How do Health Care Costs fit into Family Budgets? Snapshots from Medicaid Enrollees

Key Takeaways

As the health care debate continues at the federal level and states pursue changes to their Medicaid programs through waivers, it is important to consider how health care costs fit into family budgets and how changes to Medicaid could affect family finances and access to care. Based on 21 interviews with Medicaid enrollees in five cities, this brief examines their family budgets, how health care costs fit into these budgets, and their views on how potential changes to health care could affect them. It finds:

- Most participants with Medicaid coverage are in a working family but live on very strained budgets with costs for basic needs taking up the majority of their monthly income. Participants are in low-wage jobs that often have fluctuating incomes, such as customer service representatives, retail workers, food service workers, daycare workers, home care attendants and warehouse employees. Those who are not working are caring for children or other family members, have a disability or serious health problem, are recently unemployed and seeking work, or are full-time students. Costs for basic needs such as housing, food, and transportation take up nearly all of their monthly income, and they often come up short on their monthly bills. Financial pressures cause them significant stress and anxiety, keeping them up at night and exacerbating health problems like depression and anxiety.

- Given their limited budgets, Medicaid is key for enabling participants to afford coverage and needed care. Most participants do not have access to or cannot afford employer-based coverage and were uninsured before they gained Medicaid. Some became eligible under the Affordable Care Act (ACA) Medicaid expansion; others qualify through eligibility pathways that existed before the ACA. Given their limited budgets, participants have little ability to pay for health care. They noted that they would not be able to afford coverage or care without Medicaid’s limited out of pocket costs. Participants reported getting needed care and generally were satisfied with their Medicaid coverage. Some pointed to challenges finding some specialists, such as psychiatrists, and some wished for broader vision and dental coverage for adults.

- Participants were concerned they would need to make trade-offs between paying for basic needs and going without care if their costs for health coverage and/or care increased. Participants noted that they do not have room in their budgets for increased health expenses. They pointed out that even small premiums or copayments could add up across family members or for multiple services or prescription drugs. Moreover, if they lost Medicaid, they do not think they would be able to afford other coverage. As such, increases in premiums or copays in Medicaid would likely lead to access barriers for these individuals and create further strain on their budgets. Similarly, these individuals would face higher costs in the form of premiums and cost sharing in Marketplace or other private plans.

Introduction

Low-income families face significant financial pressures and often struggle to cover expenses for basic needs each month. Health coverage is key for enabling individuals to access needed care and provides families with financial protection from the high cost of medical bills. Medicaid provides health coverage to over 74 million low-income parents, pregnant women, children, elderly individuals, and individuals with disabilities. As debate over health care continues at the federal level and states pursue changes to their Medicaid programs through Section 1115 waivers, insights into how health care costs fit into the family budgets of Medicaid enrollees are important to assess how changes to the program would affect family finances and access health care.

Most participants with Medicaid coverage are in a working family but live on very strained budgets.

This brief examines the family budgets of 21 Medicaid enrollees and explores how health care costs fit into their budgets. It also provides insight into enrollees’ views on how potential changes to health care could affect them. It builds upon a previous brief profiling Medicaid and Marketplace enrollees: How Would Proposed Changes to Medicaid and Marketplace Coverage Affect Real People? The findings are based on in-depth, in-person interviews conducted by the Kaiser Family Foundation and NORC at the University of Chicago during Summer 2017 with Medicaid enrollees in five cities (Richmond, Virginia; Kansas City, Kansas; Nashville, Tennessee; Portland, Oregon; and Albuquerque, New Mexico) and self-reported household income and expenses from interviewees. Interviews also were conducted with six uninsured individuals in these cities to understand how experiences vary between low-income individuals with Medicaid and those who are uninsured.

Medicaid enrollees were selected to provide for gender and racial/ethnic diversity and to represent enrollees eligible through a variety of eligibility pathways, including parents, pregnant women, adults with disabilities, and expansion adults in states that implemented the expansion. The locations provided geographic diversity and differing state decisions to implement the Affordable Care Act (ACA) Medicaid expansion to adults. Two cities were in Medicaid expansion states (New Mexico and Oregon), and three cities in states that have not implemented the expansion (Kansas, Tennessee, and Virginia).

