How Might Expiring Premium Tax Credits Impact People with HIV?

ACA premium tax credits, which make health insurance Marketplace plans more affordable, were first enhanced as part of the American Rescue Plan Act in 2021 and then extended by Congress through 2025. The enhanced credits have improved insurance coverage affordability for millions of people, including those with HIV. However, they are currently set to expire at the end of the year, unless Congress acts to extend them. Their extension became a major political issue playing a role in the government shutdown. In addition, because of the political uncertainty surrounding their extension, health insurers have proposed premium increases beyond what would otherwise be the case. The loss of the enhanced tax credits, coupled with increased premiums for some, could jeopardize coverage or health care affordability for millions. People with HIV may be particularly vulnerable, given that they are more likely to have Marketplace plans than the public overall and many also rely on the federally-funded Ryan White HIV/AIDS Program, which could be further stretched if Marketplace plans become more expensive. Moreover, loss of coverage and increased costs could lead to disruptions in care for people with HIV which could have serious implications for individual and public health. Being engaged in HIV care, including being on antiretroviral therapy, promotes optimal health outcomes including viral suppression, which in turn prevents transmission of HIV to others. This issue brief provides an overview of these potential impacts.

People with HIV and Marketplace Coverage

A larger share of people with HIV receive coverage through the Marketplaces than the general population. As with Marketplace enrollees overall, the costs they face could rise significantly if the tax credits are not extended (detail on how the enhanced tax credits are calculated and differ from the original ACA tax credit here). For example:

- Scenario 1: A 45-year-old enrolled in a Marketplace plan in Miami-Dade County, FL with an annual income of $38,000 (243% of the federal poverty level (FPL)), demographics similar to the HIV epidemic overall, would pay an estimated $1,699 more per year for coverage for the second lowest cost silver plan, with the monthly premium going from $117 to $259. (Additional scenarios can be run using this KFF interactive tool.)

Separately, those with incomes over 400% of the FPL (estimated at $62,600 in 2026 for a single-individual household) would face a double hit when it comes to cost increases without an extension. First, people with incomes in this range were provided with a new tax credit, limiting premium costs to 8.5% of income, which they would lose entirely without an extension. Second, without any cap on costs, they would be fully exposed to increased premiums proposed for 2026. (This differs from those in the 100%-400% FPL income group who would still receive some federal assistance, albeit at a lower level than with the enhanced credits.)

- Scenario 2: A 45-year-old enrolled in a Marketplace plan in Miami-Dade County, FL with an annual income of $65,000 (415% of the federal poverty level (FPL)), would pay an estimated $2,027 more per year for coverage for the second lowest cost silver plan, with the monthly premium going from $460 to $629. (Additional scenarios can be run using this KFF interactive tool.) Costs would go from being caped at 8.5% of their income to consuming 11.6%

Certain state enrollees are already facing especially large hikes. Looking at the 5 states with the greatest HIV prevalence the, median and range requested premium increases for the 2026 plan year are as follows:

- CA: 14% (7%-20%)

- FL: 26% (19%-41%)

- GA: 20% (9%-43%)

- NY: 13% (10%-37%)

- TX: 19% (3%-42%)

There are multiple potential impacts of increased premium costs for individuals with HIV paying for their own coverage. While some people may retain coverage, and be able to manage the increased costs, others could:

- Retain coverage and struggle with the increased costs.

- Choose a plan with less expensive premiums, but potentially higher out-of-pocket costs for items like HIV medications, labs, and provider visits.

- Drop coverage altogether and not seek alternative access to care or coverage.

- Drop coverage and seek support from the Ryan White Program.

