How ACA Repeal and Replace Proposals Could Affect Coverage and Premiums for Older Adults and Have Spillover Effects for Medicare

Now that the House has passed its bill to repeal and replace the Affordable Care Act (ACA), Senate negotiators face a number of policy decisions that could be of particular interest to older adults who are not quite old enough for Medicare. Prior to the ACA, adults in their fifties and early 60s were arguably most at risk in the private health insurance market. They were more likely than younger adults to be diagnosed with certain conditions, like cancer and diabetes, for which insurers denied coverage. They were also more likely to face unaffordable premiums because insurers had broad latitude (in nearly all states) to set high premiums for older and sicker enrollees.

The ACA included several provisions that aimed to address problems older adults faced in finding more affordable health insurance coverage, including guaranteed access to insurance, limits on age rating, and a prohibition on premium surcharges for people with pre-existing conditions.

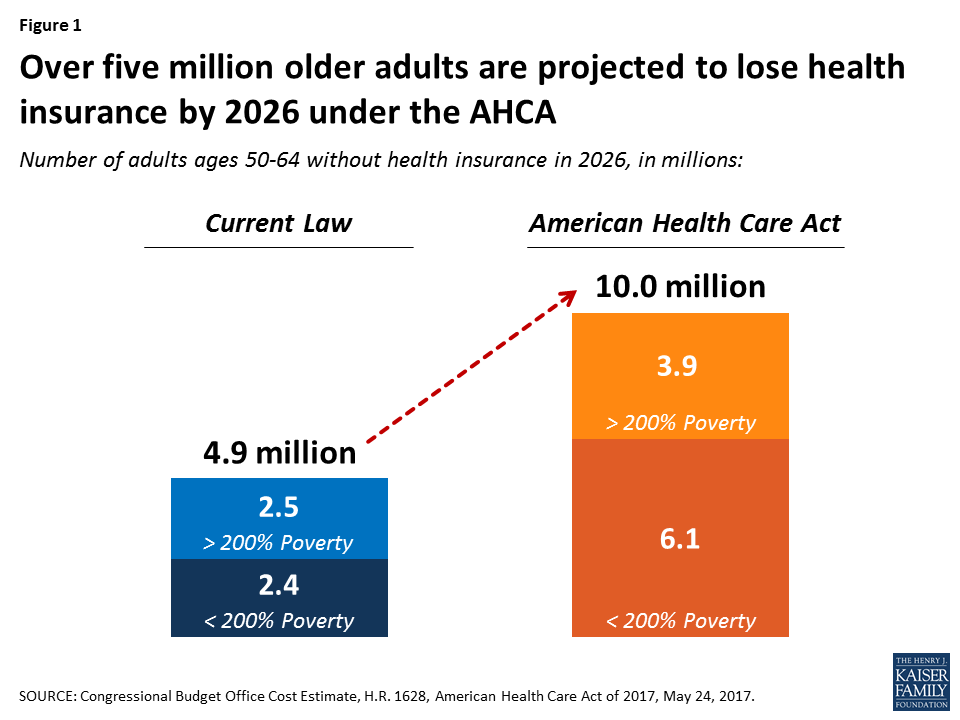

The House-passed American Health Care Act (AHCA) would make a number of changes to current law that would result in a 5.1 million increase in the number of uninsured 50-64-year-olds in 2026, according to CBO’s updated analysis (Figure 1).

Figure 1: Over five million older adults are projected to lose health insurance by 2026 under the AHCA

These changes would disproportionately affect older adults with incomes below 200% of poverty. Adults age 50-64 with incomes below 200% of the poverty level would see the biggest loss of coverage under the AHCA – a 150% increase in the number of uninsured in 2026 relative to current law, compared to 90% for all adults. CBO projects the share of low-income older adults who are uninsured would rise from 12% under current law to 29% under the AHCA by 2026.

The increase in the number and share of uninsured older adults would be due to the following provisions in the AHCA:

- Age Bands. The AHCA broadens the limits on age bands established under the ACA, a change that is likely to lead to higher premiums for older enrollees. The ACA prohibits insurers from charging older adults more than 3-times the premium amount for younger adults. The House bill would allow insurers to charge older adults five times more than younger adults, beginning in 2018. States would have flexibility to establish different age bands (broader or narrower).

- State Waivers. The AHCA allows states to seek waivers that, if approved, would allow insurers to opt out of the ACA’s community rating and benefit requirements. Insurers in these states could charge a higher premium to an applicant with a pre-existing condition who had a lapse in coverage of 63 days or more. Before the ACA, insurers in nearly all states could deny non-group coverage for people with pre-existing conditions or charge them higher premiums. These waivers would lower premiums for people who are healthy, but raise premiums and out-of-pocket costs for people who are sick.