Key Findings

Family Budgets

Most participants with Medicaid coverage are working or have a spouse or partner in the family that is working (Table 1). However, most of these jobs are low-wage positions that do not offer benefits or insurance, and many have fluctuating or seasonal hours that lead to varying income from month to month. Examples of these positions include customer service representatives, retail workers, food service workers, daycare workers, home care attendants, and warehouse employees. Many participants who are working part-time indicated that they would like to pick up more hours. Some participants said that their work schedule options are limited because they have to arrange work around when other family members can care for their children. They noted that this is an even larger challenge in the summer when children are out of school. Several participants indicated plans to go back to school to improve their job opportunities.

| Table 1: Profiles of Medicaid Enrollee Participants* | |||

| Expansion States | |||

| Kristina, 36, Albuquerque, NMGross Household Monthly Income:$2,605 (127% FPL)Household Size: 4Kristina lives with her boyfriend and two sons in a home that they rent from her parents. She works part-time in merchandising. After her son was diagnosed with autism, she left her full-time job to have more time to care for him. Her boyfriend works full-time as a pizza delivery driver. | Suzanne, 32, Albuquerque, NMGross Household Monthly Income:$2,663 (97% FPL)Household Size: 6Suzanne lives with her five children in a small home that she recently downsized to in order to save money. She is currently working as a brand ambassador, but her work options are limited because of a knee injury. Her goal is to go back to school to pursue a nursing degree. | Cheryl, 38, Albuquerque, NMGross Household Monthly Income:$1,815 (76% FPL)Household Size: 5Cheryl lives with her four children. Their primary source of income is social security survivor benefits received by her children. Her ability to work is limited because she is caring for one her sons who is facing behavioral health problems. | |

| Cynthia, 29, Albuquerque, NMGross Household Monthly Income: $1,250 (40% FPL)Household Size: 7Cynthia lives with her boyfriend and their five children in a house that was given to her boyfriend by his grandfather. She is a self-employed party planner and her boyfriend is a self-employed mechanic. | Joy, 56, Portland, ORGross Household Monthly Income: $0 (0% FPL)Household Size: 1Joy lives by herself and has one grown daughter. She is recovering from shoulder surgery. She hopes to return to her job as a caregiver once she recovers. | Ruthkeysha, 28, Portland, ORGross Household Monthly Income: $421 (18% FPL)Household Size: 5Ruthkeysha lives with her twin 9-year-olds, and their 7-year-old younger brother. She works as a caregiver for her grandmother who also lives in the home with them. | |

| Barbara, 23, Portland, ORGross Household Monthly Income:$1,100 (109% FPL)Household Size: 1Barbara lives with roommates. She works part-time as a caregiver for adults with developmental disabilities and hopes to go back to school to study industrial design. | Diana, 36, Portland, ORGross Household Monthly Income:$1,321 (78% FPL)Household Size: 3Diana lives with her two sons ages 3 to 16. She works part time as a home care aide. She is hoping to pick up more clients for additional hours of work. | Jeannie, 42, Portland, ORGross Household Monthly Income:$506 (25% FPL)Household Size: 4Jeannie lives with her boyfriend and two daughters. She is unable to work due to health problems and is applying for Social Security disability benefits. | |