AIDS Drug Assistance (ADAPs) Programs

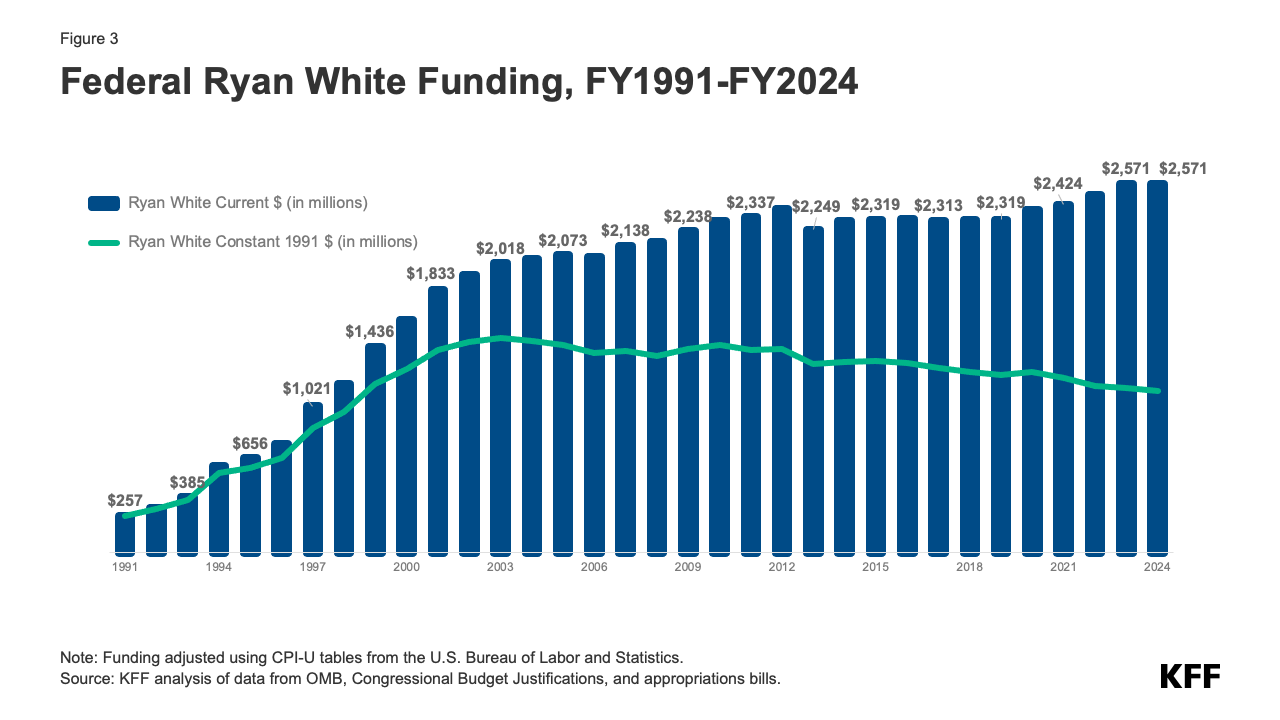

Notably, HIV programs would also be impacted if enhanced tax credits are not extended, with the policy lapse costing them potentially tens of millions of dollars. This is especially the case for AIDS Drug Assistance Programs (ADAPs), which are part of the Ryan White HIV/AIDS Program, a federal safety net program for those with low-to-moderate incomes, reaching over half of people with HIV in the U.S. ADAPs provide HIV medications to people with HIV either directly or by purchasing insurance coverage with prescription drug benefits on their behalf and/or assisting with cost-sharing of insurance coverage. Each state/territory runs its own ADAP and programs differ in their operation and services provided. ADAPs face limited budgets and federal allocations have been fairly flat over time, making the program vulnerable to changes in the size of the population needing services as well as the cost of those services. ADAPs hit with rising premiums or increased enrollment, could be faced with modifying their programs in ways that could impede access.

Insurance purchasing became more widespread once the ACA was signed into law as historically HIV had been an uninsurable condition in the individual market. The health law meant that people with HIV could not be denied coverage or charged more for being HIV positive and that they were assured relatively coverage access to necessary medications and treatments.

Most ADAPs purchase private insurance premiums for clients (at least 42 states and DC in 20231). In total, in 2023 at least 76,365 clients were assisted with insurance assistance that included help paying for premiums across insurance markets. Among all ADAP clients, over 40,0002 were enrolled in Marketplace plans in 2023 and most received insurance support from the program. ADAPs that enroll eligible clients in Marketplace plans receive the benefit of the tax credits (currently available to those 100% of the poverty level and above) and have processes in place to work with clients on tax credit reconciliation at the end of the year. Larger shares of ADAP clients receiving premium support 3 have incomes above 100% FPL (the income level at which tax credit eligibility begins) compared to those enrolled in full-pay drug support only.

