from a hypothetical February 1, 2020 selected drug publication date, assuming implementation in 2022 for this analysis)

- for small-molecule drugs, approved/licensed prior to 2013 (since that is at least 7 years from a hypothetical Feb 1, 2020 selected drug publication date, assuming implementation in 2022 for this analysis)

- does not have an approved generic/biosimilar

- is not designated as an orphan drug; has approved orphan drug designations for more than one rare disease/condition; or is past the orphan exclusivity period

- above $200 million in total Part B drug spending and total Part D spending combined

- is not derived from human whole blood or plasma

For drugs with multiple formulations and/or dosage amounts we combine the drugs into one and use the same criteria. We use the earliest, non-discontinued FDA approval date among the combined drugs and consider them to have a generic/biosimilar or orphan exclusivity if any one does. The BBBA provides some latitude to the Secretary of Health and Human Services for handling drugs with multiple formulations and/or dosage amounts which may result in differences with our methodology during a negotiation selection process.

To calculate the spending and count of beneficiaries for a drug, we used 2019 claims data for Part B drugs and 2019 prescription drug event data for Part D drugs from a 20% sample of Medicare beneficiaries, removing drugs taken by fewer than 11 beneficiaries in the sample. Part B claims include beneficiaries in traditional Medicare only; Part D claims include beneficiaries in stand-alone prescription drug plans and Medicare Advantage drug plans. Using HCPCS for Part B drugs, claims were pulled from the outpatient, carrier, and durable medical equipment (DME) files, removing packaged drugs, vaccines, and claims from Maryland hospitals, Critical Access Hospitals, and dialysis facilities. Data on the approval date, generic/biosimilar reference status, and orphan status come from the FDA Orange Book (for small-molecule drugs) and Purple Book (for biologics).

To derive the top 20 separately payable Medicare Part B drugs and top 20 Medicare Part D drugs by total spending in 2019, we adjust the spending and beneficiary counts to be representative of the population. For drugs with multiple formulations and/or dosages, we add the individual total spending amounts together and count the number of unique beneficiaries (if a beneficiary switched between formulations during the year, they would only be counted once). Total spending includes the amount paid by Medicare and the beneficiary liability amount. Part D spending does not account for rebates; however, under the BBBA, Part D drugs would be ranked based on total gross spending not accounting for rebates.