How an ACA Premium Spike Will Affect Family Budgets, and Voters

If the enhanced ACA tax credits are not extended, premium payments will increase by more than 100% for many of the 24 million Americans who buy their own coverage (as forthcoming KFF research will show), and that’s on top of rising food and housing costs among other inflationary pressures that are already stressing many families out.

The impact will be felt especially hard in red states that did not expand Medicaid and by groups Republicans traditionally rely on to vote for them. Take small business owners, for example. Half of voters who purchase their own health insurance are small businesses or work for them. Or farmers—a quarter of all farmers get their coverage from the Marketplaces. It’s an open question whether President Trump’s loyal base will protect him, and Republicans more generally, from the usual consequences that a party in power face when voters’ costs rise, especially when they were promised they would go down.

Congress is belatedly coming to grips with the consequences of not extending the credits and a partial fix is looking increasingly possible. The tab for a full extension, $350 billion over 10 years, is likely too steep for Republicans and Democrats to agree on. A shorter extension would increase federal costs by about $30 billion per year, assuming the structure of the credits isn’t modified. President Trump may be the wild card, as he will ultimately have to agree to any deal Republicans may want to make to avoid blowback at the polls. However, his interests are different than those of a House member who has to stand for re-election, and “Obamacare” has never been his favorite program.

People will experience these health cost increases in the context of their family budgets. For literally decades, I have been giving speeches and writing about how voters view health care as a dimension of their economic concerns, and not as a separate issue. I see it that way because when we conduct surveys about voters’ top concerns, we ask likely voters who tell us that the economy is their top issue to explain what specifically about the economy worries them, and health and drug costs are usually near the top of the list, along with costs of food, housing, utilities, and gas. (Many aspects of health care, obviously, have nothing to do with costs, especially when you are sick.) The ordering of concerns jumps around depending on the year, but health care costs are always there and sometimes at the top. That’s important because that’s how Marketplace enrollees will experience premium spikes—within the context of everything else going on in their family budgets. The political impact of rising prices is then multiplied by the family members who will see or share their plight. If you see your kids suffering economically from something Congress did or did not do, or your parents, or even a close friend, that can affect your vote, too. The amount of the increase is material to its impact and people’s reactions. So is their income level. And the fact that food and housing and other costs are rising at the same time compounds the effects economically and politically.

Consider the following two illustrations of how premium increases could affect family budgets at somewhat different income levels for Marketplace enrollees, by comparing them to food and utility costs:

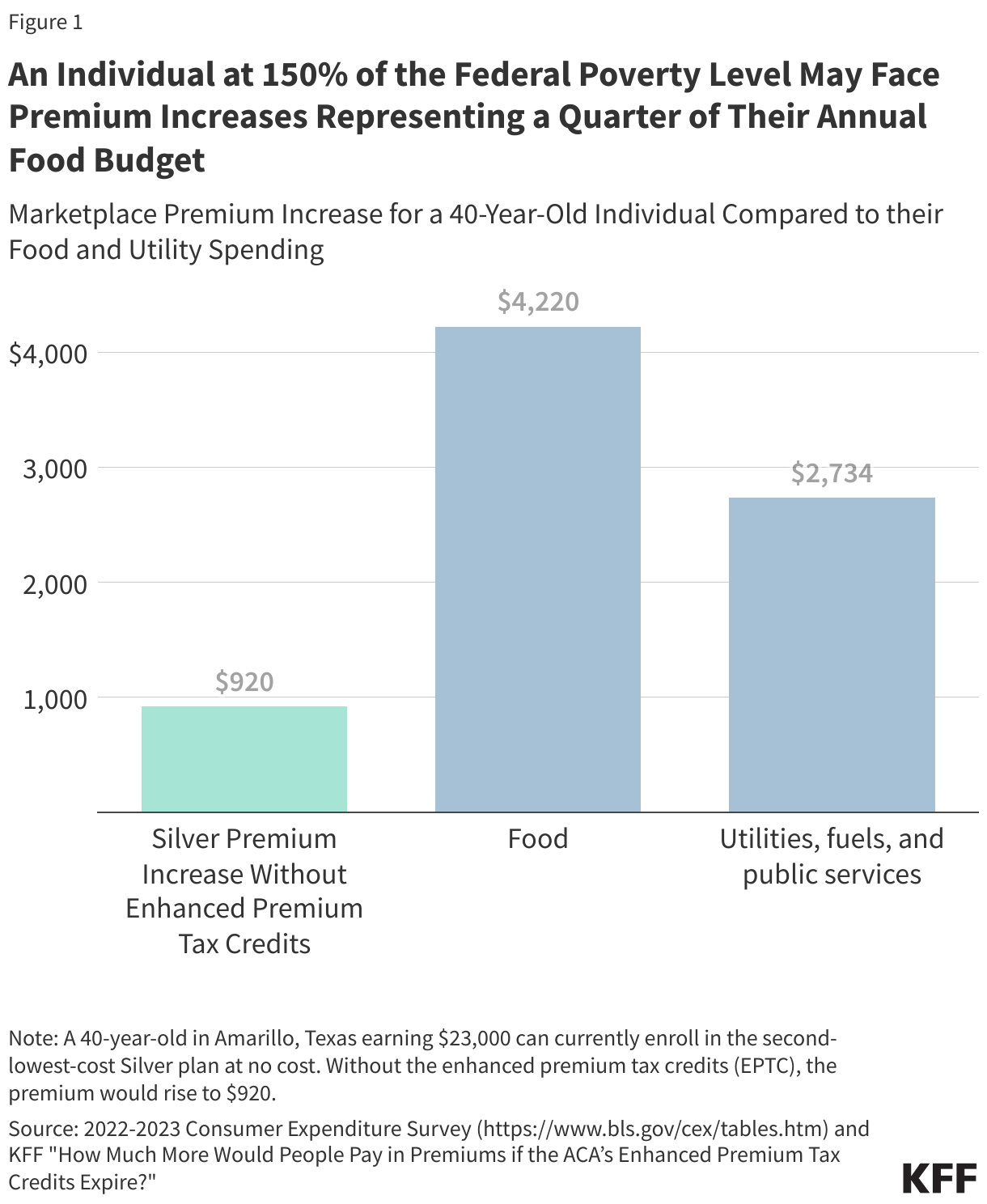

A Lower-Income Enrollee

Low-income Marketplace enrollees (with incomes below 150% of the federal poverty level) can currently enroll at no cost in a silver plan that has a significantly lowered deductible (often less than $100). If enhanced premium tax credits expire, they would be required to pay upwards of 4% of their income to purchase the same plan.

For example, a 40-year-old in Amarillo, Texas earning $23,000 per year could see their premium rise from $0 to $920 annually. While they would still receive financial help, the added expense could strain already tight household budgets for people living just above the poverty level. In this case, the premium increase would be the equivalent of about a quarter (22%) of their typical annual food budget, or about a third (34%) of the average utility and fuel budget for individuals with similar incomes. They could switch to a bronze plan to keep their $0 monthly premium, but that would likely leave them with a deductible that is about $7,000 higher than their current plan (for someone with a $23,000 income, that’s pretty useless coverage).