| Non-Expansion States | |||

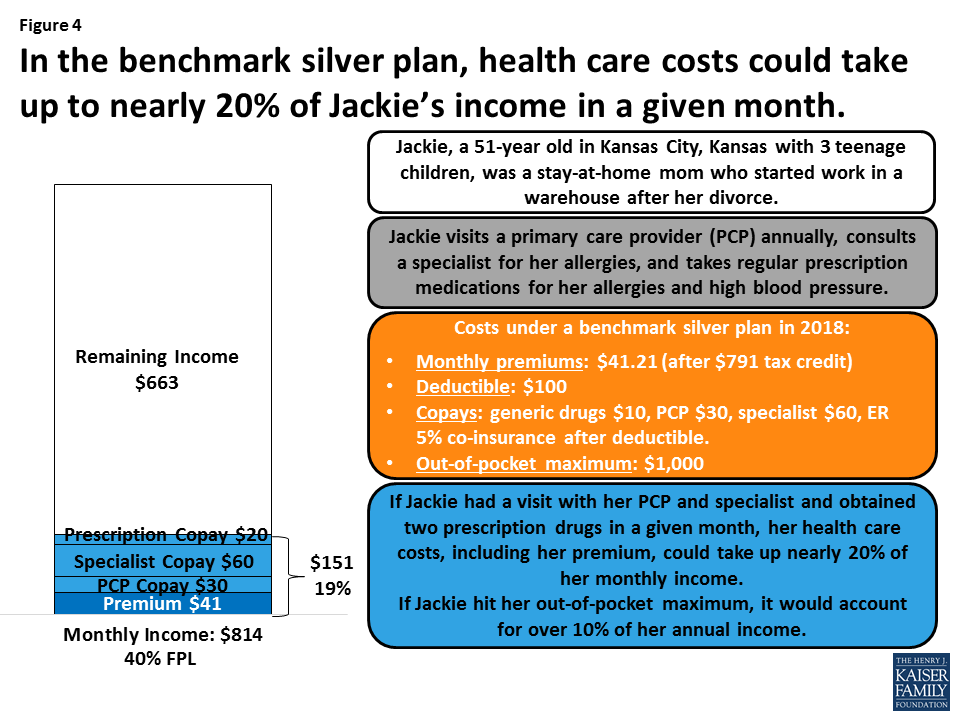

| Kimberly, 45, Kansas City, KSGross Household Monthly Income:$2,000 (98% FPL)Household Size: 4Kimberly lives with her boyfriend and two children ages 6 and 8. She is a stay at home mom but is looking into part-time options now that her youngest started school. Her boyfriend is a self-employed handyman. | Megan, 27, Kansas City, KSGross Household Monthly Income:$1,350 (66% FPL)Household Size: 4Megan lives with her 3-year-old son and twin 9-month-old girls. She was a stay at home mom but, after separating from the children’s father, began working part-time as a restaurant server. | Jackie, 51, Kansas City, KSGross Household Monthly Income:$814 (40% FPL)Household Size: 4Jackie lives with her three teenage children. She was a stay-at-home mom for 16 years but began working as a warehouse employee after her divorce. | |