How much could the loss of enhanced tax credits cost state ADAPs?

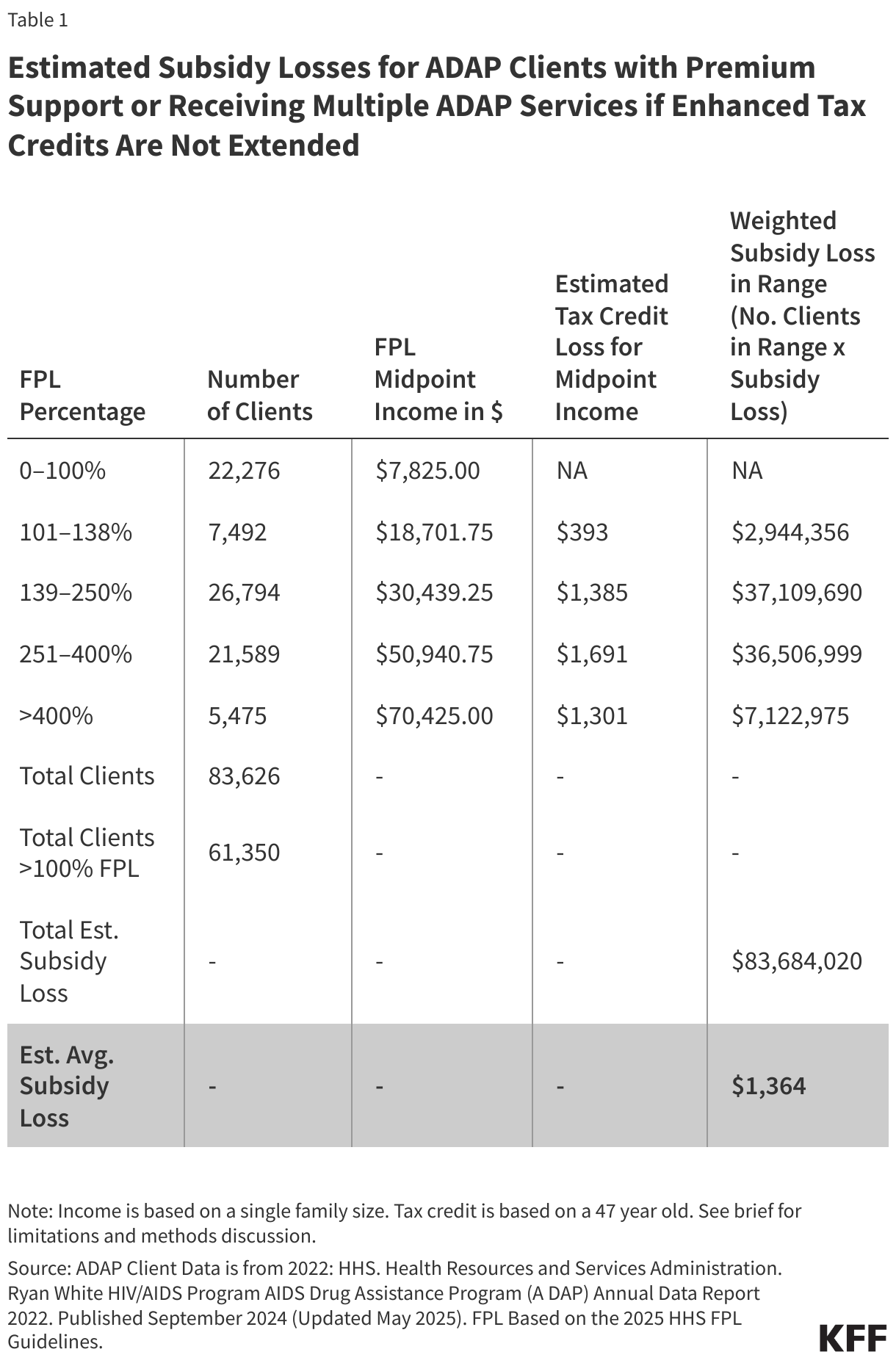

A typical ADAP client (with an average age of 47 and in a single person family) receiving premium support could expect to see an estimated additional $1,364 in premium costs in 2026. This cost would be borne by ADAPs and vary by actual client demographics (i.e. age, income, family size and location for those over 400% FPL who would lose the entirety of their tax credit), metal level enrollment, and the number of clients the ADAP has enrolled in the Marketplaces. Different estimates can be generated using this tool. Overall, this would likely represent a relatively small increase in ADAP budgets. However, concerns have already been raised that this policy change, as well as others that are likely to occur soon as a result of the recent reconciliation bill, could be financially challenging for ADAPs. Additionally, certain state ADAPs, such as those with high marketplace enrollment and those in non-expansion states are likely to be disproportionately impacted if enhanced tax credits. (See Methods and Limitations.)

Increased costs resulting from expiring enhanced tax credits and higher premiums, would not impact ADAPs evenly across the country. Levels of enrollment, differences in typical family income and age of clients, and type of plan enrollment would impact how these changes affect ADAP budgets, among other factors. ADAPs with smaller client enrollment or less robust insurance purchasing programs would be more sheltered and those with larger client enrollment and robust insurance assistance programs would likely to be harder hit. It is possible that ADAPs in non-Medicaid expansion states could being especially impacted. In expansion states, many clients with incomes 100-138% of the FPL would be enrolled in the Medicaid program whereas in non-expansion states, those clients would be more likely to be enrolled in ADAP insurance assistance through the ACA marketplace. For example, the share of ADAP clients enrolled in Marketplace plans (regardless of whether ADAP is assisting with costs) is much higher for Florida (31%) and Georgia (25%), high prevalence non-expansion states, than in California (15%) or Illinois (11%), high prevalence expansion states.

