Tariffs Are Driving up Premiums for Small Businesses

Small businesses may expect that the recent tariffs levied by President Trump will drive up the price of multiple imported goods from various countries. But less expected is how these trade policies may ripple through employee health benefits. Most recently, President Trump indicated that the administration will phase in tariffs on pharmaceutical imports—starting with a “small tariff,” climbing to 150% within roughly 12 to 18 months, and eventually rising to as much as 250%—as part of an effort to bring drug manufacturing back to the U.S.

Tariffs can indirectly affect health insurance premiums by increasing the cost of imported medical goods, especially prescription drugs. When pricing plans, insurers must make assumptions about future medical costs, often months in advance. In the absence of clear policy guidance, some insurers take a cautious approach by incorporating potential cost increases into their proposed rates for the upcoming plan year. Rather than waiting for final decisions, some carriers preemptively accounted for these risks to avoid underpricing. This can be particularly true when the affected drugs are brand-name or specialty medications with limited alternatives, many of which are imported. By building in assumptions about possible cost increases, tariffs can influence premiums even before any measurable price change has occurred, particularly in markets where insurers may already operate on tighter margins.

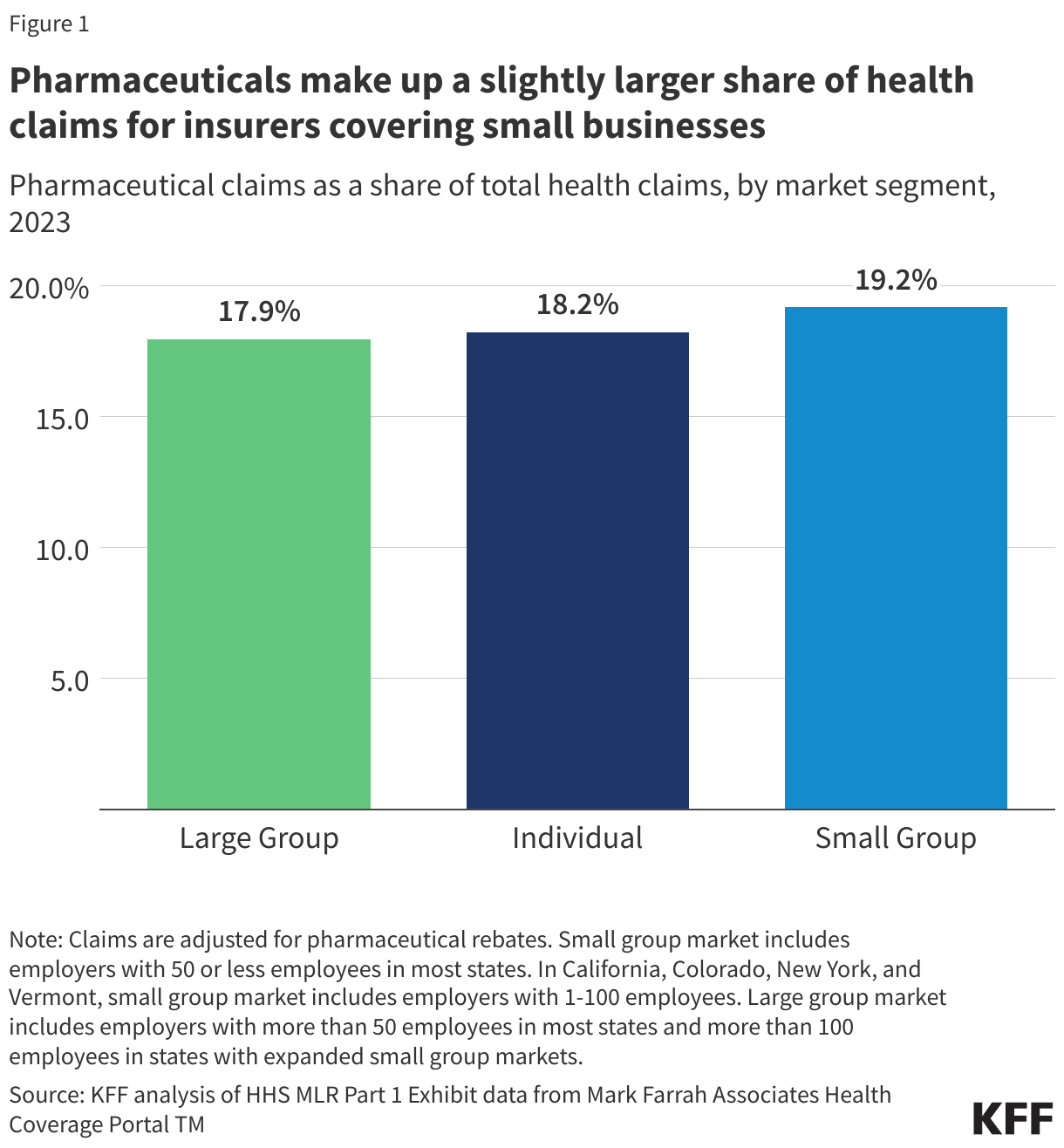

The share of total health claims attributable to pharmaceuticals varies by market segment but generally makes up between one-sixth and one-fifth of total claims after adjusting for pharmaceutical rebates.

Pharmaceuticals comprise a slightly larger share of total health care claims in the small group market compared to the individual and large group markets. In the small group market, pharmaceuticals account for just under one-fifth of all claims (19.2%), while the share is slightly lower in the individual (18.2%) and large group (17.9%) markets.

Health insurance companies must submit their proposed premium changes for the coming year to state regulators in the spring and summer. As part of this process, some insurers in the Affordable Care Act (ACA)-compliant guaranteed-issue small group market — just as in the individual market — are explicitly citing tariffs, particularly those affecting pharmaceutical imports, as a reason for higher-than-expected premium increases. In the individual market, several insurers have included upward adjustments of about 3% in response to anticipated increases in drug costs tied to tariffs, while others acknowledge the risk but have not incorporated it into their pricing assumptions. Of the 88 small group market rate filings reviewed in detail, one-quarter (22 insurers) explicitly mentioned tariffs. Other insurers may have factored in tariff effects without stating so directly.