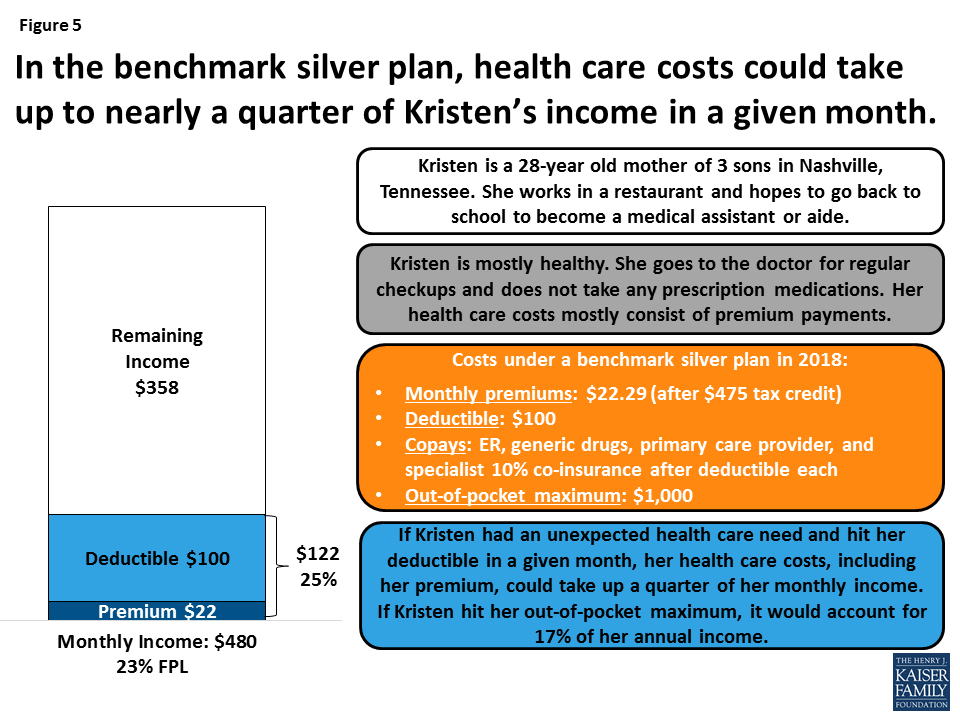

| Kristen, 28, Nashville, TNGross Household Monthly Income:$480 (23% FPL)Household Size: 4Kristen lives with three sons in her aunt’s home. She works in a restaurant but has difficulty finding hours in the summer with the children out of school. She hopes to go to school to be a medical assistant. | George, 44, Nashville, TNGross Household Monthly Income:$733 (73%FPL)Household Size: 1George lives on his own in a rented apartment. He became disabled in 2011 and currently lives on his fixed SSI disability payments each month. | Kristen, 27, Nashville, TNGross Household Monthly Income:$250 (10% FPL)Household Size: 5Kristen lives with her four children in the mobile home in which she was raised. She provides childcare in her home for several children. | |

| Nikki, 37, Richmond, VAGross Household Monthly Income:$900 (67% FPL)Household Size: 2Nikki lives with her 9-year-old son who has autism. She has been unable to work since 2011 due to serious health problems, including stomach cancer and a heart attack. Her son receives monthly SSI disability payments. | Amy, 33, Richmond, VAGross Household Monthly Income:$2,000 (98% FPL)Household Size: 4Amy lives with her three children, including her new baby. For the past 13 years, she has been working supervising a cleaning crew. She hopes to one day to go back to school to become a nurse. | Lydia, 48, Richmond, VAGross Household Monthly Income:$557 (27% FPL)Household Size: 4Lydia lives with her three daughters. She recently became unemployed and is searching for a new job. | |

| Note: *Some enrollees in expansion states are enrolled through traditional eligibility pathways (e.g., for parents and individuals with disabilities). Household income may be different from income calculated for Medicaid eligibility because it is gross income, includes income from all members of the household, and includes cash and food assistance. | |||

Participants who are not working are caring for children or other family members, have a disability or serious health problem, are recently unemployed and seeking work, or are full-time students. Individuals who are not able to work due to physical or mental health problems reported a variety of conditions, including congestive heart failure, post-traumatic stress disorder, bipolar disorder, arthritis, knee injuries, among others. Other individuals are caregivers for other family members who have extensive physical or behavioral health issues. Several individuals are going through difficult transitions in life, such as recent unemployment or separation from a spouse or partner. Those who are recently unemployed are in the process of looking for jobs.

“So a lot of times I will go without things like my phone… With the cost of food right now, sometimes it can get extremely high… So sometimes we have to cut back… we just can’t afford it anymore.”

– Lydia, Richmond

Participants reported facing major financial pressures and difficulty paying their monthly bills. Expenses for basic needs such as housing, food, and transportation take up nearly all of participants’ monthly income, and they often come up short on their bills and have to juggle and put off expenses. Several participants indicated that they sometimes turn to food pantries or charities. Participants noted that they live frugally to try to stay within their limited budgets, looking for savings and discounts and only buying what they need. They often go without things like cable, cell phones, or eating out and sometimes activities for their children. Despite the significant financial pressures these individuals face, a number said that they try to limit the help and resources they rely on because there are others with greater needs.

Participants reported no or limited savings to rely on when faced with unexpected costs. Without savings available, many noted that they sometimes turn to family for financial help when unexpected costs like car or home repairs arise. Those who do not have family available to help or whose families cannot always help sometimes use credit cards or short-term loans to pay for these expenses but then are left with debts that are difficult to repay.

Many participants reported having medical debt in collections, primarily acquired from a time when they were uninsured. Reported medical debts ranged from $300 to $30,000. In most cases, this debt was from when the individual or a family member received hospital care or surgery during a time when that person was uninsured. Most participants said they cannot afford to pay the debt and that it is in collections, negatively affecting their credit and limiting their ability to open bank accounts or make certain purchases, like a car. Some noted that their inability to pay these medical bills prompted them to prioritize obtaining health insurance in order to avoid large medical bills in the future.