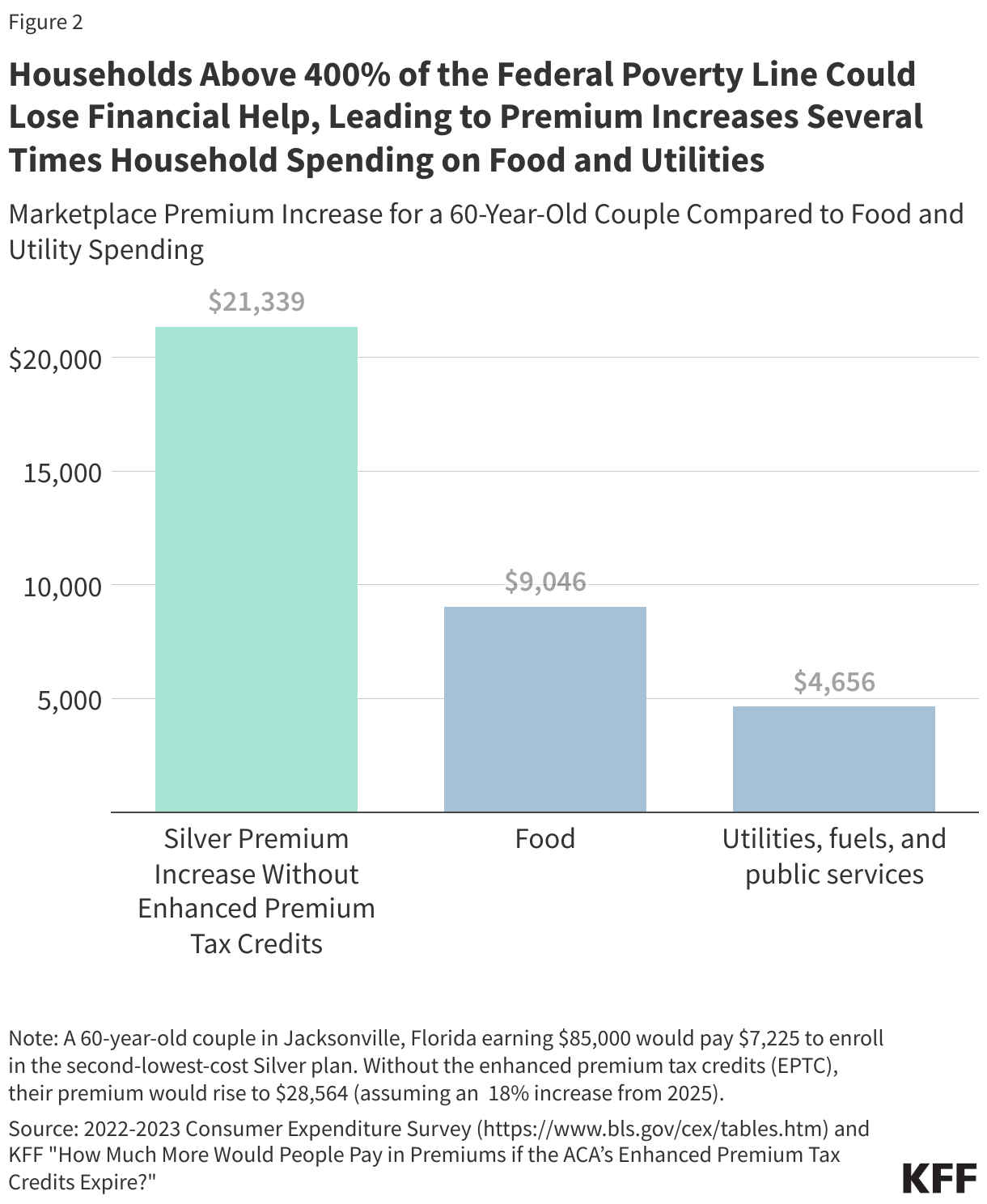

A Moderate-Income Enrollee

The consequences are more stark for some households with incomes above 400% of the federal poverty line, who risk losing financial help all together. Consider a 60-year-old couple in Jacksonville, Florida with a combined income of $85,000. With enhanced tax credits, they pay $7,225 annually to enroll in a silver plan, which is 8.5% of their income. But if the enhanced tax credits expire, they will no longer be eligible for any financial help. They would not only lose their $16,982 tax credit, but would also face the underlying rising cost of health insurance, which is expected to be 18% next year. If enhanced premium tax credits are extended, their monthly costs would remain about the same in 2026. But if the enhanced tax credits expire and premiums rise 18% on top of that, they would have to pay as much as $28,561 (about a third of their annual income) for the same plan. That’s an increase of $21,339 in their annual premium costs. For comparison, a two-person household in this income bracket spends an average of $6,928 per year on food. The loss of financial help would mean the increase in their premium cost is about triple their food bill.

This is how almost 24 million moderate-income working people will experience the loss of the enhanced tax credits—in the context of family budgets already straining to pay for food, utilities and housing. They don’t look at it the way we often do in health—“it’s X dollars more.” They experience it as X dollars more on top of everything else. And right now, most everything else is also going up.