In several states, small group filings note that new import tariffs are expected to increase the cost of certain brand-name and specialty drugs, especially those without generic alternatives.

“IHBC is seeking an overall rate change of 18.9% in 2026, primarily due to increased costs due to inflation and tariffs.” – Independent Health Benefits Corporation (New York)

“To account for uncertainty regarding tariffs and/or the onshoring of manufacturing and their impact on total medical costs, most notably pharmaceuticals, a total claims impact of 2.9% is built into the initially submitted rate filings. This has increased our premium by roughly 2.7%.” – United Healthcare Insurance Company (Oregon)

Among small group insurers that have accounted for the potential impact of tariffs in their rate filings, the estimated premium effect ranges from 1.7% to 3.0%. Other insurers reference the possibility of tariffs but do not factor them into their pricing assumptions.

“Neighborhood did not consider the impact of tariffs during rate development as rates were created based on current law today and too much uncertainty remains of what (if any) tariffs will become final.” – Neighborhood Health Plan of Rhode Island (Rhode Island)

Because insurers in the ACA-compliant small group market must lock in premiums well ahead of the coverage year — often six to nine months in advance — they are frequently pricing against policy uncertainty. Unlike inflation or shifts in service utilization where insurers can draw on historical experience, there is little precedent for how sweeping import tariffs could affect prescription drug pricing.

Additionally, ACA-compliant small group insurers must also adhere to Medical Loss Ratio (MLR) requirements, which limit the share of premiums that can go toward administrative costs and profit. If premiums overshoot actual spending, carriers are required to issue rebates. But if they underprice premiums and tariffs drive up drug costs, insurers could face financial shortfalls.

This dynamic could translate into higher employee benefit costs for small businesses as these tariffs take effect and impact drug prices. For employers operating on narrow margins, even small premium increases can influence decisions around employer contributions, cost sharing, or continuing to offer coverage at all. While ACA’s MLR rules shield employers from some costs by requiring insurers to return excess premiums if spending falls short, these rules do not insulate businesses or workers from the upfront burden of higher premiums. With no clear precedent to guide assumptions, tariff-related uncertainty is now a factor in how some small group insurers approach rate-setting — adding a new variable to the affordability of some job-based coverage.