ACA Insurers Are Raising Premiums by an Estimated 26%, but Most Enrollees Could See Sharper Increases in What They Pay

Published: October 28, 2025

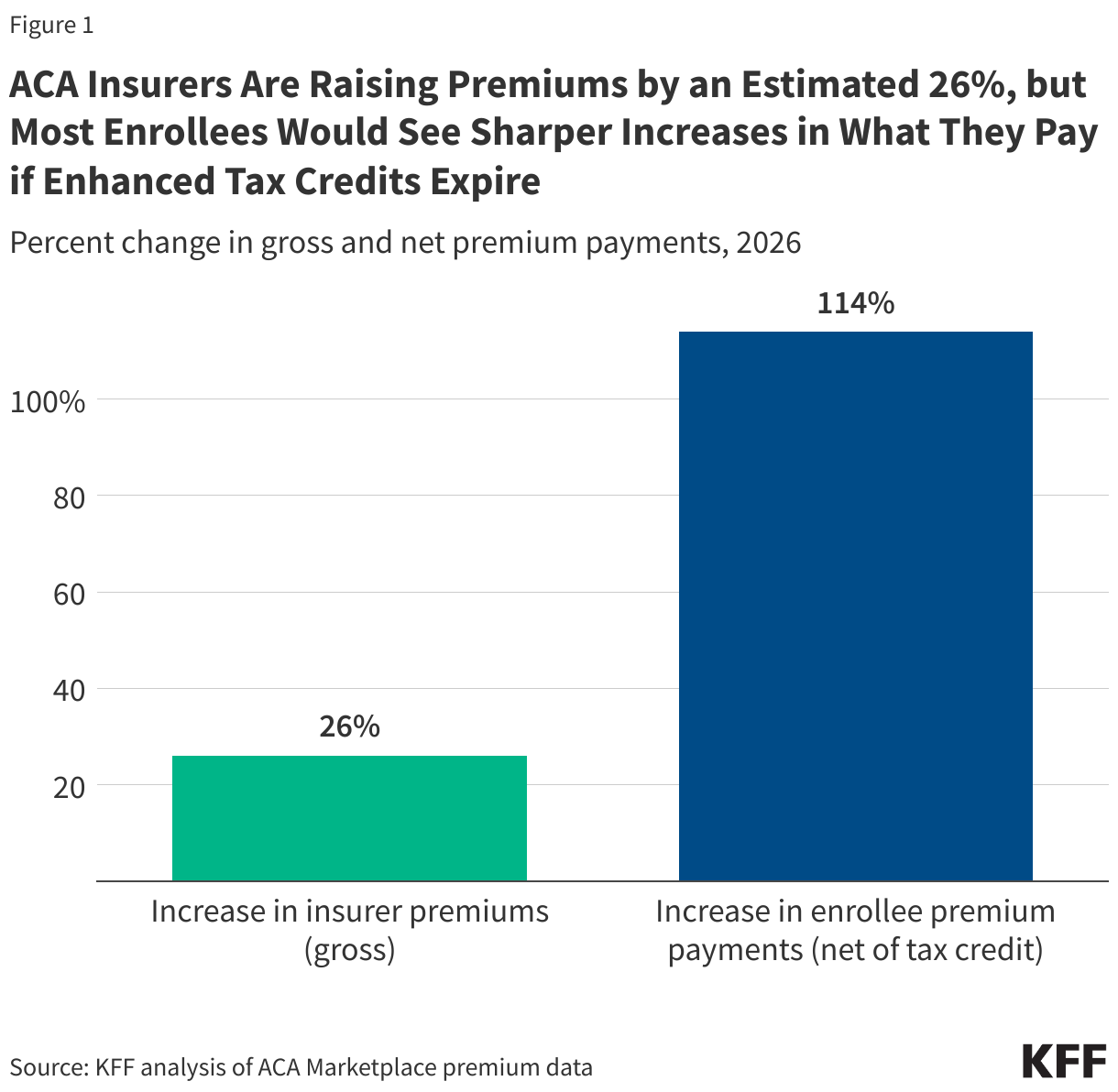

The amount health insurers charge for coverage on the ACA Marketplaces is rising 26%, on average, in 2026. In states that run their own Marketplaces, the average benchmark (second-lowest cost) silver premium, on which the tax credit calculation is based, is rising 17% next year. In states that use Healthcare.gov, these premiums are rising an average of 30%.

Most enrollees would face even sharper increases in what they pay if the ACA’s enhanced premium tax credits expire. This 26% is the increase in the amount insurers are charging, which in most cases is not what enrollees pay. 22 million out of 24 million marketplace enrollees currently receive a tax credit. The amount subsidized enrollees pay is not what insurers charge, but rather a sliding-scale share of their household income, based on a formula set by Congress. If Congress extends the enhanced tax credits, the amount subsidized enrollees pay each month will remain about the same, even though the amount insurers are charging is increasing sharply.

If the enhanced premium tax credits expire at the end of this year, KFF estimates that currently subsidized enrollees will see their monthly premium payments more than double, increasing by about 114%, on average. This reflects people with incomes below four times the poverty level receiving less financial assistance and those with incomes over four times poverty no longer being eligible for financial assistance at all and therefore being hit by a double whammy of lost tax credit and higher insurer premiums.

Even if the enhanced tax credits expire, many lower income enrollees will continue to be eligible for a bronze plan with zero or a very low premium payment after accounting for the smaller tax credit they will continue to receive. However, this could mean switching from a silver plan with a reduced deductible as low as under $100 to a bronze plan with a deductible of over $7,000.

The amount insurers charge for ACA Marketplace premiums is rising for several reasons, including but not limited to increasing hospital costs, the rising popularity of expensive GLP-1 drugs like Ozempic, and the threat of tariffs. These factors are similarly cited by insurers selling employer coverage. However, an additional factor driving up the amount insurers charge for ACA Marketplace premiums (that is not affecting employer premiums) is the expected expiration of the enhanced premium tax credit. In their 2026 filings to state regulators describing their requested premium increases, ACA Marketplace insurers said they would charge about 4 percentage points more, on average, than they otherwise would have because they expected healthier people to drop Marketplace coverage if enhanced premiums tax credit expire.

Because the ACA’s tax credit is tied to the cost of the second-lowest cost silver plan, when these benchmark premiums rise, so does the federal cost of offering tax credits.