Additionally, as noted above, issuers are planning large premium increases for the coming year. ADAPs with clients enrolled in Marketplace plans would still have some protections from these price hikes through premium tax credits. Even if the enhanced credits expire, clients 100%-400% FPL would still have the original tax credits provided through the ACA. However, clients enrolled in off Marketplace ACA compliant plans (about 9,600 clients in 2023) and clients with incomes over 400% FPL (7% of ADAP clients with premium support or multiple types of ADAP support in 2022) would not have any buffer against these rising costs. Further, ADAPs might also face higher costs if those who had been purchasing coverage independently, find increases in premiums unaffordable and turn to the program for assistance.

Even relatively small cost increases in ADAP budgets can challenge their ability to maintain their current levels of services and some have raised questions about how they would respond to this and other future policy changes. ADAPs could respond in a number of ways, some of which could amount to limiting access to program services or generosity and/or seeking alternative resources to supplement federal funds:

- Cost-containment strategies could include changing the eligibility for the program – for example reducing the income eligibility level – or further limiting plans in which clients can enroll. Another possible action is making ADAP formularies for clients receiving direct drug assistance less generous or introducing more utilization management techniques like prior authorization or step-therapy. ADAPs could also introduce or reduce caps on their programs (or on drug utilization) and could also create waiting lists. Waiting lists have been used in the past when program budgets have been strained but were last cleared through infusion of supplemental federal funds in 2012.

- ADAPs faced with increased costs could try and supplement ADAP earmark funding (funding dedicated to ADAPs by Congress) with funding from other sources such as the state’s non-ADAP Ryan White fundings (Part B), funding from local county/city Ryan White Grantees (Part A), other state/local funding, maximizing generation of program income, and seeking deeper rebates from pharmaceutical companies, among other actions. However, if funding is shifted from Part B or other state or local funding (entities with already constrained budgets) to ADAPs, this could mean a reduction of other public health services.

Beyond ADAPs, grantees of other “Parts” of the Ryan White Program are also permitted to use funding to support client enrollment in health insurance, including in Marketplace plans. While this occurs less commonly among other grantees than it does with ADAPs, any other grantees currently using funding this way, would also be impacted by the above cost-increases resulting from expiration of enhanced tax credits and increases premiums for 2026.