“[The financial pressure] is just stressful because I already have PTSD and that always makes it worse.”

– Kevin, Nashville

Participants said that financial pressures cause them significant stress and anxiety, often keeping them up at night. Some participants noted that financial pressures exacerbate existing health problems such as depression or anxiety. Others said that their financial situation negatively affects their self-esteem and makes them feel like a failure or bad parent because they are unable to provide their children with the things they want or pay for their activities.–

MEDICAID COVERAGE SNAPSHOT: MELODIE, 23, RICHMOND, VIRGINIA

Melodie is a 23-year old mother who lives in Richmond with her three-year-old daughter. Melodie works full-time as a customer service representative. She works overnight hours so that her mother can watch her daughter since she cannot afford other childcare. Melodie reported that her household monthly income for April 2017 was about $600, which is about 43% of the poverty level for a family of two.

Even with full-time work, Melodie struggles to pay her bills every month as her expenses exceed her monthly income. Housing, food, and transportation take up nearly two-thirds of her income and she sometimes comes up short on her bills (Figure 1). Melodie also has $4,000 in medical debt, an amount nearly seven times her monthly income, from when she needed emergency care and surgery while previously uninsured. Her medical debt is in collections, which has damaged her credit and prevented her from being able to open a bank account.

After a period of being uninsured and not accessing care unless it was an emergency, Melodie enrolled in Medicaid. Her daughter also has Medicaid coverage. Melodie says Medicaid enables her and her daughter to get needed physical and mental health services. Melodie, who is expecting her second child, is receiving prenatal care as well as treatment for depression and anxiety. Her daughter receives behavioral health services for attention-deficit/hyperactivity disorder (ADHD) in addition to well-child checkups and other physical care. With Medicaid coverage, Melodie has few out-of-pocket health care expenses, although she does pay for some uncovered and over-the-counter medications.

Melodie says that she would not be able to afford the premium for a private plan given her limited budget and would be uninsured without Medicaid. Without coverage, she says she would have to put off care and rely on the emergency room because she would not be able to afford to pay for doctor’s visits. She is concerned that if her out-of-pocket costs for care increased and/or she lost access to Medicaid that she would no longer get all the care she needs and her depression may worsen.

Health Care Costs

“[Getting Medicaid was] very relieving. It felt like a weight lifted off my shoulders… Because you don’t have the money to pay out of pocket or go to the ER and get a thousand dollar bill later…. So when I finally got it, it was a big relief.”

– Kristen, Nashville

Most participants were uninsured before they obtained Medicaid and said they delayed and went without needed care due to cost when they were uninsured. While uninsured, they relied on emergency rooms for care that they could not put off, often resulting in large bills they could not pay. Some participants became eligible for Medicaid under the ACA Medicaid expansion to low-income adults and noted they would be uninsured without the expansion. Others qualify through eligibility pathways that existed before the ACA. Participants noted that they no longer had to delay care or rely on emergency rooms after gaining Medicaid. They also said that having Medicaid gives them peace of mind knowing they are protected from high costs if an emergency or unexpected health need arises. Some participants had private coverage prior to Medicaid but lost this coverage when they changed or lost jobs or aged out of their parent’s policy. Some noted that, when they had private insurance, they often had difficulty accessing care because of its higher out of pocket costs.–Given their limited budgets, Medicaid is key for enabling participants to afford coverage and needed care for themselves and their children. Participants noted that they have limited room in their already strained budgets for health care. Reflecting the Medicaid program’s limits on premium and cost sharing amounts, participants with Medicaid reported limited out of pocket costs for health care with no premiums and relatively low cost sharing levels. Some participants did report paying out of pocket for uncovered or over the counter drugs and/or items or services such as eyeglasses. However, others said they are foregoing uncovered services, such as glasses or dental care, because of costs. In addition, participants noted that they often confirm coverage of services before seeking them because of concerns about costs.–

“I don’t know what I would have done if my kids hadn’t had health insurance. Like, with how much care they’ve needed and how often they’ve been sick? I just can’t imagine them not having health insurance.”

