Financial Performance of Medicare Advantage, Individual, and Group Health Insurance Markets

Medicare-for-All proposals have sparked discussion about the role of private health insurance in the U.S. health care system. Some of the current Medicare-for-All proposals would essentially eliminate private insurance. Others would allow private insurers to administer benefits under the new public program, similar to the role of Medicare Advantage plans today, which serve as a private-plan alternative to traditional Medicare. Another set of proposals would create a new Medicare-like public plan option, but preserve a role for private health insurance, including employer-sponsored coverage and policies sold to individuals and families in the Affordable Care Act (ACA) Marketplaces.

As context for these discussions, this brief examines and compares the financial performance of insurers in the Medicare Advantage, individual, and fully-insured group markets, using data reported by insurance companies to the National Association of Insurance Commissioners and compiled by Mark Farrah Associates. We analyze how insurers’ gross margins vary across the three markets, over time, and among insurers. Gross margins are the difference between premiums collected and medical expenses and do not account for administrative expenses. The brief also examines medical expenses as a percentage of premiums collected (simple loss ratios) across these three markets. See the Methods section for more information on calculations.

Key findings include:

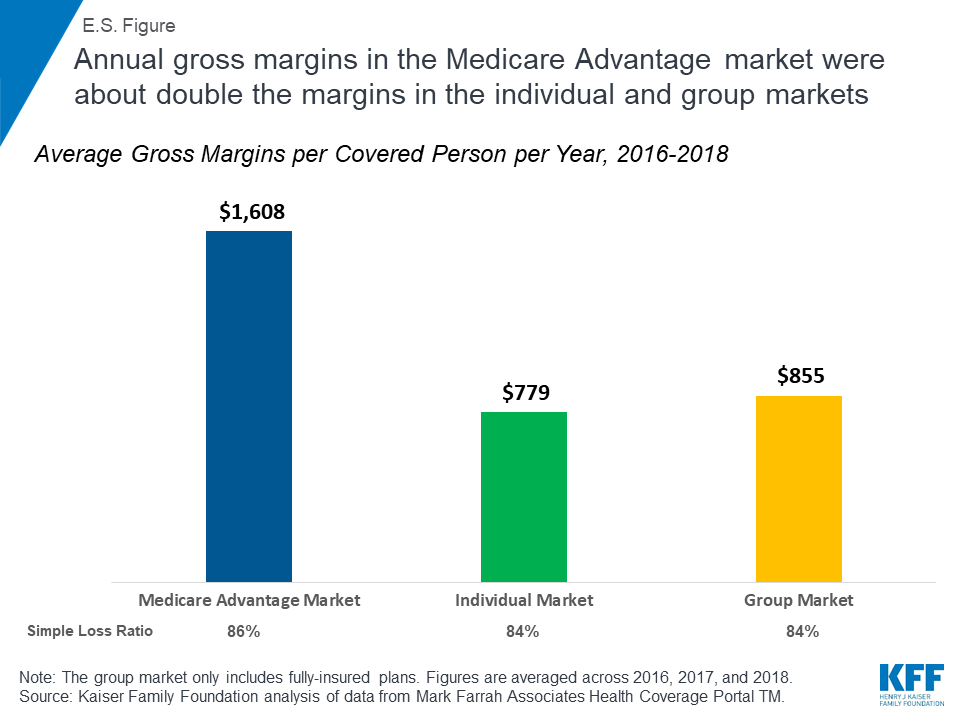

- Annual gross margins in the Medicare Advantage market averaged $1,608 per covered person between 2016 and 2018, about double the margins in the individual and group markets (E.S. Figure). Between 2016 and 2018, the individual market experienced substantial volatility, and the three-year average gross margins are not representative of any single year. In 2016, individual market insurers saw significant losses, and in 2018, margins were unusually high and plans were overpriced due to policy uncertainty.

- When aggregated across all plans in this analysis, annual gross margins sum to $23.9 billion, $10.6 billion, and $26.5 billion for the Medicare Advantage, individual, and group markets, respectively, for 2016-2018.

- Total medical expenses as a share of premiums collected (simple loss ratios) were similar for across the three markets between 2016 and 2018 (about 84-86%; E.S. Figure).

ES Figure: Annual gross margins in the Medicare Advantage market were about double the margins in the individual and group markets

Each of these three health insurance markets now appear to generate high gross margins per person, particularly for insurers of Medicare Advantage plans.