Potential Impact of Policy Changes on HIV Care

As described above, if these changes occur, they are likely to have an impact on both individuals with HIV and the programs people with HIV rely on. Individuals could lose coverage and/or face higher costs, and might turn to Ryan White for assistance. To address funding shortfalls due to these changes, ADAPs could work to inject new funding into their programs but could also constrain existing eligibility and benefits or restrict enrollment.

Increased premiums or certain changes to ADAPs could lead to enrollees being less engaged with or fall out of HIV care and treatment. Higher out-of-pocket costs are a known deterrent to care engagement. KFF has found that over-quarter (27%) of people with HIV who are out-of-care say that at least one barrier to care has been problems with money or insurance and of those who recently missed an antiretroviral dose, nearly 10% say problems were as a barrier. Since HIV care and treatment engagement improves individual health and because viral suppression prevents transmission of HIV to others, monitoring access to services and safety net program capacity moving ahead will be important, as will assessing the potential public health impact, if people with HIV lose access to care and treatment.

Finally, while the potential expiration of tax credits is a looming major change on the health policy horizon, there are other significant changes coming that could impact care, coverage, and programs for people with HIV. The recent budget reconciliation bill (HR1) makes a range of changes to the health system that will reduce coverage, some impacting the private market but the biggest, reshaping state Medicaid programs, the primary payer for HIV care in the U.S. These changes too could put downward pressure on ADAPs which are already operating on budgets that have remained mostly flat for decades.

{kind=link}

Methods and Limitations

Methods: The estimated average income was generated based on income and age date from the Health Resources and Services Administration (HRSA). Ryan White HIV/AIDS Program AIDS Drug Assistance Program (ADAP) Annual Data Report 2022. Published September 2024 (Updated May 2025). The data is based on 2022 ADAP client enrollment. Age and income data was examined for ADAP clients with premium support and those getting multiple ADAP services (likely including premium support). Age and income data in the HRSA report is presented in ranges with the number of clients in each category. The range midpoints were identified within each category. For age, the estimated average age was calculated based on a weighted average of age midpoints, excluding those over 65, a group likely enrolled in Medicare. The average age used in this analysis was 47. For each income category incomes were calculated based off the range midpoints using the 2025 FPL guidelines from HHS. For the mid-point of each category for incomes above 100% FPL (those currently tax credit eligible), the increased cost of expired tax credits was assessed using the KFF calculator and then weighted based on the number of clients within the category (the weighted average estimated increases for each range are below). This analysis used the “US average”, and was based on a single person family size, representing a national average of second-lowest cost silver page weighted by plan selections. Across all income categories we estimated an average subsidy loss of $1,364. (See Table 1.)

Limitations: There are several limitations with this estimate: While those over 65 were excluded from the average age estimates, it was not possible to exclude the incomes of those over 65 from the income calculations. It is possible Marketplace enrollees have different demographics from these estimates which include clients receiving any ADAP insurance premium (e.g. some clients receiving ADAP assistance for employer insurance). It is estimated that about 40,000 ADAP clients are enrolled in Marketplace plans (the data above is for about 60,000 clients). In particular, it is possible that these income estimates are high given that those with employer coverage are likely to have higher incomes than those with Marketplace coverage. The estimates also inlcude those receiving “multiple ADAP services” which is thought to inlcude those with premium assistance but could theoretically inlcude others. Averages could also obscure actual changes in costs. Location of enrollment should not impact costs for most of those under 400% FPL because of the structure of the tax credits. However, the US average used for the location may be imprecise for the 7% of enrollees assisted with premiums over 400% whose costs would vary by location. As noted above, actual costs will vary by client demographics (i.e. age, income, family size and location for those over 400% FPL who would lose the entirety of their tax credit) as well as client plan metal level enrollment. Additional scenarios can be run using the KFF calculator.

- Data from Alabama, Montana, and West Virginia were not available. ↩︎

- The number of ADAP clients in Marketplace plans in unknown in full or in part in several states, including New York and Texas, states with high HIV prevalence and ADAP enrollment, so this is likely an undercount. ↩︎

- This is not specific to QHP enrollees includes any client getting premium support (e.g. it includes those getting assistance for employer plans or other coverage). ↩︎