– Megan, Kansas City

Participants with Medicaid reported getting needed care and were generally satisfied with their coverage. Most participants said they have a regular primary care provider and receive regular check-ups and screenings for themselves and their children. A number also said they see specialists to address mental and/or physical health issues. Some individuals have multiple and, in some cases, complex physical and mental health needs, including anxiety and depression, post-traumatic stress disorder, bipolar disorder, heart disease, high blood pressure, asthma, and cancer. In addition, some with substance and/or alcohol use disorders described how Medicaid provides them access to services they need to support their recovery. Despite being generally satisfied with their coverage, some wished they had broader dental and vision coverage, although those with children noted their children are able to get the dental and vision services they need with Medicaid. Some individuals pointed to challenges finding certain specialists, such as a psychiatrist and pain specialist; others said they do not have difficulty finding conveniently located providers who accept their insurance.

MEDICAID COVERAGE SNAPSHOT: TRACY, 38, ALBUQUERQUE, NEW MEXICO

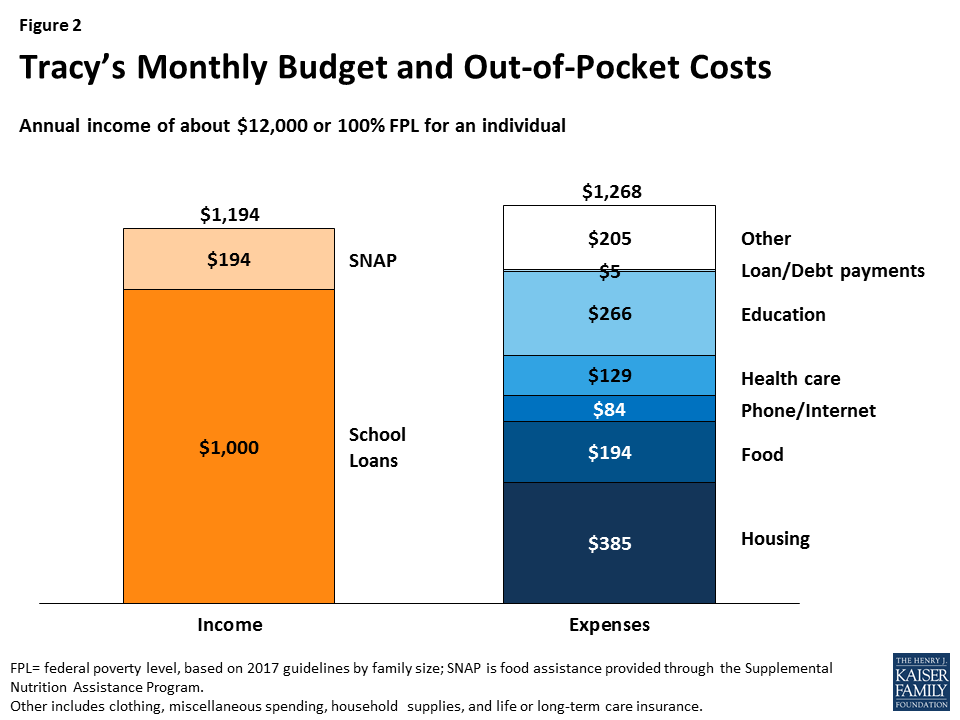

Tracy is a 38-year-old full-time student pursuing a teaching degree in Albuquerque, New Mexico. Prior to going back to school, Tracy was a janitor, but he now is pursuing his goal of teaching science to early elementary school children. Tracy receives $1,000 per month in student loans, which is about 100% of poverty for an individual. He has a part time job at the campus bookstore but does not currently have many hours due to the slower summer season. Tracy lives on a very tight budget, with housing and food constituting over half of his monthly income (Figure 2). He cuts back on expenses where he can, sometimes going without a phone to save money. While he tries to live within his limited budget, he sometimes comes up short on his bills.Tracy is eligible for Medicaid because New Mexico implemented the ACA Medicaid expansion, which expanded eligibility to adults with incomes up to 138% of poverty. Tracy enrolled in Medicaid in 2015 when completing a recovery program for substance use disorder. Before he had Medicaid, Tracy was uninsured. With Medicaid, Tracy is accessing services to support his substance use recovery, which has allowed him to pursue his goal of becoming a teacher. Because of his limited budget, Tracy does not think he would be able to afford very much in premium or cost sharing expenses. He currently pays out of pocket for some over the counter medications and his eyeglasses.