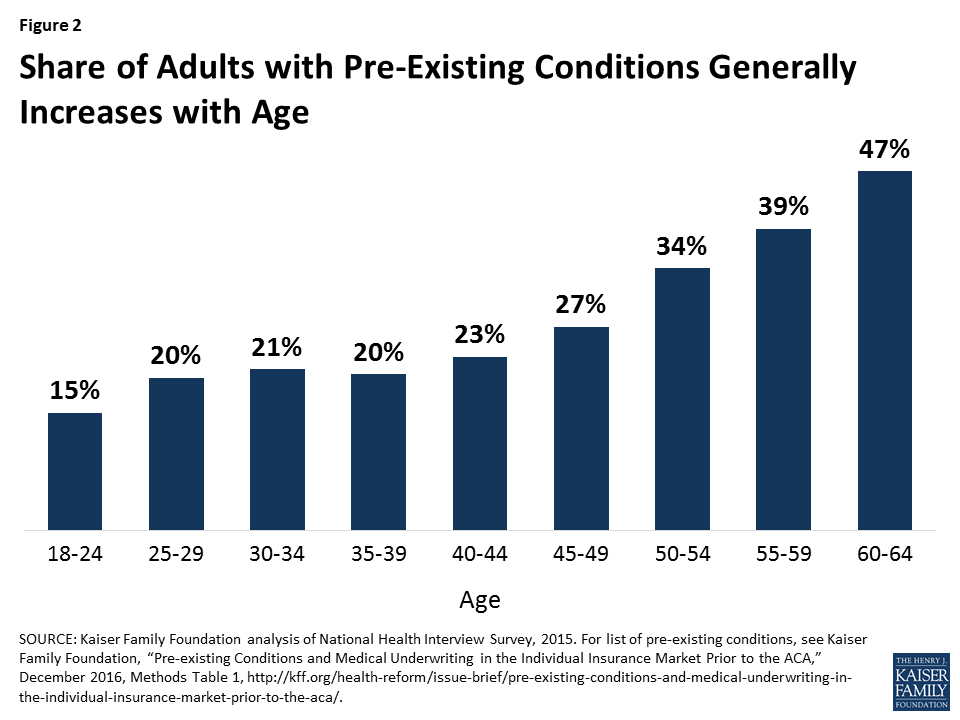

Because many health problems and pre-existing conditions tend to increase with age, the opt-out could particularly affect older adults. For example, 47% of adults age 60-64 have a pre-existing condition that would have led to a denial of coverage pre-ACA, compared to 27% of non-elderly adults overall (Figure 2).

Figure 2: Share of Adults with Pre-Existing Conditions Generally Increases with Age

- Tax Credits. The AHCA changes the way that premium tax credits are calculated, providing lower premium subsidies for low-income adults, relative to the ACA – a change that would have a particularly pronounced effect for low-income older adults. The combination of higher premiums (due to wider age bands) and lower tax credits (especially for those with lower incomes) will result in higher out-of-pocket premiums for older adults.

CBO’s updated analysis illustrates how these proposed changes to the non-group market result in substantially higher premiums for low-income older adults. According to CBO, a 64-year-old adult living on an income of $26,500 would, on average nationwide, pay a premium of $1,700 under current law in 2026, after receiving a tax credit of $13,600. Under the AHCA, the tax credit for that 64-year-old would fall to $4,900, resulting in an average out-of-pocket premium in states not seeking waivers of $16,100. That premium would also be for a plan, according to CBO’s estimates, with a higher deductible than under current law.

Even in states that waive federal market regulations for benefits and community rating, the out-of-pocket premium for this low-income 64-year-old would rise to $13,600. The impact on higher income 64-year-olds relative to current law would be more modest, since AHCA tax credits do not phase out by income like the ACA.

The effects would vary geographically since AHCA tax credits (unlike ACA credits) do not vary based on actual local premiums. For example, in Mecklenburg County, North Carolina (an area with particularly high premiums), a 60-year-old enrollee with income of $20,000 would pay $960 per year in premiums in 2020 for a mid-range plan under the ACA and would pay $19,060 for equivalent coverage under the AHCA. The increased premiums would be less pronounced in areas with lower premiums. But, given the effects of changes under the AHCA in allowed premium variation due to age, low and middle income older adults would see increases in premiums in almost all areas of the country (as shown here). Older adults with higher incomes would fare better, since they would receive premium tax credits under the AHCA but not the ACA. - Medicaid. Changes to Medicaid could also affect coverage and costs for low-income older adults, depending on how states respond to new financial arrangements in the AHCA. The AHCA would limit federal funds for states that have elected to expand coverage under Medicaid, repealing the ACA’s higher federal match for these expansion states as of January 2020. This provision – along with a cap on the growth in federal Medicaid funding over time on a per capita basis – is expected to result in 14 million people losing Medicaid coverage by 2026, some of whom would no doubt be older adults. In 2013, about 6.5 million 50-64-year-olds relied on Medicaid for their health insurance coverage.1

The loss of coverage for adults in their 50s and early 60s could have ripple effects for Medicare, a possibility that has received little attention. If the AHCA results in a loss of health insurance for a meaningful number of people in their late 50s and early 60s, as CBO projects, there is good reason to believe that people who lose insurance will delay care, if they can, until they turn 65 and go on Medicare, and then use more services once on Medicare. This could cause Medicare to increase, and when Medicare spending rises, premiums and cost-sharing do too.

A 2007 study published in the New England Journal of Medicine that looked at previously uninsured Medicare beneficiaries helps explain this dynamic. It showed a direct relationship between lack of insurance (pre-65) to higher service use and spending (post-65). Previously uninsured adults were more likely than those with insurance to report a decline in health, and a decline in health (pre-65) was associated with 23.4% more doctor visits and 37% more hospitalizations after age 65. Depending on the number of people who lose coverage and how long they remain uninsured, the impact for Medicare may initially be modest, but could compound with time.

In addition, the AHCA would repeal the Medicare payroll tax imposed on high earners, a change that would accelerate the insolvency of the Medicare Hospital Insurance Trust Fund and put the financing of future Medicare benefits at greater risk for current and future generations of older adults – another factor to consider as this debate moves forward.

This issue brief was funded in part by The Retirement Research Foundation.