Though he hopes to have access to employer-sponsored insurance when he becomes a teacher, Tracy is grateful that Medicaid is available for him right now. Without the Medicaid expansion, Tracy would lose his Medicaid coverage. Tracy does not think he could afford a private plan and says he would not be able to access the services he needs to support his recovery without Medicaid coverage.

Views on Potential Changes to Coverage

“I wouldn’t have…the money to afford the copays and the medication…. It would affect my whole life, my son’s life, my family members’ lives, because that means they’re gonna have to help me and they’re already struggling as well.”

– Nikki, Richmond“I think [losing Medicaid would affect my health]. I definitely would be second guessing going [to the doctor]. I would second-guess even going…Yeah, it would definitely take a toll on my health.”

– Suzanne, Albuquerque

Most participants with Medicaid coverage had limited knowledge of potential changes to health care being discussed at the federal level but were fearful about facing increased costs or losing access to Medicaid. Participants said they would have difficulty paying higher costs for coverage or care. When asked about potential changes that could result in monthly premiums and/or higher cost sharing amounts, most indicated a willingness to pay but had concerns about being able to make consistent payments, especially since their incomes vary from month to month and they often come up short on their existing expenses. Similarly, some noted that cost sharing could quickly add up for multiple family members and/or when they need multiple services or prescription drugs. Some felt they would probably need to cut back on other expenses and/or go without needed care or medications if their cost sharing increased. Some said that their anxiety and depression would likely worsen if they could no longer afford care or their medications. When asked what would happen if changes made them and/or their children ineligible for Medicaid, participants said that they would not have another affordable coverage option and would likely become uninsured and be unable to access needed care.

How Experiences of Medicaid Participants compare to those who are Uninsured

Uninsured participants also are living on very tight budgets but, in contrast to those with Medicaid, are going without health care. Uninsured participants are working in low wage jobs without benefits that are similar to those in which Medicaid participants are employed. As a result, they face financial pressures that are similar to Medicaid participants, they often have difficulty paying their monthly expenses, and many report medical debt. Uninsured participants said they do not have affordable health coverage options available. Some were not aware of Marketplace or Medicaid coverage and had not explored those options. Others had looked at Marketplace options but felt the premiums and deductibles were unaffordable. However, in some cases, they were unaware of the tax credits available to help reduce costs. Without coverage, uninsured participants said they are going without care, including preventive screenings and primary care, and relying on home remedies and self-care options. A few reported using retail clinics or community health clinics when they could no longer put off care or had an injury and paid out of pocket for this care. Uninsured participants had very limited knowledge of potential changes to health care being discussed at the federal level and few thought that changes would affect their situation.

MEDICAID COVERAGE SNAPSHOT: KEVIN, 61, NASHVILLE, TENNESSEE

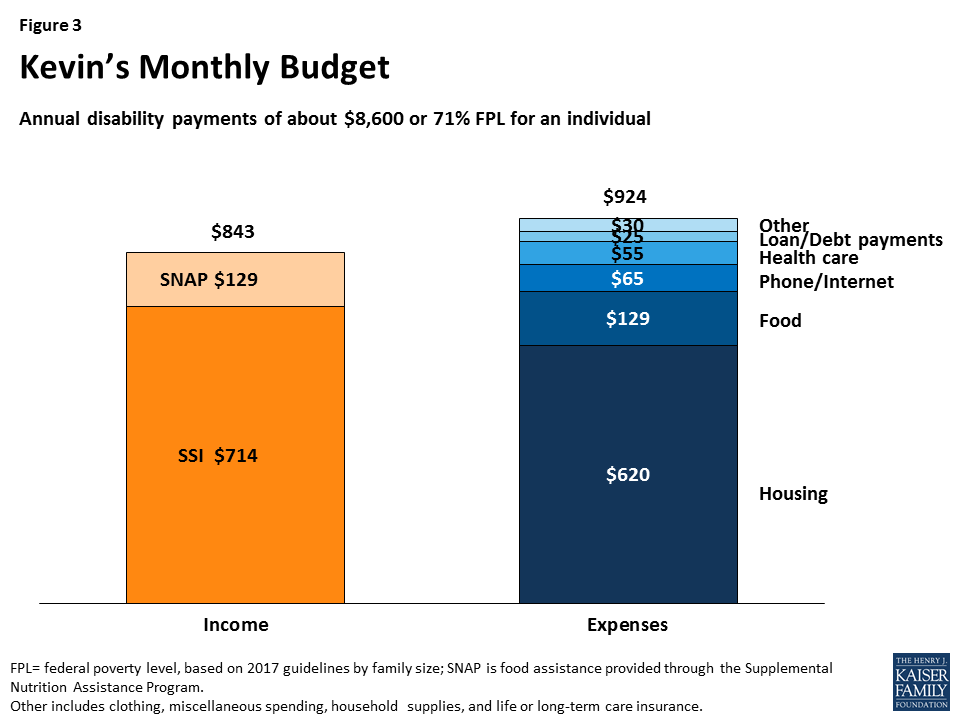

Kevin, 61, is an early retiree residing alone in Nashville. He has two older children ages 28 and 26. After 31 years in the business, he retired from working at a car dealership in 2010 due to health problems. After sustaining a traumatic injury, Kevin suffers from post-traumatic stress disorder (PTSD) and is unable to work. He also suffers from chronic obstructive pulmonary disease and has high blood pressure.Kevin lives on a fixed monthly Supplemental Security Income (SSI) disability payment of $714, which is about 71% of poverty for an individual. Kevin lives in a boarding house to reduce costs and prioritizes paying rent, which alone takes up nearly all of his monthly disability payment (Figure 3). He often comes up short on his bills and says he forgoes eating out and some basic items, pointing to instances where he could not afford a razor for himself or a Mother’s Day card for his mother. Kevin has medical debt from cost sharing amounts he could not afford when he previously had coverage through his private employer plan. Kevin says his financial pressures exacerbate his PTSD.

Kevin has had Medicaid coverage since 2012. He was uninsured for two years after retiring from his job before he enrolled in Medicaid and noted that he did not access care while he was uninsured due to cost. Kevin says, with Medicaid, he now accesses primary care and sees specialists to address his physical and behavioral health needs, although he wishes for broader coverage to address his dental needs. Medicaid covers five of his six prescription medications; he pays for the remaining medication out of pocket. Kevin says that if he had to pay more for health care, he would have to go without some medications since he would not be able to afford to pay for them all.

How Medicaid Enrollees Would be Affected by Increased Health Care Costs

Under Medicaid, enrollees have limited out of pocket costs for health care with no premiums and relatively low cost sharing levels. Given the limited incomes and financial pressures currently facing these Medicaid enrollees, increases in premiums or copays in Medicaid would likely lead to access barriers for these individuals and create further strain on their family budgets. Similarly, these findings suggest that these individuals would face challenges paying premiums and out of pocket costs for Marketplace or other private coverage. For example, if Medicaid enrollees like Jackie and Kristen moved to a Marketplace plan in 2018 and had health care needs, in a given month, health care costs could take up a significant share of their income.

Conclusion

Despite primarily living in working families, these Medicaid enrollees are facing major financial pressures and many struggle to pay their bills each month. Expenses for basic needs take up nearly all of their monthly income, most have little to no savings, and many have medical debt from times they were uninsured. Given their already strained family budgets, these Medicaid enrollees have little ability to pay for health care. As such, Medicaid coverage is key for enabling them to afford coverage and care for themselves and their children.

Most of these enrollees have limited knowledge of the potential changes to health care being discussed at the federal level, but many are fearful about losing access to Medicaid or facing increased costs for their coverage and care. Enrollees do not think they would be able to afford coverage without Medicaid, including those who became eligible through the ACA Medicaid expansion. Moreover, they indicate it would be challenging to pay premiums or higher cost sharing, and they would likely have to make difficult trade-offs between health care and other basic needs if costs increased. As such, these individuals would likely face significant challenges if they faced increased costs in Medicaid or were moved to Marketplace plans where they faced higher premium and out-of-pocket costs.